The multi-asset essay: Why commodities will recover

Thanks to a subscriber for this report from Deutsche Bank which may be of interest to subscribers. Here is a section:

Our call for a final leg down in metals prices is based on weaker-than-expected oil prices and the potential depreciation of the Chinese renminbi. Metals currently are factoring in oil at $40 a barrel – not today’s prices of low $30s. Furthermore, a weaker Chinese currency is likely to drag down commodity currencies even further. But that is likely to be the end of this deflationary cycle.

Management teams may be able to take out more costs, but we are at the point where these cuts would be unsustainable, ultimately leading to lower output in the future.Why is that? Because current spot prices are 40 to 50 per cent below so-called incentive prices, which are the prices required to earn a 12-15 per cent rate of return on a project. As a result, capital spending on new capacity has simply dried up, with industry capex down over 60 per cent versus the peak in 2012. Ore bodies are depleting assets and current capex levels are not sufficient to sustain current output for more than two to three years. In copper, for example, the world needs two new large-scale mines every year just to offset the reserve depletion.

While oil prices are low, current spot prices for metals are well below the marginal cost of most producers. As an extreme example, nearly two-thirds of the nickel industry is under water. That has placed mining company balance sheets under intense pressure. We estimate the net debt of the largest companies will approach an uncomfortable 3.5 times ebitda by the end of the year. This could force an industry tipping point and, indeed, supply curtailments have already started to gather momentum. In aggregate, around five per cent of the industry’s capacity is in the process of closing. We need at least ten per cent of the capacity to be shuttered to reach critical mass. Given the stresses in the industry, we think this will occur during 2016 and will stabilise prices. It may take a little longer for capital constraints to become apparent, but as they do, metal price deflation will quickly turn to inflation.

Here is a link to the full report.

I was talking to a Scotland based nickel buyer in Heathrow a couple of weeks ago who testified to how difficult the business of buying scrap has been over the last few years. Prices have been falling in a jerky fashion, which complicated their hedging strategy making it largely ineffectual. They are now surviving on thin margins and really hope for a turn in the price environment soon to ensure survival.

The problem for many basic resources operations is that the cost of delivering marginal supply falls in line with energy prices. Labour and energy represent two important costs for mines so higher energy prices would represent an increase in costs highly leveraged marginal producers would be unlikely to shoulder. This would represent a withdrawal of supply from the market and may allow prices to stabilise.

The LME Metals Index remains in a medium-term downtrend and will need to break the progression of lower rally highs to signal a return to demand dominance beyond short-term steadying.

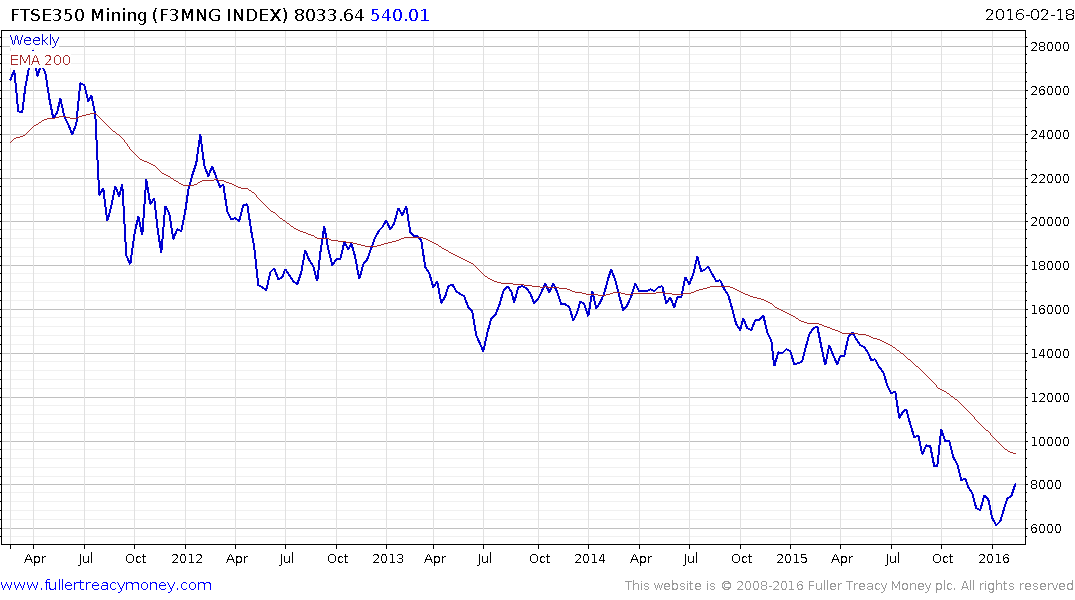

Mining shares may be leading on the upside. The FTSE 350 Mining Index rallied this week to break the steep downtrend evident since April and a process of mean reversion is now underway. It will need to find support above the January low on the first major pullback to demonstrate demand coming back in at a progressively higher level and to signal more than a temporary floor.

The first questions are now being asked about the sustainability of the rebound in miners with shares like Tech Resources now testing the region of its trend mean. A sustained move above this week’s high will be required to confirm a return to medium-term demand dominance.