After Brazil, the Deluge? Watch These Nations for Downgrades

This article by Lyubov Pronina for Bloomberg may be of interest to subscribers. Here is a section:

Two weeks after the Latin American country lost its investment grade at one of the three major ratings providers, CDS investors are punishing other emerging markets facing similar challenges, sending their implied ratings at least five levels below their official grades, according to data from Moody’s Corp. Malaysia is A3 at the company, though traders see it six levels lower at Ba3. South Africa, which is a Baa2, is viewed as a B1 borrower. Three Aa3 nations including China are perceived by the markets as deserving the lowest investment grade.

Most developing nations are confronting the same issues that saw Brazil losing its investment-grade rating at Standard & Poor’s -- a plunge in commodity prices, a slumping currency and political turmoil. Sputtering growth in China and the prospect of higher U.S. interest rates are also boosting concern of more downgrades across emerging markets. Having been censured for laxity during previous market meltdowns, the ratings providers won’t want to be caught failing to act this time round, Per Hammarlund of SEB AB said.

“The deterioration in commodity-dependent economies’ credit-risk metrics can lead to more downgrades in emerging markets in the next three to six months, if not earlier,” said Hammarlund, the chief emerging-markets strategist at SEB in Stockholm. “The rating agencies were roundly criticized for being slow to react during the 2008 crisis as well as the 2011 euro-zone crisis. They are going to be much more trigger happy this time.”

The 2037 Brazilian US Dollar denominated benchmark with a coupon of 7.125% traded at a price of 155 at its 2012 peak. It traded below par for the first time since 2009 this week as the outlook for Brazil’s capacity to repay its debts has deteriorated with commodity prices and the realisation that governance has not improved to any measurable extent. The downgrade to junk status by S&P is an important development.

Many globally oriented investment grade bond funds simply cannot hold junk bonds. They may have a decision about whether to hold on to a deteriorating position for the coupon as long as an issuer is investment grade but following a downgrade they have to sell. This creates a panicky environment but from a behavioural perspective we also know that the number of people who still have long positions, purchased at elevated levels, will be fewer than it was only a month ago.

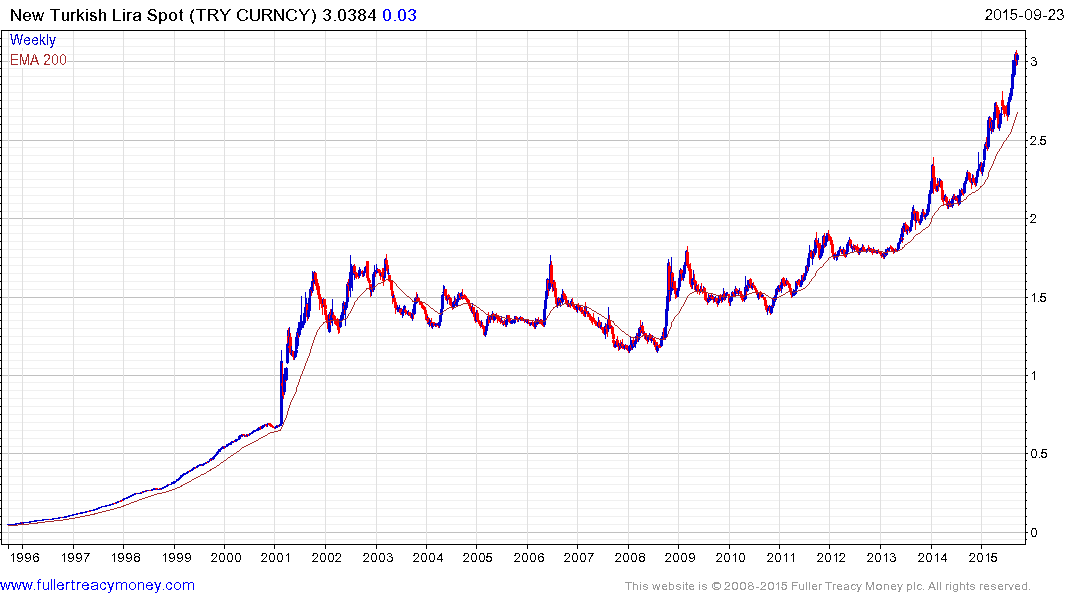

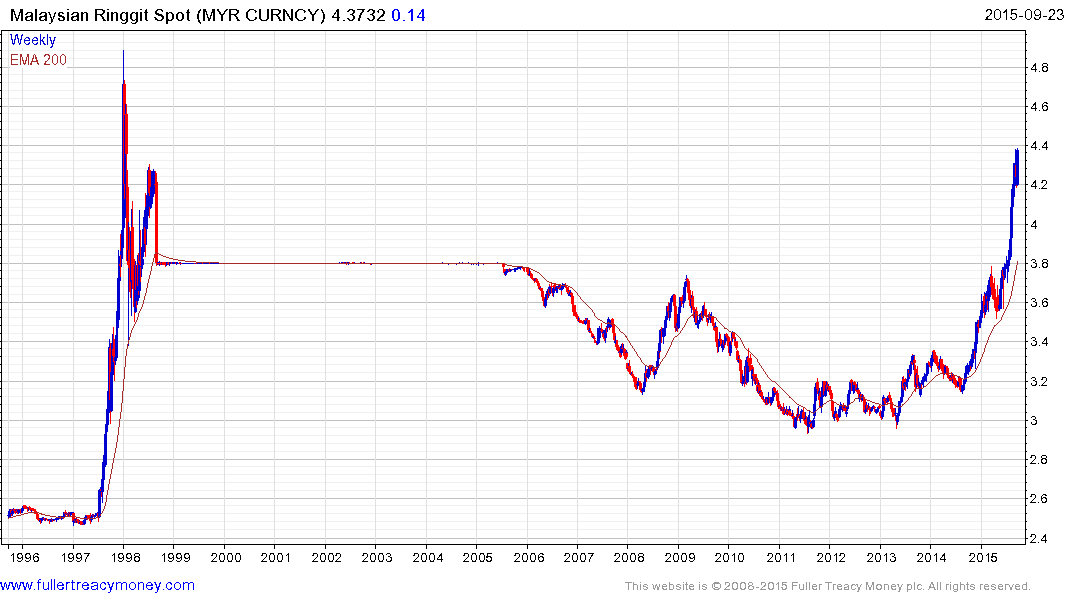

Brazil has borne the brunt of the selling pressure considering how exposed the market is to commodity prices. Nevertheless, the Turkish Lira, Malaysian Ringgit, Indonesian Rupiah and South African Rand have also deteriorated considerably and are already pricing in credit downgrades. As I pointed out yesterday Indonesian sovereign spreads are still relatively tight considering the deterioration already evident in the currency markets so there is ample room for spreads to widen.

.png)

This topical report from the Brookings Institute may be of interest. Here is a section:

As we have argued in the introduction, it is important to understand the role of global liquidity when we want to focus on foreign currency borrowing by EM corporates. As shown by Baskaya, di Giovanni, Kalemli-Özcan, Peydro, and Ulu (2015), there is a direct link between global liquidity and capital flows and domestic credit boom in Turkey. As Hardy (2015) shows, when global liquidity is abundant, it is feasible that corporates themselves can borrow directly and easily in the markets, bypassing the domestic banking system. When the conditions are tight, this situation might reverse, where banks become the sole source of foreign currency lending to corporates. In fact, as seen in Figure 18 taken from Hardy (2015), there is a positive correlation between VIX and the share of foreign currency loans in the domestic credit provided by banks on average, when we look at a group of emerging economies composed of Argentina, Brazil, Chile, Colombia, Costa Rica, Croatia, Czech Republic, Hungary, Indonesia, Israel, Latvia, Lithuania, Mexico, Poland, South Africa, Turkey, and Ukraine.

.png)

Generally speaking banks have been leading on the downside during this correction and the VIX remains elevated. With emerging market currencies weak, the ability of their respective corporations to refinance debt at attractive rates is likely to be impaired not least by downgrades at the sovereign level.

This remains a fraught environment where deleveraging is evident. It may take a catalyst in the form of a sovereign default, major devaluation or political change in a major country to check selling pressure beyond short-term steadying.