Carney to Put Pen to Paper as U.K. Inflation Climbs Above 3%

This article by David Goodman for Bloomberg may be of interest to subscribers. Here is a section:

The latest data mean Carney has to write to Chancellor of the Exchequer Philip Hammond explaining why inflation is more than 1 percentage point away from the official 2 percent target.

The letter will be published alongside the BOE’s policy decision in February, rather than this week, as the Monetary Policy Committee has already started its meetings for its Dec. 14 announcement.

Markets expect no further rate increases until late 2018, a view echoed in a survey of economists published Tuesday.

Bloomberg Economics sees the benchmark, currently at 0.5 percent, staying on hold for all of next year.

What Our Economists Say: “Inflation bounced higher in November, but only because of the extremely volatile price of flights. The Bank of England won’t lose much sleep over it. The governor was expecting to write a letter of explanation to the chancellor at some point and the story is simple. Inflation is peaking, it’s set to fall back toward the 2 percent target next year and action has been taken to help it stay there.”

While some BOE officials say they are seeing early signs of a pickup in wage growth, a report on Tuesday offered a gloomier assessment, predicting that pay increases will fall short of inflation again. Recruitment firm Korn Ferry said Britons’ real wages will drop 0.5 percent next year, lagging behind a global average of a 1.5 percent gain.

The Bank of England has not been opposed to running inflation a little hotter than headline for the last few years, not least because it helps to erode the quantity of outstanding debt. Carney has been quite vocal in stating that living standards would be impacted by the Brexit decision and the slow pace of wage growth against a background of quickening inflation is a testament to that.

The devaluation of the Pound between 2014 and 2016 sheltered the UK economy from a deeper economic impact as uncertainty reigned. However, since the economy has steadied and with less uncertainty, as the Brexit negotiations wind their way through approval in Parliament, the argument for allowing inflation to run hot is likely to come under question.

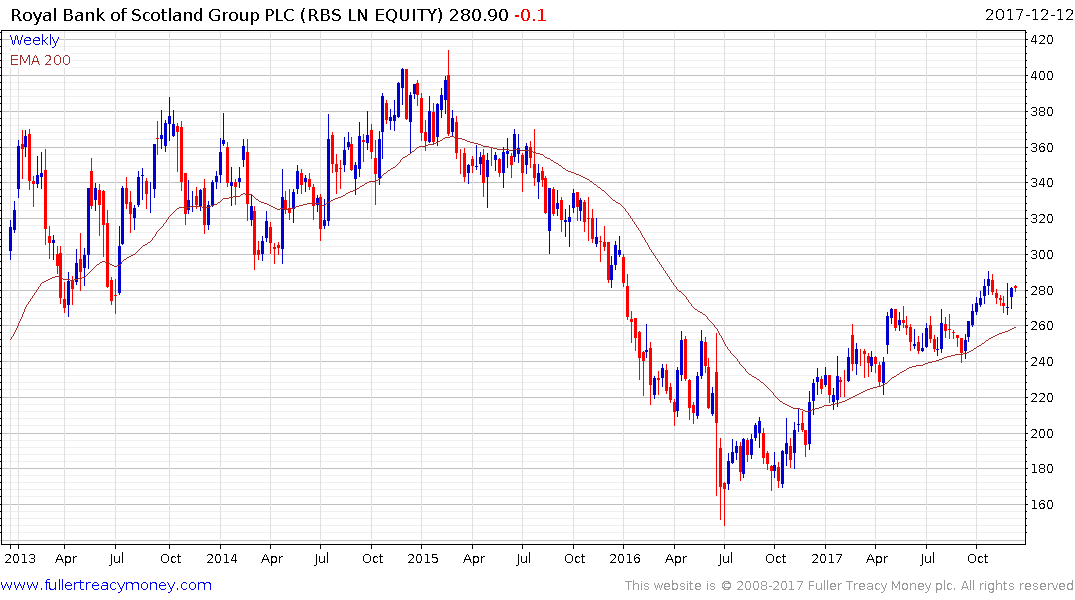

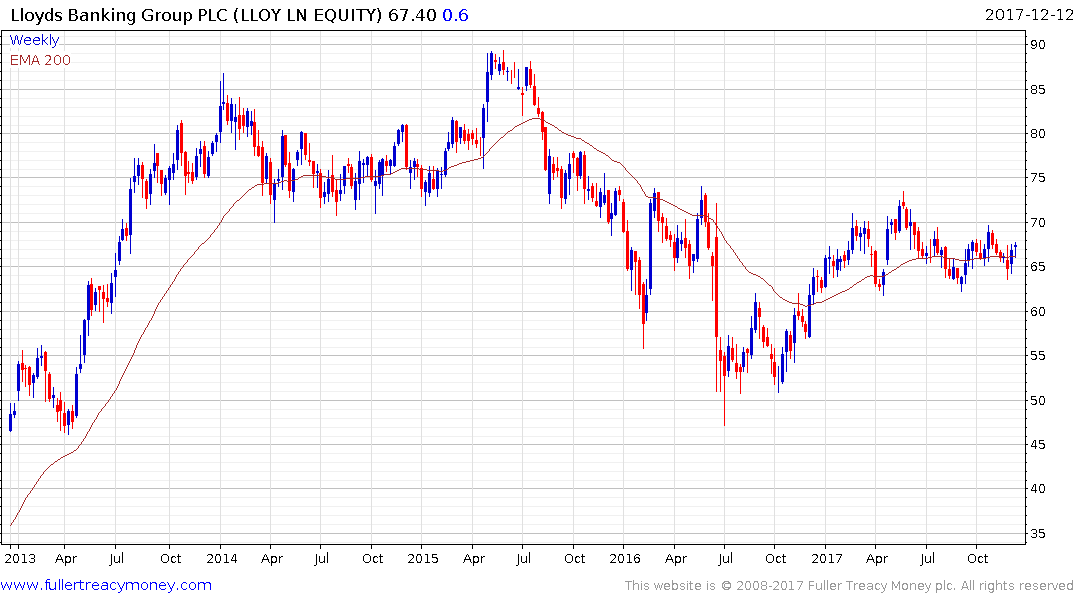

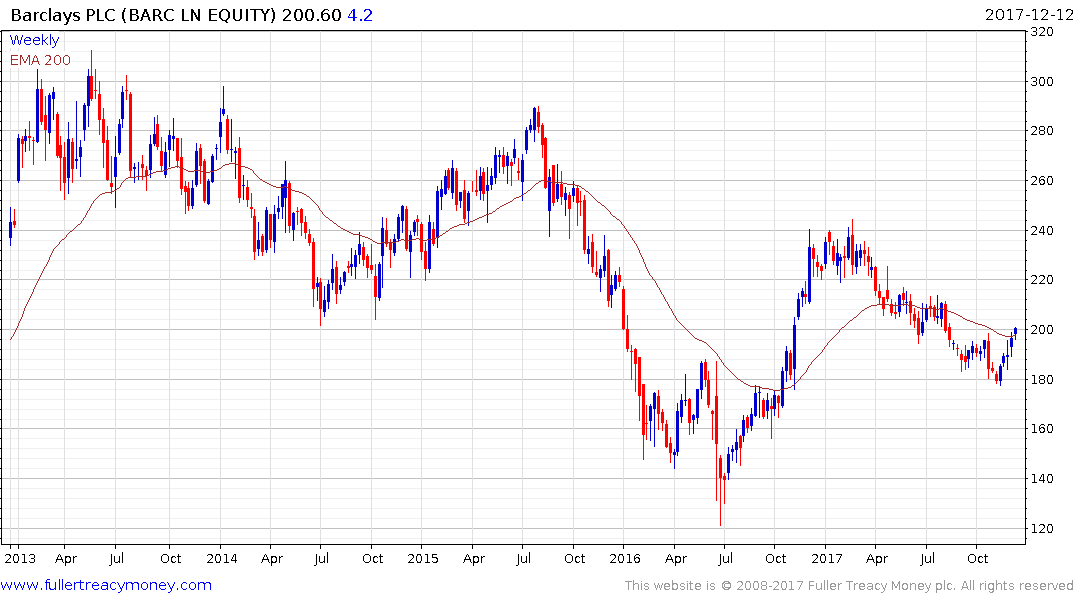

It remains my view that while the USA has been first major economy to raise interest rates, the UK will probably be second. That is positive for the banking sector and the FTSE-350 Banks Index is firming from the region of the trend mean as it continues to test the upper side of a developing eight-year base formation.

RBS (Est P/E 12, DY N/A) has held a progression of higher reaction lows since the spike lower in June 2016, following the Brexit vote, and firmed again today from the upper side of the May-October range.

Lloyds (Est P/E 8.64, DY 4.01%) has held a progression of higher reaction lows this year and is firming from the most recent one at present.

Barclays (Est P/E 13.2, DY 1.5%) rallied this week to break this year’s progression of lower rally highs and will need to sustain a move above 250p to break the medium-term downward bias.

HSBC (Est P/E 15.18, DY 5.23%) bounced last week from the region of its trend mean and is testing the upper side of an eight-year range.

Standard Chartered (Est P/E, DY %) has been largely rangebound this year. The bank has considerable exposure to the commodity sector and is firming at present as interest in mining shares returns.

CYBG Plc (Est P/E 14.29, DY 0.30%) broke out of its post-IPO range in October and continues to extend its advance.

Metro Bank (Est P/E 142.99, DY N/A) is bouncing from the region of its trend mean.