America's "Retail Apocalypse" Is Really Just Beginning

This article by Matt Townsend, Jenny Surane, Emma Orr and Christopher Cannon for Bloomberg may be of interest to subscribers. Here is a section:

Until this year, struggling retailers have largely been able to avoid bankruptcy by refinancing to buy more time. But the market has shifted, with the negative view on retail pushing investors to reconsider lending to them. Toys “R” Us Inc. served as an early sign of what might lie ahead. It surprised investors in September by filing for bankruptcy—the third-largest retail bankruptcy in U.S. history—after struggling to refinance just $400 million of its $5 billion in debt. And its results were mostly stable, with profitability increasing amid a small drop in sales.

Making matters more difficult is the explosive amount of risky debt owed by retail coming due over the next five years. Several companies are like teen-jewelry chain Claire’s Stores Inc., a 2007 leveraged buyout owned by private-equity firm Apollo Global Management LLC, which has $2 billion in borrowings starting to mature in 2019 and still has 1,600 stores in North America.

Just $100 million of high-yield retail borrowings were set to mature this year, but that will increase to $1.9 billion in 2018, according to Fitch Ratings Inc. And from 2019 to 2025, it will balloon to an annual average of almost $5 billion. The amount of retail debt considered risky is also rising. Over the past year, high-yield bonds outstanding gained 20 percent, to $35 billion, and the industry’s leveraged loans are up 15 percent, to $152 billion, according to Bloomberg data.

Even worse, this will hit as a record $1 trillion in high-yield debt for all industries comes due over the next five years, according to Moody’s. The surge in demand for refinancing is also likely to come just as credit markets tighten and become much less accommodating to distressed borrowers.

One of Warren Buffett’s most colourful adages is “you don’t know who has been swimming naked till the tide goes out” A great many companies have survived with high debt loads because liquidity was abundant, interest rates were at rock bottom levels and access to credit was easy. Until recently, refinancing has been easy which allowed companies to pile on additional debt. An obvious point is that highly leveraged companies are heavily exposed to refinancing issues as interest rates rise.

Coupled with the march of online retail, where many established companies have simply failed to keep pace, the potential for substantial store closures has to be considered realistic. The bigger question is how much of this is already in the price of related shares. For example, Macys has already experienced a steep decline suggesting that while visibility on a recovery strategy is not yet apparent a lot of bad news has been priced in.

It was among the leading performers over the last couple of days and formed an upside weekly key reversal this week. Upside follow through next would signal a low of at least near-term significance. It is trading on an Estimated P/E of 6.27, has a debt to assets ratio of 34%, while the debt to equity is 158%. It is currently trading on a price to book of 1.44.

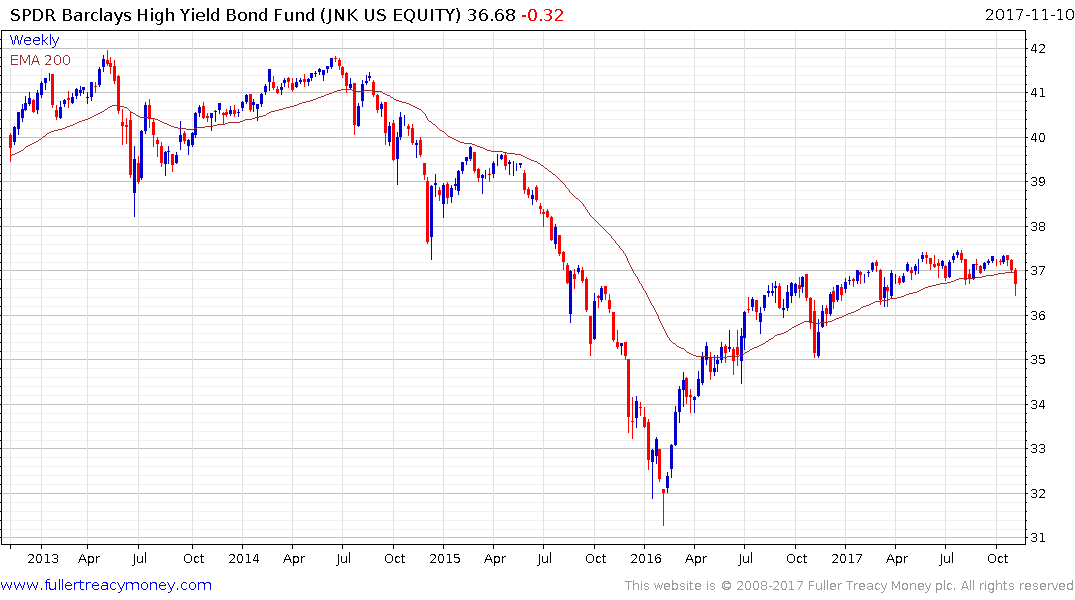

From a broader perspective, if we think about what the most important lead indicators for a recession are: an inverted yield curve, soaring oil prices, widening high yield spreads and unemployment trending higher are at the top of my list.

Right now, interest rates are coming off of very low levels but leverage is high, so markets are sensitive to even small moves. That suggests high yield spreads are likely to be one of the most important markets to monitor because refinancing will be both an influence on spreads as well as suffering a feedback loop from widening.

The Barclays High Yield Spread Index posted a failed downside break this week and is back testing the region of the trend mean. A sustained move above it would signal a return to supply dominance.

Meanwhile the SPDR High Yield ETF (JNK) dropped below the trend mean this week and will need to rebound soon if top formation completion is to be countermanded.