Bill Gross Says Tough Time for Bonds If Fed Relies on Jobs

This article by Sabrina Willmer for Bloomberg may be of interest to subscribers. Here is a section:

Bill Gross says bonds will have a tough period ahead if the Federal Reserve relies on job growth as a critical measure for raising interest rates.

After a Labor Department report today showed that payroll growth surged in December to 292,000, Gross said it appears that the Fed is on track to raise rates three or four times this year, based on statements from policy makers.

"If the Fed continues to believe jobs are a critical element as opposed to aggregate demand and global growth, bonds have a sad period ahead of them," Gross, the lead manager of the $1.3 billion Janus Global Unconstrained Bond Fund, said in a Bloomberg Radio interview.

The Federal Reserve raised interest rates in December for the first time in almost a decade after a strong year of job growth. Payrolls increased by 2.65 million last year compared with 3.1 million in 2014 -- the best back-to-back years for hiring since 1998-99. The central bank is counting on job growth leading to increases in worker pay and inflation.

"The Fed does believe that jobs and the unemployment rate is critical to future inflation over the medium term," Gross said. "So the three or four Fed steps that Stan Fischer and Janet Yellen seem to confirm are probably on track, at least in their verbiage."

Gross said he doesn’t think it’s possible to raise interest rates by 100 basis points in today’s levered global economy, in which the dollar is rising and hurting companies in emerging markets. Bonds will be stable if the Fed only raises interest rates one or two times over next 12 months, said Gross.

The first question is whether the Fed will raise rates four times this year the second is do they intend to raise them four times in 2017 as well?

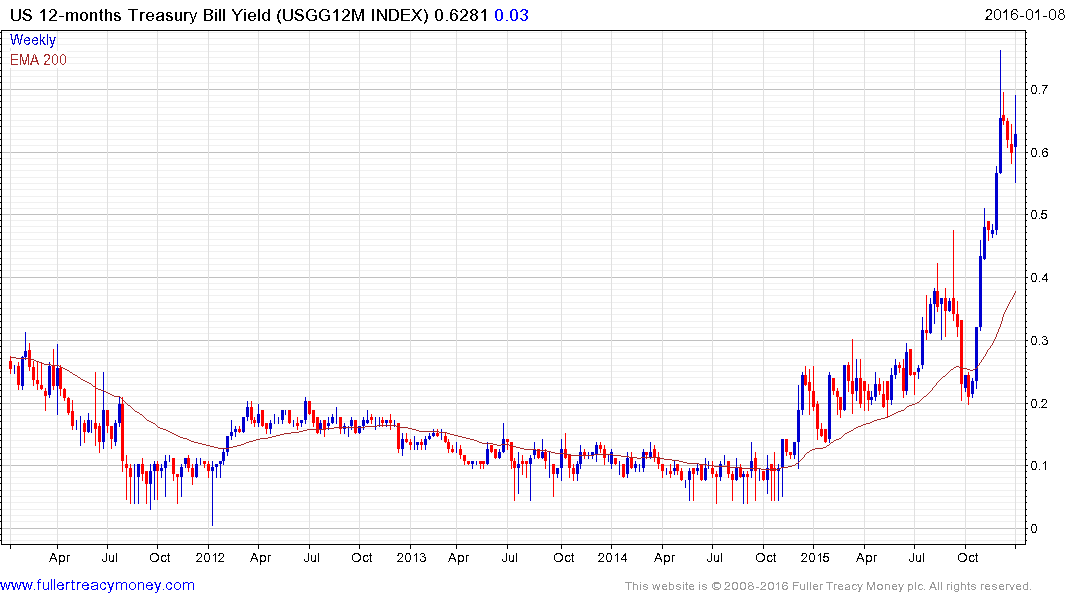

The bond market is telling us investors do not believe the Fed will be able to raise rates at such an ambitious pace not least because of the influence that will have on the ability of foreign companies to fund repayments of Dollar loans they took out over the last decade of a weak greenback. This has an issue we have been discussing for nearly 18 months now and the low level of commodity prices represents an additional headwind to many debt issuers in emerging markets.

12-month yields are reflecting expectations that there will be fewer than two more interest hikes this year not four. There is a certain amount of cat and mouse to this argument because if the impact on the global economy of a strong Dollar is so deleterious then the Fed will not be able to raise rates, and may even have to reverse course, the Dollar’s advance will slow down. If on the other hand the situation is not as severe as some of the most bearish prognostications believe then the Fed will persist in raising rates and US economic pre-eminence will be even more exaggerated in what is likely to remain a volatile environment overall. On aggregate we have to conclude that a choppy environment is more likely than not in either scenario.

Right now the Dollar Index is ranging below the psychological 100 level but despite some respite this week, a sustained move below the trend mean, currently near 96, would be required to question the medium-term upward bias.