"Serenity Now"

Thanks to a subscriber for this report by Jeffrey D.Saut for Raymond James which may be of interest. Here is a section:

To be sure, all of this fits with our thesis the equity markets are transitioning from an interest rate-driven to an earnings driven secular bull market. To that point, many of y’all know we are on an email “string” with folks like Arthur Cashin, David Kotok, Dennis Gartman, Bob Pisani, etc. It is a freewheeling exchange of thoughts that provides very interesting insights. Last Thursday, the savvy Bob Pisani wrote this:

President-elect Trump's proposed nominee for U.S. Treasury Secretary, Steven Mnuchin, said on our air yesterday that the administration was still targeting a reduction in the corporate tax rate from 35% to 15%. The current 2017 estimate for the entire S&P 500 is roughly $131 per share. Thompson estimates that every 1 percentage point reduction in the corporate tax rate could "hypothetically" add $1.31 to 2017 earnings. So do the math: if there is a full 20 percentage point reduction in the tax rate (from 35% to 15%), that's $1.31 x 20 = $26.20. That implies an increase in earnings of close to 20%, or $157. What does that mean for stock prices? The S&P is currently trading at a multiple (PE ratio) of 17, high by historical standards. Applying that 17 multiple to earnings of $157, we get a price on the S&P 500 of roughly 2,669 for 2017. That is 469 points or roughly 20% above where it is today.

Our sense is the new administration will not be able to get the corporate tax rate down to 15%, but even at a 25% rate, it implies an additional $13.10 to the S&P 500’s bottom up operating earnings number ($1.31 x 10 = $13.10). Using Bob’s same math produces an earnings estimate of $144.10, and at 17 times earnings, it renders a price objective of roughly 2450 for the S&P 500.

Here is a link to the full report.

A successful transition from an almost total reliance on easy monetary policy to an expansion predicated on improving profitability can be considering the best possible scenario. With corporate margins at record highs cuts to corporate taxes could well be what is required to lend an additional boost to justify higher equity prices.

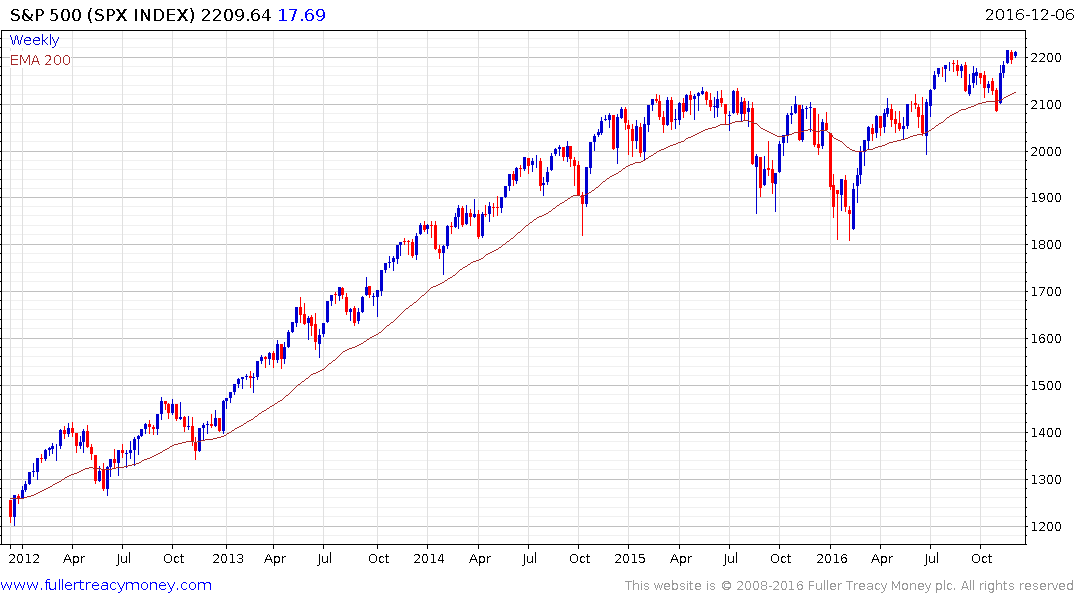

The S&P500 broke out of a long-term range in 2013 and spent more than a year ranging in what was a volatile consolidation with two major downward spikes that challenged investor confidence. However the Index broke out to new highs in July and found support in the region of the trend mean and the upper side of the underlying range in November. A sustained move below 2050 is the minimum required to question medium-term scope for continued upside.

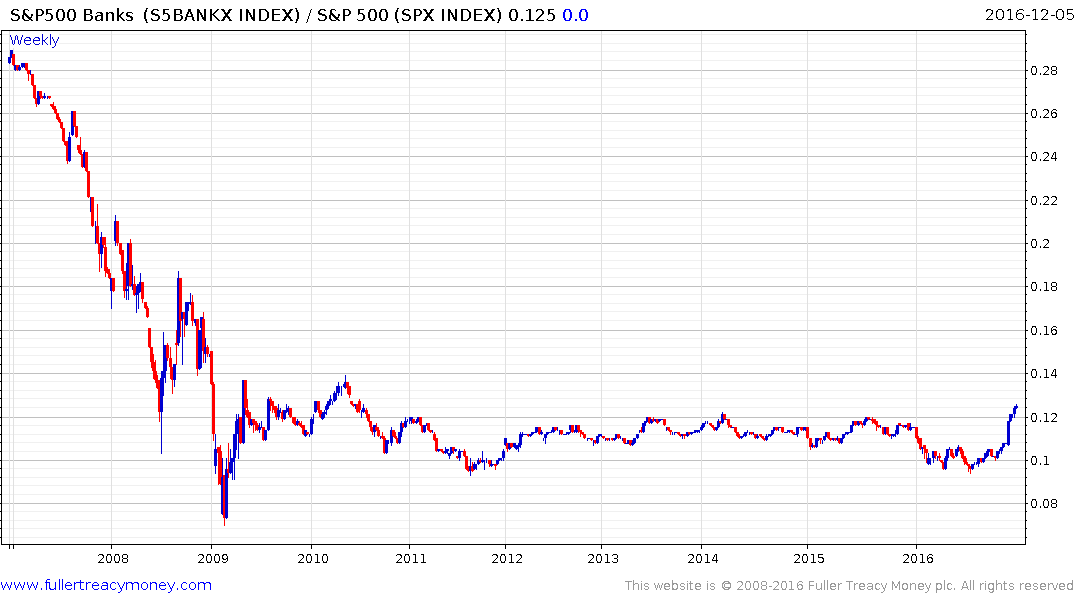

The S&P500 Banks Index is in the process of completing a relative base and a sustained move below 0.12 would be required to question potential for continued outperformance. With banks likely to benefit from looser regulation, higher interest rates and lower taxes, the potential for lending to pick up might now be considered the base case.

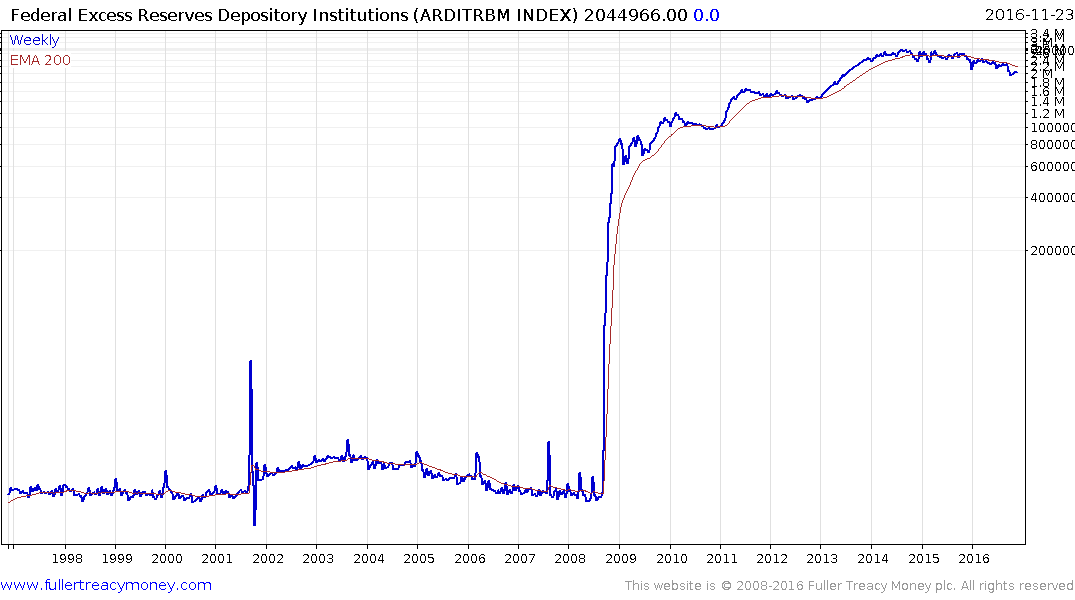

Federal Excess Reserves for Depository Institutions peaked in 2014 and continues to trend lower. Considering the run-up to $2.5 trillion was in large part driven by banks rebuilding their balance sheets amid tighter regulations and a weak economy, the downtrend may suggest banks are starting to lend again. That’s an important support for any bull market.