A must read: ballast water convention

Thanks to a subscriber for this report from Deutsche Bank which may be of interest. Here is a section:

The convention will reinforce multi-year shipping upcycle

The Ballast Water Management Convention, which is scheduled to come into force in September 2017, requires all ships sailing in international waters to install a Ballast Water Management System (BWMS). In light of the high cost and uncertainties associated with BWMS, we expect shipowners to scrap most of their vessels of above 15 years in the coming 2-3 years. We estimate global dry bulk fleets will shrink 1.5% in 2018 and 3.9% in 2019 while VLCC utilization will pick up starting 2018. Buy Pacific Basin and CSD.An introduction of this convention

Initiated by the IMO in 2004, the Ballast Water Management Convention was designed to prevent transfers of invasive aquatic species via ships’ ballast water. After the accession of Finland, the convention was ratified in Sept. 2016, and will enter into force in Sept. 2017. Thereafter, new vessels will have to install the BWMS on delivery date. For existing vessels, they are required to carry out retro-fit until their next International Oil Pollution Protection (IOPP) renewal survey (conduct every five years). While some vessels could get a grace period of up to five years (assuming the IOPP is renewed just before September this year), there are high levels of uncertainty over this exemption as the IMO is scheduled to further debate this exemption in July.Potential impacts on shipping market

The BWMS is expensive (USD2.5m for a VLCC and USD1.5m for a Capesize). This extra cost, along with higher maintenance expense, would substantially lift the breakeven level for 15+ years old vessels. Alongside the freight rate discount (to new ships) and rising demolition prices, our analysis shows that scrapping is the best option for shipowners. Currently, 14% of dry bulkers and 19% of VLCCs are above 15 years old and we expect this proportion of capacity to largely exit in the coming 2-3 years. Coupled with falling newbuild deliveries, we expect dry bulk supply growth to drop to 0.9% in 2017, and decline 1.5% in 2018 and 3.9% in 2019 (vs. 2.3% in 2016). Similarly, we expect VLCC utilization rates to pick up to 85.1% in 2018, in part due to the 2015-16 peak cycle.

Here is a link to the full report.

The Baltic Dry Index has been ranging in a volatile manner for eight years because a lot of the new ships ordered in the commodity bull market were delivered at just the time that global economic activity collapsed. The result has been a surplus of ships, where the lives of old vessels were prolonged because it was more economic to keep them in service than to scrap or sell them. The introduction of the Ballast Water Management Convention has the potential to represent a significant bullish catalyst for the sector.

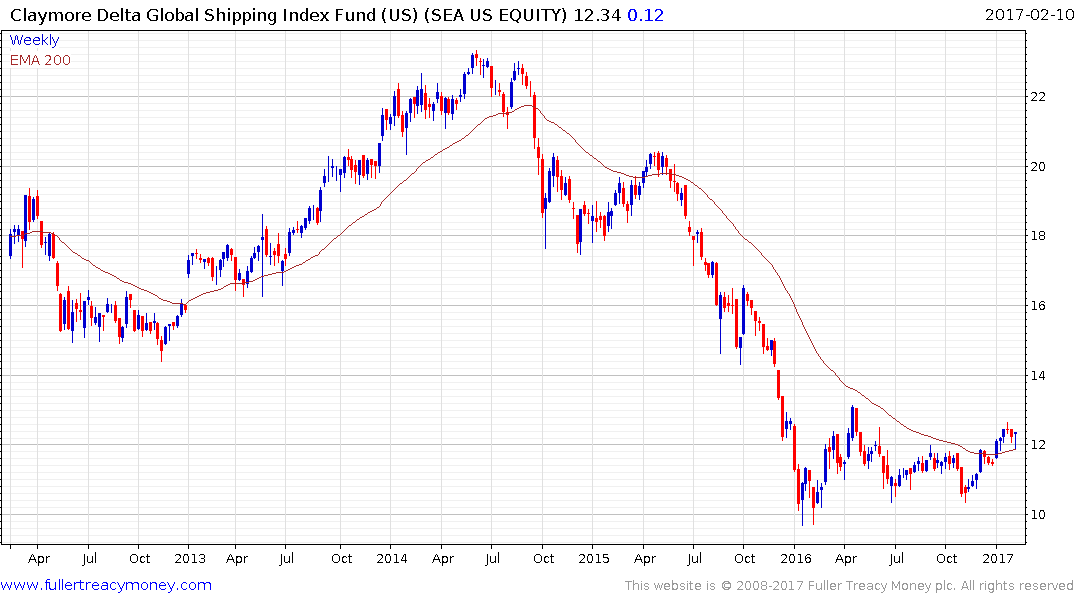

The US listed Claymore Delta Global Shipping Index Fund hit a medium-term low in January 2016 and has been confined to a ranging consolidation since. It found at least near-term support in the region of the trend mean over the last couple of weeks and a sustained move below it would be required to question medium-term recovery potential.

Here is a list of the ETFs constituents sorted by price to book; highlighting just how low ship prices are right now. With global economic growth picking up and the potential supply of ships contracting this could represent the bottom of the cycle for what is a highly cyclical sector.

Back to top