AI and the Big Five

This article from Ben Thompson may be of interest to subscribers. Here is a section:

Indeed, the biggest winners may be Nvidia and TSMC. Nvidia’s investment in the CUDA ecosystem means the company doesn’t simply have the best AI chips, but the best AI ecosystem, and the company is investing in scaling that ecosystem up. That, though, has and will continue to spur competition, particularly in terms of internal chip efforts like Google’s TPU; everyone, though, will make their chips at TSMC, at least for the foreseeable future.

The biggest impact of all though, though, is probably off our radar completely. Just before the break Nat Friedman told me in a Stratechery Interview about Riffusion, which uses Stable Diffusion to generate music from text via visual sonograms, which makes me wonder what else is possible when images are truly a commodity. Right now text is the universal interface, because text has been the foundation of information transfer since the invention of writing; humans, though, are visual creatures, and the availability of AI for both the creation and interpretation of images could fundamentally transform what it means to convey information in ways that are impossible to predict.

For now, our predictions must be much more time-constrained, and modest. This may be the beginning of the AI epoch, but even in tech, epochs take a decade or longer to transform everything around them.

ChatGPT and other artificial intelligence models are growing in capability and the pace of development is accelerating. There is a big question about how consumers will react to intrusive predictive models and how the sector will ultimately be regulated. However, if history is any guide these issues arise after a significant interval and prices move ahead regardless.

NVida is bouncing from the region of the 1000-day MA as it puts in the first higher reaction lows since 2021. There is a possibility that $100 is the low for this correction and if AI represents a new source of demand for its products the base formation development could be shorter than might otherwise be the case.

NVida is bouncing from the region of the 1000-day MA as it puts in the first higher reaction lows since 2021. There is a possibility that $100 is the low for this correction and if AI represents a new source of demand for its products the base formation development could be shorter than might otherwise be the case.

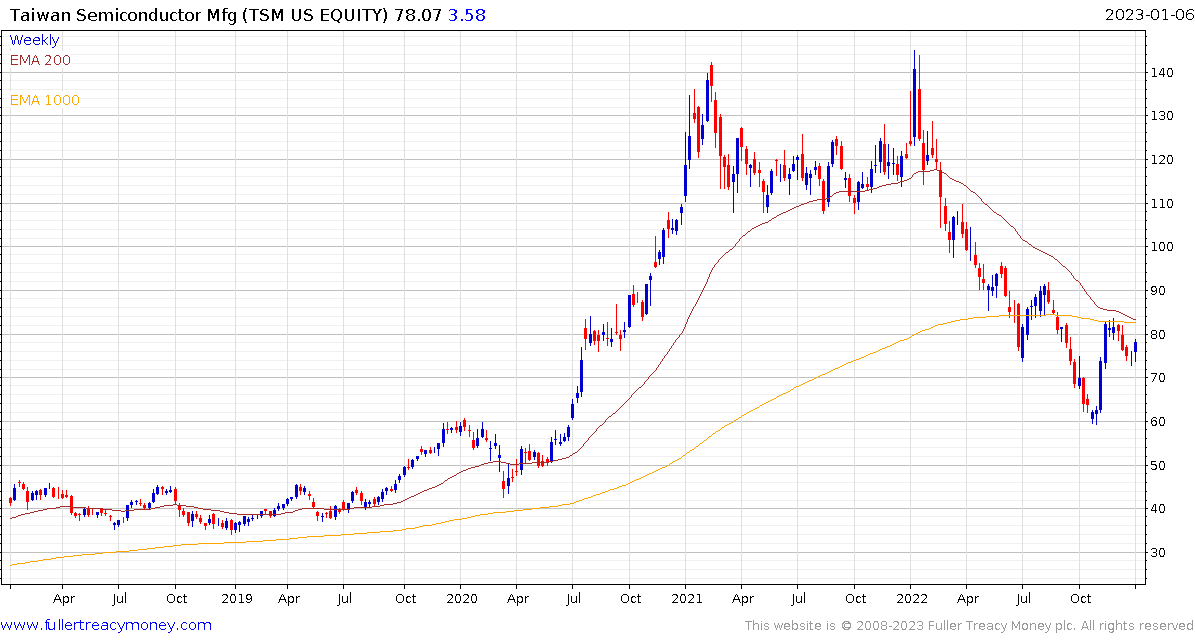

Taiwan Semiconductor is testing the region of both the 200-day and 1000-day MAs. It needs significant new demand to justify investments in new supply so it will likely be a while before the peaks near $140 are surmounted but the lows near $60 may offer a significant area of medium-term support.

Taiwan Semiconductor is testing the region of both the 200-day and 1000-day MAs. It needs significant new demand to justify investments in new supply so it will likely be a while before the peaks near $140 are surmounted but the lows near $60 may offer a significant area of medium-term support.

Meta continues to rebound from its November low but still has quite some way to go before it unwinds the overextension relative to the 200-day MA. Investors do not yet appear convinced the lows are in.

Both Microsoft and Apple continues to steady from the region of their respective 1000-day MAs, while Alphabet is steadying from its November low. Breaks in their medium-term sequences of lower rally highs will be required to confirm more than short-term support building.

Both Microsoft and Apple continues to steady from the region of their respective 1000-day MAs, while Alphabet is steadying from its November low. Breaks in their medium-term sequences of lower rally highs will be required to confirm more than short-term support building.

These charts suggest support building is in its early stages. This is the stage in the cycle where we can expect big swings but less consistent trends as a war goes on between promises about the future and the cost of capital in the present.

.png) Meanwhile, Tesla has been investing heavily in autonomous driving. While this has had limited success, there is no doubt this is an AI heavy project which potentially has alternative uses in picture recognition etc.

Meanwhile, Tesla has been investing heavily in autonomous driving. While this has had limited success, there is no doubt this is an AI heavy project which potentially has alternative uses in picture recognition etc.

The share is very oversold and rebounding from the psychological $100 area. It could double and still only approximate the region of the 1000-day MA.

Back to top