2017 Roundtable, Part 2: Manual for a Mixed-Up Market

Thanks to a subscriber for Part 2 of this transcript from Barron’s which may be of interest. Here is a section on German Bunds:

Next, like Felix, I would short German Bunds. They are yielding 0.27%, and Germany’s inflation rate is 1.7%. Historically, it is very rare to have a Bund yield below the inflation rate. The current gap is a record. The Bund yield is unsustainably low.

Schafer: What is the best way for an individual to short German Bunds?

Gundlach: Short the futures. I agree with Felix that the Italian bond market is deeply troubled. Shorting Italian bonds could potentially produce a massive home run; they are yielding 47 basis points less than 10-year U.S. Treasuries, which represents a full buy-in on the idea that the euro zone will last forever. If the euro zone breaks up, a possibility we have discussed, and Italy has to go it alone, sovereign bonds could yield 1.9%. The current yield is insanely low. But shorting German Bunds appeals more. They are more vulnerable at this point than U.S. bonds.

One argument for U.S. bonds when yields hit a low last July was that they yielded more than German Bunds, which had negative yields. In other words, U.S. bonds were better than something really terrible, but that didn’t make them good. Underlying the argument was the notion that German yields would stay negative forever. Well, forever lasted about a month. Since then, Treasury yields have risen more than German rates, but Bunds could underperform in the next leg of the bond bear market.

Zulauf: In 2012, there were widespread fears about the euro zone breaking apart. Back then, money flowed from the southern countries to the northern countries, and into Bunds. The next time the euro zone looks endangered, money will flow out of the euro completely and into another currency, primarily the U.S. dollar.

Here is a link to the full report.

Germany has benefitted enormously from the ECB’s quantitative easing program. As the largest economy in the bloc it garners the most purchases which are weighted by GDP. As the region’s largest creditor it holds sway over the direction policy takes. The creation of the Euro alleviated currency risk for Germany and country’s approximating its economic model such as the Netherlands and Austria. However for countries that did not have economies similar to Germany’s it crystallised currency risk.

I have heard more than a few commentators share the view that the primary reason to own German bonds is as a cheap hedge against the dissolution of the Euro. The logic runs that if the Euro disappears the “Neuer” Deutsche Mark would soar in value as Germany’s individual economic strength would be priced in. The countervailing argument is that Germany might not be able to collect on the massive debts it is owed by its neighbours if the currency those debts were denominated in no longer exists.

Bund yields have paused near 0.4% and some steadying following another doubling since January looks likely. However a sustained move below 0.15% would be required to question medium-term potential for additional expansion.

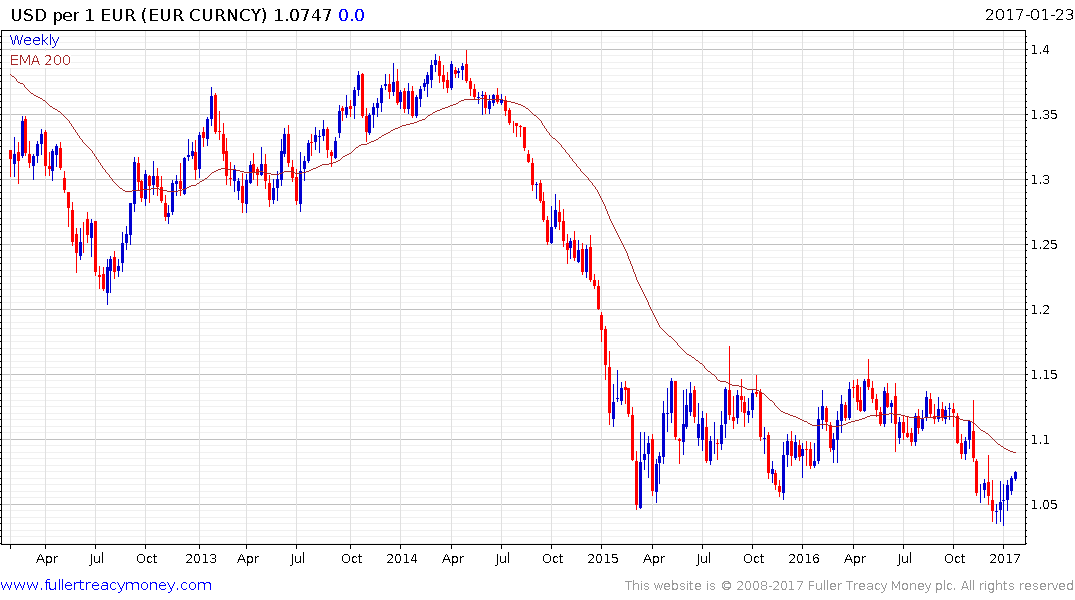

The Euro failed to sustain the break below $1.05 and has unwound most of its overextension relative to the trend mean. This is the largest rally since November and a sustained move above $1.09 would break the almost 9-month progression of lower rally highs.

Concurrently, many investors will be keeping a close eye on the Dollar Index which is retesting the psychological 100 level. In early December it posted an emphatic upside key day reversal from this area and a similar upward dynamic will now be required to confirm a return to demand dominance.

Back to top