China Builders Tap Local Bonds at Record-Low Rates on Easing

This article for Bloomberg News may be of interest to subscribers. Here is a section:

Combined bond maturities in onshore and offshore markets for the sector amount to $76.5 billion through the end of 2019, according to data compiled by Bloomberg. Builders are expected to tap both markets to meet the refinancing needs.

"We expect onshore issuance will remain strong after a pick-up in recent months," said Franco Leung, property analyst at Moody’s Investors Service. "Offshore issuance slowed recently, but we expect issuers will continue to tap the offshore bond market given the maturity walls in the coming 6 to 12 months.”

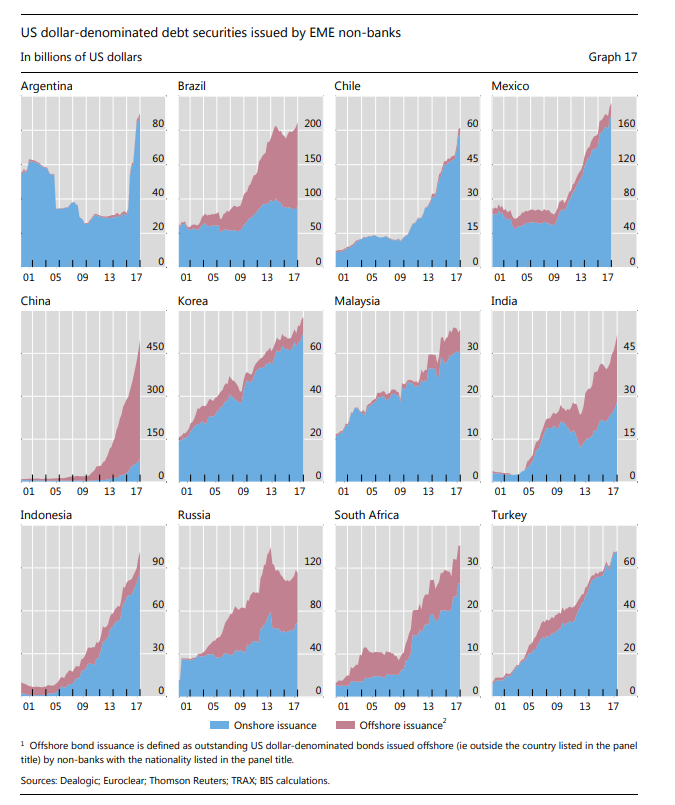

China came down hard of local currency debt issuance from 2015 when it looked like the pace of property market price appreciation was going to cause a bubble from already elevated levels. That action was the causal factor behind the growth of the shadow banking system and the massive growth in foreign debt sales.

This graphic from the IMF highlights that China has the largest outstanding quantity of foreign currency debt. When measured against the size of its economy that figure is not considered as challenging as Turkey’s. Nevertheless, $450 billion is a considerable sum to have accrued in so short a time and with China permitting defaults the success of the newly permitted onshore debt sales will be important to manage the exposure of domestic property companies.

The Shanghai Property Index has paused over the last six weeks but needs to sustain a move back above the trend mean to signal a return to demand dominance.