China Needs to Engineer a Beautiful Deleveraging

This article from Ray Dalio may be of interest. Here is a section:

So, how do those who reduce the debt burdens do it? It primarily depends on whether the debt is in one’s own currency or a foreign currency (if it’s in one’s own currency like China’s debt is, it’s easier to manage) and whether it is held by one’s own citizens or foreigners (if it’s held by one’s own citizens like China’s debt is, it’s easier to manage)—though it is never easy. Given these circumstances, it also depends on how the restructuring is done. A well-done restructuring happens in a balanced way. I call that a “beautiful deleveraging.” It balances deflationary defaults/restructurings with inflationary printing of money/debt monetization to spread out the burden. The mechanics of this process are explained in the first chapter of the book linked above, so I won’t try to squeeze them in here.

China is overdue in doing this, so in my opinion, it needs to follow this beautiful deleveraging process now because the debt-burdened balance sheets and burdensome debt service payments are freezing the economy, especially at the provincial level and most especially in some of the poorest provinces. One day the United States, Europe, and Japan will probably have to do their own deleveragings, which I expect to follow this process. Because the stabilities of orders (also known as “Mandates of Heaven”) in all countries are driven by the interrelated forces of 1) the credit/debt/economic dynamic, 2) the internal political dynamic, 3) the external geopolitical dynamic, 4) acts of nature (i.e., droughts, floods, and pandemics), and 5) human inventiveness (especially of new technologies), and because how this deleveraging process is handled has a big effect on the overall order or disorder of the system, it’s worth keeping in mind how this deleveraging dynamic works, which is why I’m passing along Principles for Navigating Big Debt Crises to you now. I hope it’s of some help.

We can assume China’s policy makers have a better understanding of the country’s debt issues that we do. There is no doubt having the majority of debt denominated in the domestic currency and having few external liabilities provides China with a strong position to deal with excess debt.

If deleveraging is performed flawlessly, the process could take a decade or longer of subpar growth. The importance of construction and property to the economy will need to shrink. That represents an existential threat to the global commodity sector which depends on Chinese demand growth to support production aspirations.

The big question is how committed the Chinese administration is to deleveraging? If they abandon the program, it will support global markets, but the problem would then only become worse. The tier 1 cities already have the most expensive property in the world relative to domestic incomes. That’s unsustainable without massive stimulus which the government has been unwilling to provide.

The LME Metals Index continues to trend fall towards the lower side of its yearlong range. The 3500 level needs to hold if the benefit of the doubt is to give to support building.

The LME Metals Index continues to trend fall towards the lower side of its yearlong range. The 3500 level needs to hold if the benefit of the doubt is to give to support building.

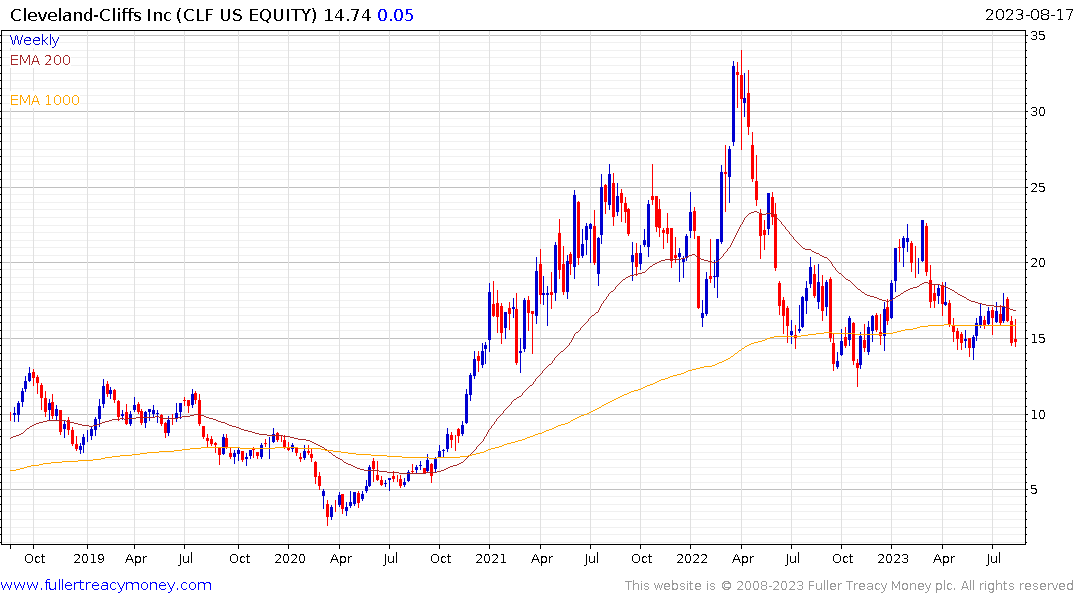

The speculative interest around US Steel, as several companies compete to acquire it, suggests executives are scrambling to gain access to recycled inventory to fuel lower carbon electric arc furnaces. The headwind from Chinese oversupply is unlikely to wane on a secular basis and may get worse before it improves if Chinese construction continues to decline.

Apple generates almost 19% of revenue from Greater China. The share extended its decline today as it reverts towards the trend mean.