ASML Profit Rises, Company Maintains Sales Forecast and Intel's Fourth-Quarter Revenue Forecast Tops Analyst Estimates both from Bloomberg may be of interest to subscribers. Here is a section from the latter:

Intel Corp., the world's biggest chipmaker, predicted fourth-quarter sales that beat analysts' estimates, helped by demand in emerging economies.

Revenue this period will be $11.4 billion, plus or minus $400 million, Santa Clara, California-based Intel said yesterday in a statement. That compares with an average projection of $11.3 billion, according to data compiled by Bloomberg.

Corporations and households in less developed markets bought more computers, helping Intel weather slumping demand among consumers in the U.S. and Europe, Intel Chief Financial Officer Stacy Smith said in an interview. The results bode well for computer makers, including Dell Inc. and Hewlett-Packard Co., which also benefit as businesses upgrade dated machines.

"It's clearly a positive for those companies in the PC and enterprise space," said Pat Becker Jr. of Becker Capital Management Inc. in Portland, Oregon. The company owns shares of Intel as part of the $2.2 billion it oversees. "The margins in that help overcome some of the weakness we've seen in the consumer in August."

The last four weeks of the quarter were better than the company predicted, Smith said on a call with analysts. That improving demand was the basis for the company's predictions for the fourth quarter. Component inventory remains "lean" throughout the computer supply chain, he said.

Eoin Treacy's view The technology sector is one of the prime beneficiaries of lower interest rates,

a weak Dollar and growth in the global middle class. Intel, while not currently

among the leaders, is a useful barometer for the technology sector generally

and the fact that its earnings are coming in ahead of estimates can be viewed

as a positive. Chip manufacture will always feature highly in the technology

sector but is currently being overshadowed by the growth of cloud computing.

(Also see Comment of the Day on September

23rd)

Broadly

speaking, Intel remains in a decade long

base formation which will not be completed until it sustains a move above $27.

In the meantime, it encountered resistance below $25 from April and remains

in a six-month downtrend. It found at least short-term support in September

and the current rally is about the same size as that posted in July. It is testing

the 200-day MA and needs to hold a move above $20 to indicate demand is regaining

the upper hand beyond the short term.

ASML

was a stronger performer from the 2008 lows but also pulled back from its April

high. It found support in the region of €20 from early September and a

sustained move below hat level would be required to question scope for further

higher to lateral ranging.

Citrix

System which has been leader in the cloud computing had accelerated well

away from its 200-day MA by late September and pulled back abruptly last week.

It is beginning to lose downward momentum and while an upward dynamic would

help to confirm the return of demand, the share may be coming back into a medium-term

buying range.

BMC

Software is pulling away from the $40 area and a sustained move below that

level would be required to question medium-term upside potential.

Check

Point Software hit a new 8-yr high three weeks ago, completing the 1st step

above its base. A sustained move below

the 200-day MA, currently near $33.50 would be required to question medium-term

upside potential.

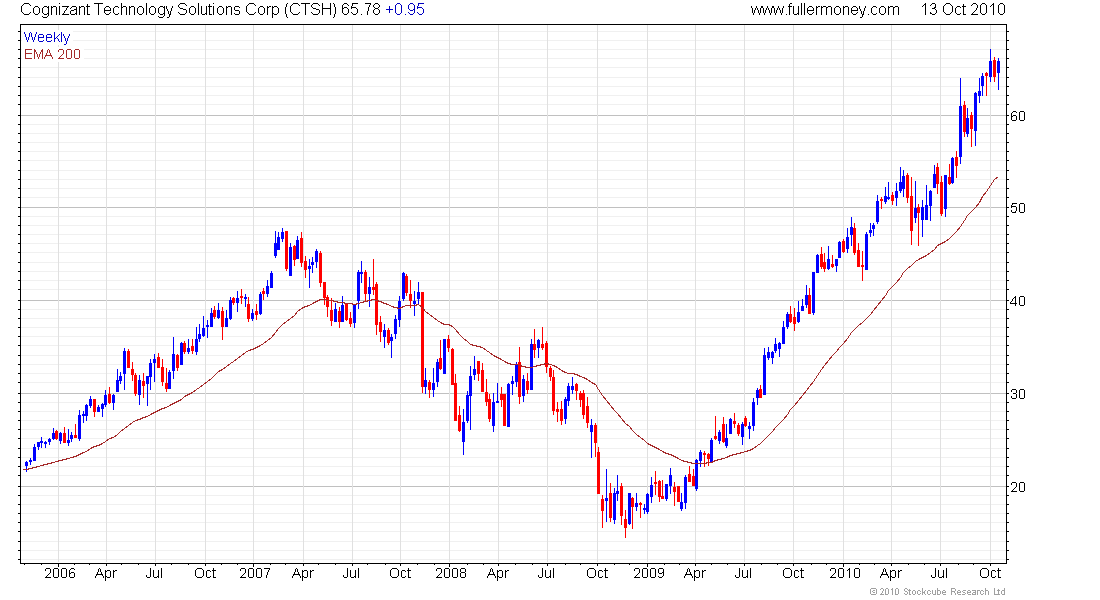

Cognizant

Technology Solutions Corp remains in a consistent two-year uptrend and while

somewhat overbought at the moment, a sustained move below the 200-day MA, currently

near $53.50 would be required to question medium-term upside potential.

Oracle

continues to hold the breakout to new medium-term highs and a sustained move

below the 200-day MA, currently near $24 would be required to question medium-term

upside potential.

Juniper

Networks remains in a long-term base.

The $32 area, which it is currently testing, has been an area of resistance

for much of the last decade and a sustained move above that level would increase

potential that demand is returning to medium-term demand dominance.

Amazon continues to sustain the breakout

from the yearlong range and a sustained move below the 200-day MA, currently

near $130 would be required to question medium-term upside potential.

Google

broke back above the 200-day MA in September and continues to advance. A sustained

move below the psychological $500 level would be needed to check near-term scope

for further upside.

This link to

IBM's cloud computing discussions may be of interest to subscribers. The share

broke upwards to new highs last month and a sustained move back below $130 would

be required to question medium-term upside potential.

Apple

has also sustained the breakout from the five-month range and would need to

sustain a fall below $250 to question the consistency of the medium-term uptrend.

{kind=link}