Bond Bears Dust Off Debt Insurance on Wave of Corporate Pain

This article by Katie Linsell for Bloomberg may be of interest to subscribers. Here is a section:

“There are many people now focusing on single-name distressed situations rather than doing plain-vanilla index trades,” said Jochen Felsenheimer, the Munich-based managing director of XAIA Investment GmbH. “There are lots of idiosyncratic situations rather than systematic triggers.”

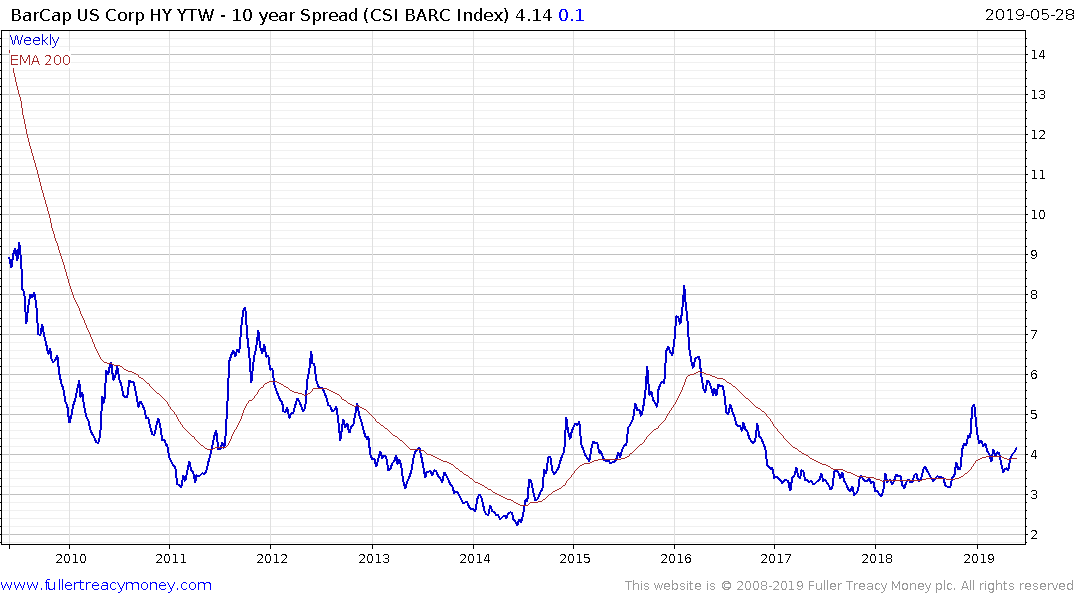

Distressed situations are increasing as companies struggle to manage the debt piles they built up during years of largesse. The cost of insuring such companies is surging, with swaps on some of Europe’s riskiest names costing thousands of basis points compared to about 300 basis points for the region’s high-yield benchmark.

Investors are paying up for protection amid speculation they’ll cash out when companies collapse. Moody’s Investors Service forecasts the speculative-grade default rate in Europe will nearly double to about 2% next year from 0.9% in April.

“Defaults are still quite low, but swaps are definitely more relevant today than they were a few years ago,” said Justin Jewell, senior portfolio manager at BlueBay Asset Management in London. “For funds that have the flexibility, these tools are becoming effective again.”

The manner in which intangibles have been squeezed out of the valuation of major companies like Kraft Heinz, General Electric and Tesla represent significant changes in the way the prospects for companies is being assessed by the debt markets. That change is a factor of tightening liquidity conditions particularly last year but the strength of the Dollar remains an inhibiting factor to global liquidity this year.

High yield tends to trade like equity and issuers are very interest rate sensitive. This report from Moody’s highlights the fallen angel risk in the lowest rung of investment grade debt. Here is a section:

Fallen Angel risk is rising in global fixed income markets, and unanticipated Fallen Angel downgrades have material adverse consequences for fixed income portfolios. We validate the use of the Moody’s Analytics Deterioration Probability (DP) metric for early detection of Fallen Angel downgrades, and find the tool to be useful for this purpose. Simply strategy backtests based on DP sorts reveal that low DP investment grade bond portfolios in the US and Europe have tended to outperform high DP bond portfolios through the business cycle, with outperformance concentrated in periods of market stress.

Private equity has upwards of $3 trillion in dry powder assets salted away for a looming fallen angel scenario where companies will do whatever is necessary to save their investment grade ranking, including disposing of prize assets; like General Electric did. That also suggests there are going to be very attractive distressed opportunities in the credit markets as they opportunities are explored by short sellers.

Back to top