Befuddled by the Bull? The Primacy of Free Liquidity and Risk-Love

Thanks to a subscriber for this report from Bank of America/Merrill Lynch which may be of interest. Here is a section:

Here is a link to the full report.

Some of the topics discussed include:

We prefer indicators that have predictive power in ascertaining stock market moves, not contemporaneous indicators like earnings growth that can be more prone to human error. So, what are these? Sentiment / market ownership and free liquidity. When sentiment / market ownership - proxied by the market cap / M1 ratio - is in the lowest, depressed quintile, global equities rally 11.1% in the following year. Conversely, when market ownership is euphoric in the highest quintile, forward global equity returns one year later are only 6.5%, on average. Similar predictive results are obtained for G7 and Asia/EM equity markets.

When free liquidity, the excess growth of M1 over nominal economic growth, is abundant in its top quintile, global equity returns are a juicy 11.2% (and emerging equities, 22.4%) Conversely, when free liquidity is scarce, sucked up by a roaring economy, forward global (and emerging markets) equity returns are 2.6% (and 13.4%).

We think the current puzzlement at rising markets and deteriorating “fundamentals”, i.e. earnings growth, reflects a standard, recurring error in financial markets: of underestimating the predictive power of initial sentiment / positioning and free liquidity in driving markets, especially at turning points. And, an over-reliance on using earnings growth to explain markets. The misguidedly confident man with an impaired hammer isn’t likely to get much carpentry done.

Further, markets tend to led economic data at turning points. For instance, in the US, at the bottom of the cycle, the market (S&P 500) leads the economic data (US ISM) by 3- months on average, with an average return of 12% between the market bottom and the economy trough. In practice though, analysts need more time to confirm that growth (US ISM) has troughed, and may miss out more of the rally

Liquidity/sentiment first, fundamentals later. Unsurprisingly, at these turning points, market cap swells up by about 25% on average from the market lows over the next 6-months – of this, about 19% can be attributed to sentiment, 15% to liquidity expansion, while growth shaves off 4%. As we stretch to longer horizons, growth becomes more and more significant in explaining stock market returns (see Table 1 on page 2).

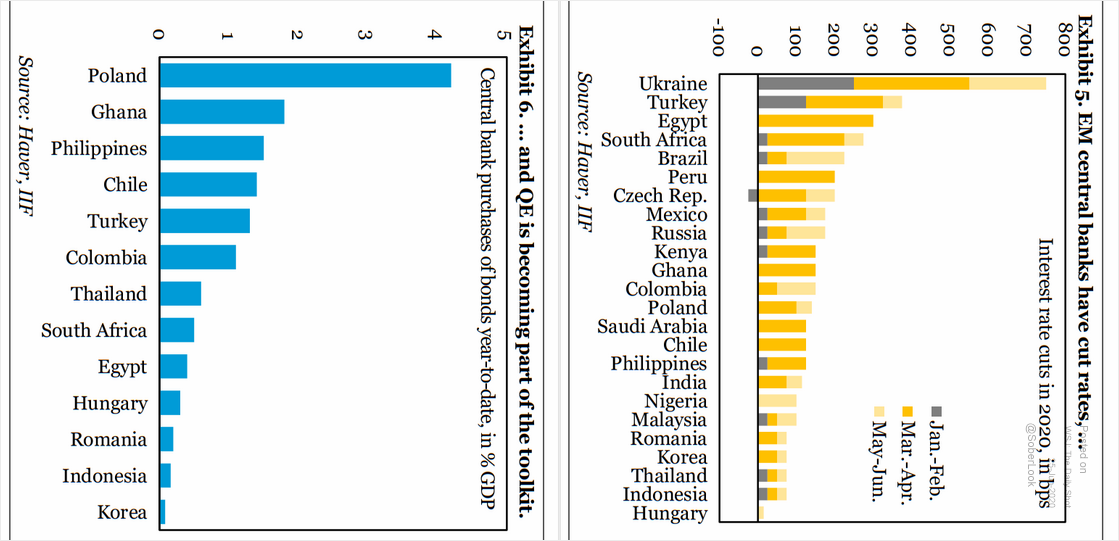

The biggest existential question in financial markets today is how likely are global interest rates to trend towards zero in aggregate. To date the Anglosphere countries have been adamant in their determination to avoid negative interest rates.

However, there is no avoiding the fact that interest rates are falling all over the world. Additionally, Poland, Ghana, Philippines, Chile, Turkey, Colombia, Thailand, South Africa, Egypt, Hungary, Romania, Indonesia and South Korea are all now engaged in quantitative easing.

That is setting off a scramble for positive yielding bonds with a reasonable credit rating which is compressing yields for just about everything. The 137-basis point pickup from investing in equities over Treasuries is a siphoning money into the stock market.

The challenge is in the timing of the liquidity infusions. The combined central bank balance sheets chart has stopped rising and the pace of announcements of fresh fiscal stimulus has slowed. Investors now have a much better understanding of the relationship between liquidity infusions and stock performance which suggests the arbitrage is narrowing which exaggerates the dependency on fresh infusions.

The 30-year Treasury yield broke its sequence of higher reaction lows today which suggests additional willingness to price in deflation rather than an inflationary outcome.