Bank Stocks Gain on JPMorgan's Biggest Rally Since November 2020

This article from Bloomberg may be of interest to subscribers. Here it is in full:

JPMorgan Chase & Co. jumped by the most in 18 months as upbeat comments from Chief Executive Officer Jamie Dimon on the US economy and improved guidance helped drive bank shares higher.

Shares of the JPMorgan rose as much as 7.1% on Monday, the most since November 2020, after the start of the company’s investor day, when it boosted its annual forecast for net interest income excluding its markets business and maintained its expense outlook. The KBW Bank Index climbed as much as 4.4%, with Citigroup Inc., Bank of America Corp. and Wells Fargo & Co. all gaining more than 5%.

Wells Fargo banking analyst Mike Mayo said in a note to clients that the biggest takeaway from JPMorgan’s gathering so far is that it shows there’s “no recession imminent.” JPMorgan’s presentation was bullish for the company and “even more so for the industry,” he added.

Bank shares have been under extensive pressure this year as worries that an aggressive series of interest rate hikes by the Federal Reserve could plunge the US economy into a recession. The KBW Bank Index has fallen 25% since hitting a record high in early January.

JPMorgan has been the worst hit among the biggest banking stocks. While Monday’s surge has helped erase some of the decline this year, the lender is still down nearly 22%, making it the worst performing big bank stock. Still, analysts have not given up on the company, with the average 12-month price target forecasting a 23% gain, near the highest it’s been since the pandemic began.

Rising interest rates are generally considered positive for banks because they get to charge more for their services. The challenge today is the spread they rely on to profit has evaporated as the yield curve has flattened. The absolute rate on mortgages also means refinancing income has disappeared on mortgages. That implies banks will probably do better when the yield curve steepens and yields contract.

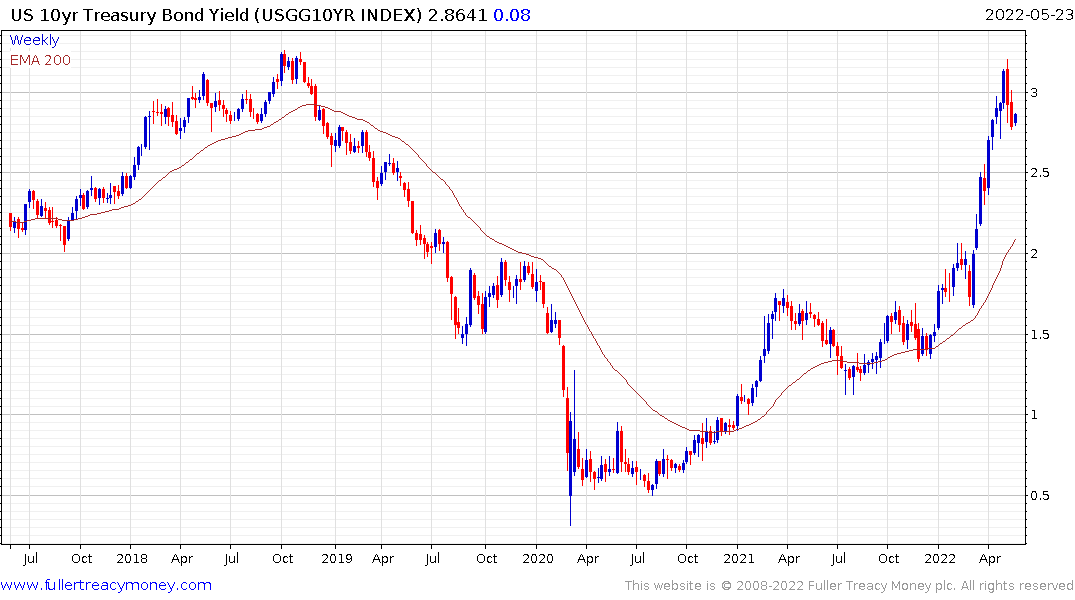

The 10-year yield steadied to push back above the 2.8% level today. The trend is no longer as consistency as during the uptrend but that is being rationalized as a bigger pause in the region of the 2013/14 and 2018 peaks. A sustained move to new recovery highs, above 3.25% will be required to signal a return to supply dominance.

The yield curve remains exceptionally flat.

The Dollar index continues to unwind its short-term overbought condition. That implies investors are more worried about slowing US growth than inflation at present. Stock market investors are betting that will translate into fewer interest rate hikes, so a short-covering rally is beginning to unfold.