Autumn Statement: What the UK's New Budget Means for Your Money

This article from John Stepek may be of interest to subscribers. Here is a section:

On the income side, if you earn more than £100,000, you really should be looking at how to put as much of your salary as you can above that amount into a pension via salary sacrifice. Why’s that? Because contrary to what you might think, you’re not paying a 40% marginal tax rate. As the team at tax advisors Blick Rothenberg point out, your marginal tax rate is in fact closer to 60%, because £100,000 is the point at which your personal allowance starts to get whittled away. (This is also why the 45% rate was cut to £125,140 rather than £125,000 — so that it aligns with the point at which your personal allowance is all gone.)

As a result, any money you can shield from this rate is doing a great deal more work than any other pound you save. That said, given that your mortgage is probably going up, and your heating bill is through the roof, it’s quite possible that you are already doing as much as you can on that front without causing a major liquidity crisis in your household.

On the investment side, falling squarely into the “be thankful for small mercies” category, at least the chancellor didn’t mess around with the annual allowances for tax-efficient “wrappers” — you can still put up to £20,000 a year into an individual savings account, and up to £40,000 a year into a pension (assuming you earn that much each year). The latter of course is still subject to the (frozen) lifetime allowance, so do be careful if you’re in danger of breaching that £1.073 million lifetime cap.

So if you have grown a bit sloppy with your admin, and you are holding any shares outside a tax wrapper (i.e. an Individual Savings Account or a pension), then now is the time to get a handle on that and move them. At least then you’ll be shielded from dividend or capital gains taxes. If you have already exhausted these allowances, you might want to start looking at venture capital trusts or enterprise investment schemes, though those are a topic for another day.

Government rules tend to change investor behaviour. The perversion, that is the tax system, means the incentive to make a lot of money from working is actively under attack. Instead one is being encouraged to invest as much as possible to shield assets from the tax regime. That basically means outsourcing the job of making money to companies rather than individuals. That’s not great news for hard workers, but it certainly benefits the asset management sector.

Meanwhile, many wealthier, mobile investors still avail of the non-domicile rules. The falling tax-free allowance for dividends suggests investors will be eager for buybacks rather than dividend increases and investing outside of a tax favoured structure is even less attractive. This is another example of how the UK economy is dominated by financialization.

The fact spending is only projected to fall after the next election suggests the Conservatives are fully aware the UK public can only take so much pain in one go. It is also a bet that a recovery will be well underway by the time an election needs to be called in early 2025.

The 10-year Gilt yield paused today above the psychological 3% level so we may see some consolidation. Nevertheless, there is clear scope for yields to contract further as the economic toll of fiscal consolidation becomes evident next year

The 10-year Gilt yield paused today above the psychological 3% level so we may see some consolidation. Nevertheless, there is clear scope for yields to contract further as the economic toll of fiscal consolidation becomes evident next year

The Pound continues to pause at $1.20, which is the lower side of the overhead five-year range and coincides with the region of the 200-day MA.

The FTSE-250 is pausing in the region of the 200-day MA as it challenges the medium-term sequence of lower rally highs. It will need to sustain a move up through the psychological 20,000 level to signal a return to demand dominance beyond short-term steadying.

The FTSE-250 is pausing in the region of the 200-day MA as it challenges the medium-term sequence of lower rally highs. It will need to sustain a move up through the psychological 20,000 level to signal a return to demand dominance beyond short-term steadying.

The AIM100 Index is still in a consistent downtrend and pausing at the lower side of the overhead range at present. Prices today are back where they traded in for much of the last decade so a lot of bad news has been priced in even if there is no clear evidence of bottoming activity just yet.

The AIM100 Index is still in a consistent downtrend and pausing at the lower side of the overhead range at present. Prices today are back where they traded in for much of the last decade so a lot of bad news has been priced in even if there is no clear evidence of bottoming activity just yet.

Abrdn (Aberdeen Asset Management) rallied last week to emphatically break the almost two-year downtrend.

Abrdn (Aberdeen Asset Management) rallied last week to emphatically break the almost two-year downtrend.

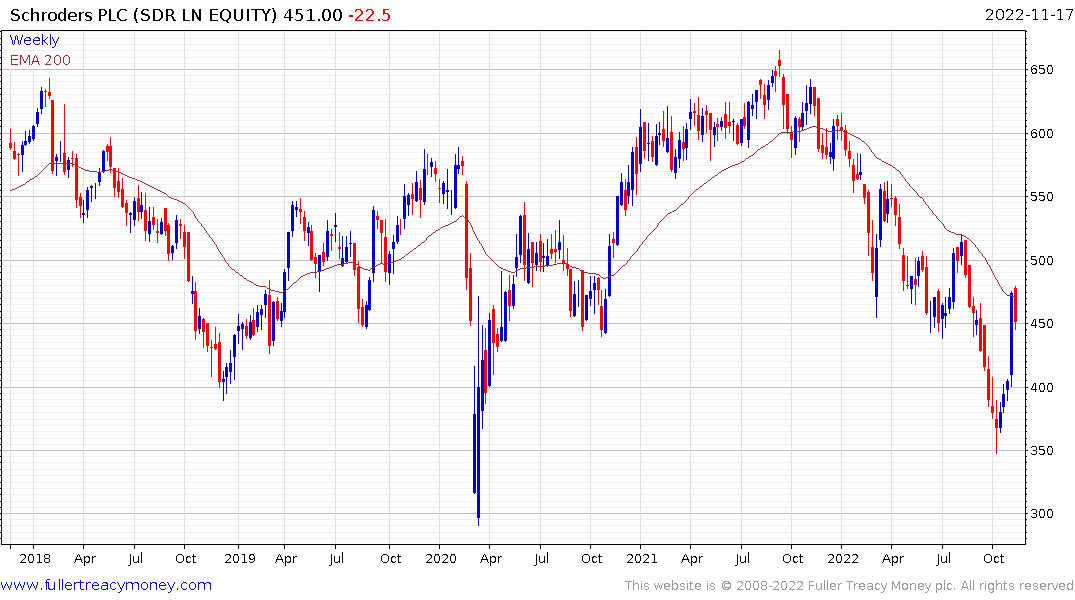

Schroders has a broadly similar pattern to the FTSE-250.

Schroders has a broadly similar pattern to the FTSE-250.