Barron's 2016 Roundtable, Part 1: A World of Opportunities

Thanks to a subscriber for this transcript of a panel discussion between a number of high profile analysts. Here is a section:

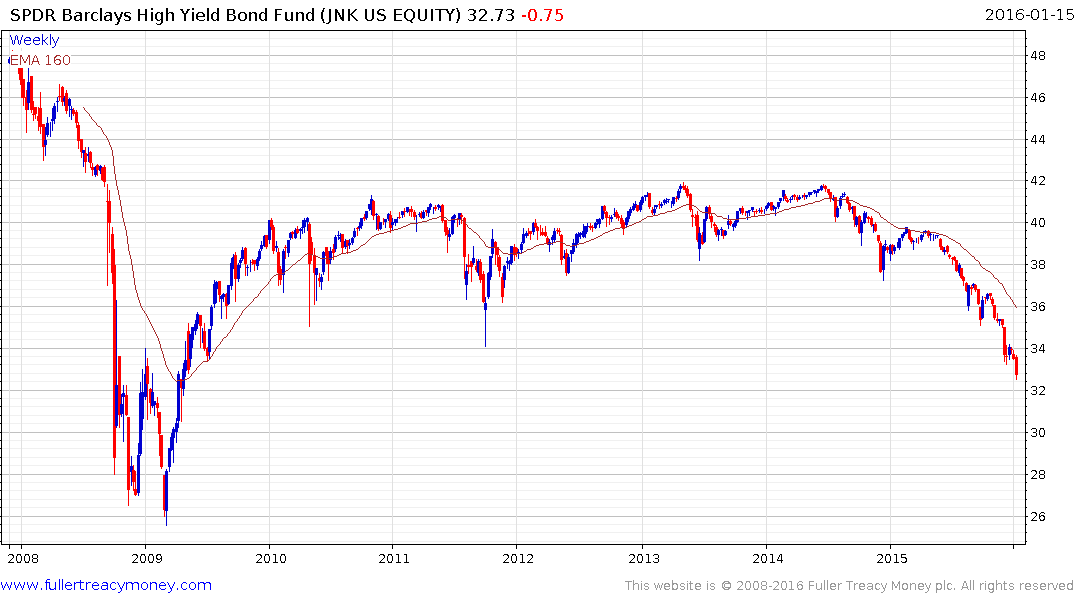

We will see a higher default rate in the junk-bond market. Junk-bond issuance used to represent about 1% of GDP. Then it rose to 2%. It was something of a stimulant to the economy. Also, the stock market has been buyback-driven to an extent, and higher borrowing costs will make that more problematic.

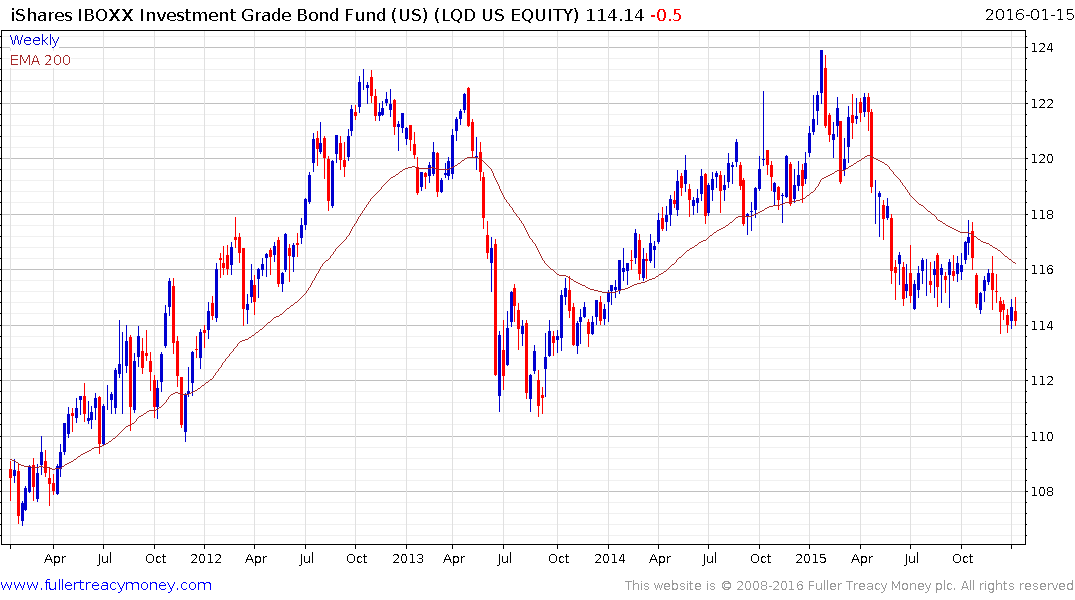

Investment-grade bonds also have been dropping in value. The LQD [ iShares iBoxx $ Investment Grade Corporate Bond ETF] consistently dropped in price through 2015. When interest rates rose, it was challenged by interest-rate risk. When the world looked problematic, it was challenged by credit risk. It seems like there is almost no way to win. When investment-grade credit is downgraded, it falls into junk territory, which makes it un-ownable for a large number of institutional investors. The credit market is sending a message, and the stock market, at least until recently, was whistling through the graveyard. When junk bonds fall 20% in price and the stock market sits at a high, something is wrong with the picture. These markets are moving like alligator jaws. Ultimately, they will move together.

Here is a link to the full report.

There are undeniable problems in the energy sector and this is all the more important because it has been one of the primary sources of new debt over the last five years. With prices where they are today, the prospect of an uptick in the default rate is non-trivial. That’s a problem, particularly for bond ETFs, because they cannot arbitrarily sell and will need to wait for a downgrade or other mandated event to occur before they liquidate. This means they will invariably be late.

LQD has not fallen to the same extend as high yield funds such as JNK but the trend remains downward. An uptick in the default rate would move the risk metrics for bond investors and would contribute to additional underperformance. Against a background where bond yields hit medium to long-term bottoms in the last three years that is unlikely to be good news for passive bond funds generally.

.png)

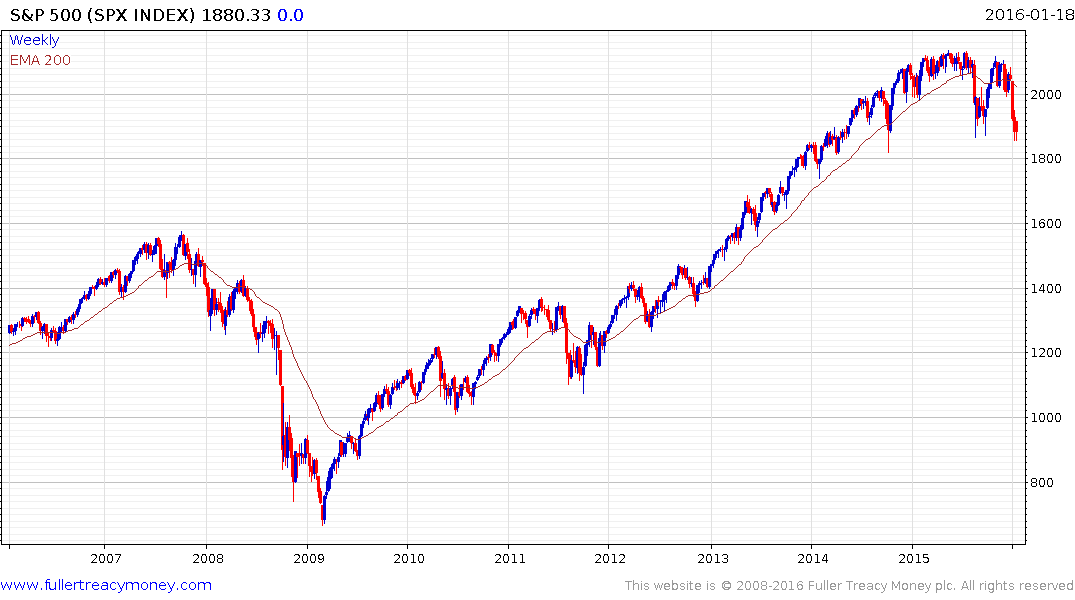

The chart of corporate profits overlaid with the S&P500 highlights the fact that corporate profits tend to peak about a year before the stock market. It is only updated through the end of September but the media have so far been reporting disappointing figures for the fourth quarter. Against that background the ability of the Fed to continue to raise interest rates has to be questioned.

The S&P 500 continues to test the region of the August lows but a clear upward dynamic, similar to those posted in August and September and held for more than a day or two, would be required to signal short covering and a possible reversionary rally.