America's Roster of Public Companies Is Shrinking Before Our Eyes

This article by Maureen Farrell for the Wall Street Journal may be of interest to subscribers. Here is a section:

The number of U.S.-listed companies has declined by more than 3,000 since peaking at 9,113 in 1997, according to the University of Chicago’s Center for Research in Security Prices. As of June, there were 5,734 such public companies, little more than in 1982, when the economy was less than half its current size. Meanwhile, the average public company’s valuation has ballooned.

In the technology industry, the private fundraising market now dwarfs its public counterpart. There were just 26 U.S.-listed technology IPOs last year, raising $4.3 billion, according to Dealogic. Meanwhile, private U.S. tech companies tapped the late-stage funding market 809 times last year, raising $19 billion, Dow Jones VentureSource’s data show.

Private funding markets have taken on attributes of public equity, such as an ability to hand employees shares they can trade. Airbnb Inc.’s recent $850 million funding round, which valued the home-rental company at $30 billion, enabled employees to sell $200 million of stock. Investors, particularly in late-stage funding rounds, now often have a better view of a private company’s financials than they used to, including through quarterly conference calls.

“There’s no great advantage of being public,” says Jerry Davis, a professor at the University of Michigan’s Ross School of Business and author of “The Vanishing American Corporation.” “The dangers of being a public company are really evident.”

There have been two important themes that have shaped the view going public is not the most worthwhile exercise for new companies. The overbearing nature of regulatory requirements has increased substantially over the last decade, not least in response to the financial crisis, and this represents a significant cost for public companies which private companies avoid. It is quite simply a hassle for small companies to go through the motions of preparing earnings reports on a quarterly basis and formulating them in such a way as to be amenable to analysts.

In the past companies had no choice but to accept the downside of gaining access to the capital markets but that is no longer the case. Extraordinarily low interest rates, massive availability of capital and institutional investors hungry for both diversification and yield have created a fertile alternative environment for private companies to source capital. The prospect of higher interest rates and a more competitive yield environment generally threaten that cosy relationship.

I am keeping an eye on news headlines relating to the success or otherwise of funding rounds for private companies. It they encounter difficulty sourcing enough funding privately they will need to list, and that would represent a new source of supply in the market.

While writing Crowd Money I created this chart of US Short Interest / US Short Interest as a percentage of Total Shares Outstanding as a proxy measure for the number of shares outstanding on the NYSE. Since we naturally expect supply to increase in line with a bull market it is not surprising that supply was relatively inert while the broad market ranged but broke out in 2014 as perceptions of future potential improved. What is particularly interesting is that the measure hit a peak last year and has declined quite considerably since. That is a bullish signal since it suggests available capital is chasing fewer shares. The reasons behind this phenomenon could be a combination of buybacks, companies being taken private, M&A activity and a dearth of new listings to compensate for those influences.

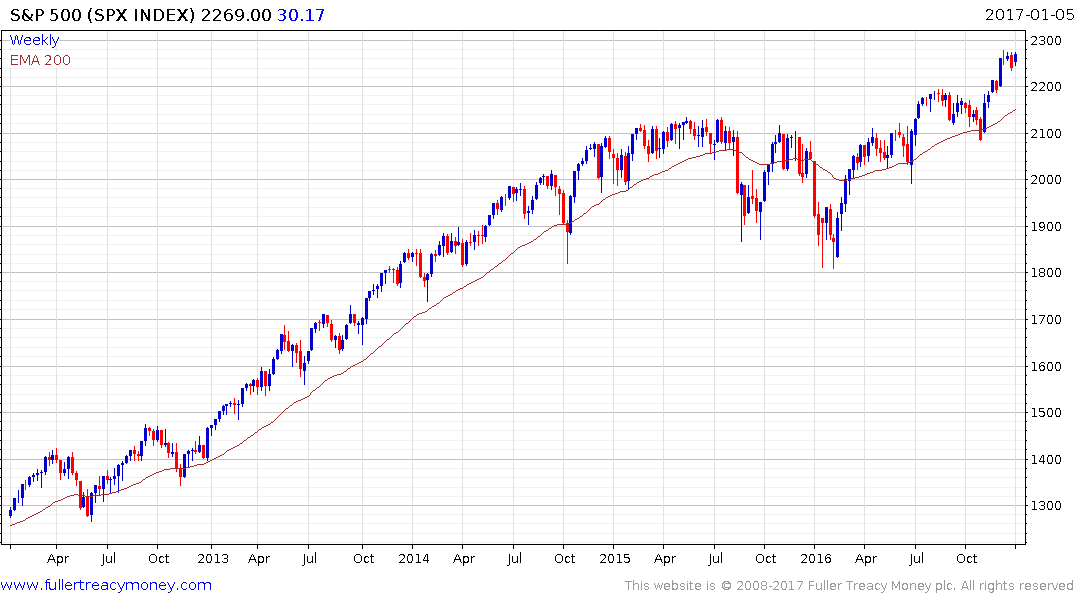

In the meantime the S&P500 remains in a reasonably consistent uptrend and a sustained move below the trend mean would be required to begin to question medium-term scope for additional upside.

Back to top