Banks Are Now Too Scared to Even Make Money

This article by James Mackintosh for the Wall Street Journal may be of interest to subscribers. Here is a section:

In both cases, those shifting money across borders want to avoid foreign exchange risk, so they hedge using basis swaps. These involve swapping yen or euros in exchange for dollars, which will be swapped back at the end of the contract at the forward rate, typically a year or more later. Meanwhile they pay each other interest at the Libor rate for their currency, plus (or minus) the basis, which moves with demand.

Without banks willing to take the other side of the trade, the basis has blown out to levels usually only seen when the financial system is in meltdown, as in 2008-9 after Lehman or in 2011-2 as the euro seemed to be failing.

Most investors care as much about basis swaps as they do about cash-settled butter futures, but the shifts in the basis have already had highly visible effects. U.S. companies now have little reason to issue bonds in euros, because the basis cost has risen so much it almost entirely offsets the benefit of issuing at a lower yield in Europe. Japanese investors have no reason to buy U.S. Treasurys, as the extra yield they earn would all be eaten up by the basis when they hedge.

In short, the world’s banks aren't doing what they should be doing to grease the flows of money between countries. They’re too regulated and too scared of the risks, slight as those are.

We should welcome the fact that banks now try to price such risks, rather than the precrisis practice of simply ignoring them, but perhaps they are going too far the other way.

The reorientation of the money markets funds sector due to take place on October 14th has been a contributing factor in the uptick in LIBOR rates seen over the last couple of months. As the above article highlights it is not the only factor.

Cross Currency Basis Swaps represent one of the most expedient ways of hedging currency exposure to interest rates and therefore are a hedged carry trade. LIBOR rates breaking out may be considered one of the unintended consequences of negative interest rates.

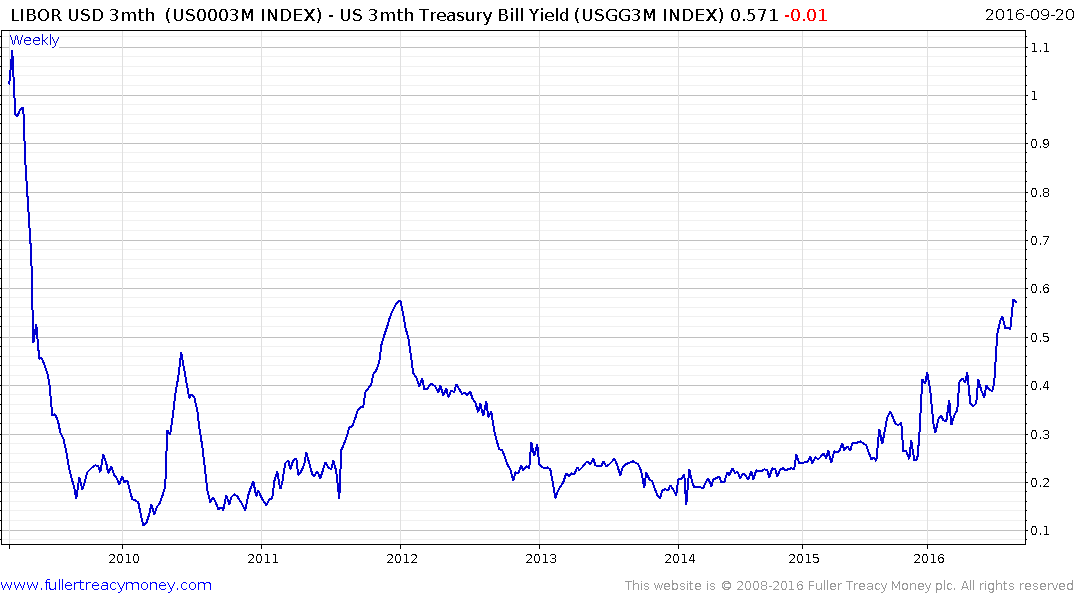

The TED spread (3-month LIBOR – 3-month Treasury Bills) is a measure of the perception of risk in the banking sector because it depicts the pick in yield banks require before they are willing to lend to one another. It is easy to argue that this time is different because the burden of regulation is so onerous that it forces financials to be more cautious and moreover they have to hold more Tier 1 (read government issued) paper. However that does nothing to detract from the fact that if banks are charging more to lend to one another they will want to charge customers more too. As liquidity providers, if banks cannot or will not lend then it imposes greater pressure on central banks to compensate through quantitative easing.

The spread has a rounding characteristic consistent with the view it is likely to move higher over the medium term. This suggests bank lending rates are likely to trend higher over time and a break in the progression of higher reaction lows would be required to question that view. Another way of looking at this spread is that it is a direct response to negative / very low interest rates.

With Wells Fargo’s CEO testifying in front of Congress today, in an attempt to explain the company’s lack of governance and oversight and with Deutsche Bank facing into a lengthy legal battle centred on avoiding a fine that threatens its existence, one might expect that the banking sector would be down more. The S&P500 Banks Index is still trading in the region of the trend mean but the consistency of the 2011-15 uptrend has been lost. The steep drawdown late last year broke the progression of higher reaction lows and it still has a lot of work to do to signal a return to demand dominance beyond near-term steadying.

Banks are in the business of making money. Increasingly stringent regulations across jurisdictions and very low interest rates require higher lending rates in order to preserve margins. That is part of the reason the banking sector is impatient with the Fed about the pace of short-term interest rate hikes. They simply make more money with higher interest rates, but that only applies if they lend which poses something of a catch-22.