The Big $hort

Thanks to a subscriber for this report from Zoltan Pozsar for Credit Suisse. Here is a section from the conclusion:

Paraphrasing Herodotus…

…”circumstances rule central banks; central banks do not rule circumstances”.

Inflation is a complex phenomenon, and it has nothing to do with DSGE models. Free-flowing commodities and commodity traders guarantee price stability, not central banks, and deflationary impulses coming from globalization shouldn’t be mistaken for central banks’ communication skills as anchors of price stability.

Luck is luck. Luck isn’t structural…

Luck is running out; central banks were lucky to have price stability as a tailwind when they had to fight crises of FX pegs, par, repo, and the cash-futures basis. Those were the easy crises. The ones you can print your way out of with QE.

But not this time around…

Inflation borne of shortages (commodities [due to Russian sanctions], goods [due to zero-Covid policies], and labor [due to excessive positive wealth effects]) is a whole different ballgame. You can’t QT or hike your way out of it easily…

…and if you can’t, credibility gets damaged, a decline of the U.S. dollar is inevitable, and shorting U.S. rates, the U.S. dollar, and some FX pegs make logical sense.

Here is a link to the full report.

There are a lot of moving parts in the markets today. Everyone is eager to come up with a narrative that cuts through the verbiage and illuminates a path to security and stability of mind and purpose. It’s not easy because there are so many conflicting ambitions. Most people can’t shake the feeling momentous events result in momentous, not necessarily fortuitous, outcomes.

Let’s think about what drives markets: Money supply and crowd psychology.

Right now, the Federal Reserve is talking the talk about tightening monetary policy and the US government is running a deficit similar 2019’s. That sounds almost reasonable when compared to the pandemic splurge but is still a whole lot of money.

Expectations for interest rate hikes have significantly diverged from reality and the short-term oversold condition in the 2-year is slowly easing. So far the pullback is similar to the February pause so a further decline will be required to confirm a peak of more than short-term significance for the price.

The ECB is determined to lag the USA in both raising rates and removing accommodation. Japan intends to be last. That’s been weighing on both their currencies, but they also oversold. If Treasuries begin to rally, the Dollar will decline.

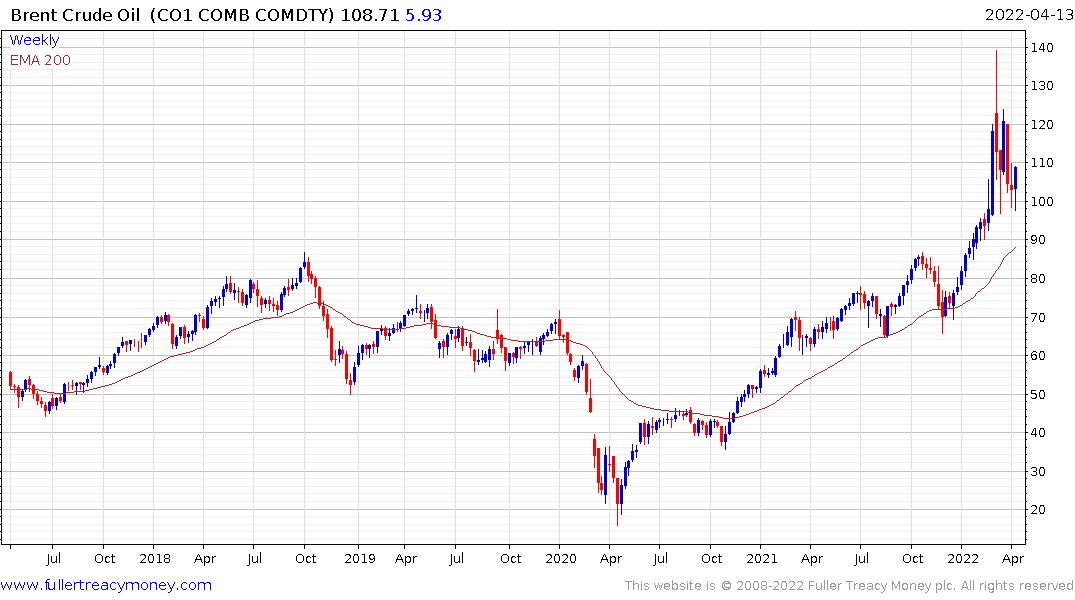

That would be a major bullish catalyst for gold and potentially also oil prices.

Silver is likely to outperform gold in the next stage of its bull market.

The total assets of central banks chart contracted by $500 billion due to Dollar strength. Quantitative tightening would have an additional negative impact on global liquidity and would inevitably contribute to volatility for as long as it lasts.

The total assets of central banks chart contracted by $500 billion due to Dollar strength. Quantitative tightening would have an additional negative impact on global liquidity and would inevitably contribute to volatility for as long as it lasts.

China’s credit impulse has not conclusively bottomed. They have internal issues with attempting to avoid further inflating the property bubble that is hindering their ability to stimulate even as the economy struggles with the pandemic. They also have a vested interest in ensuring the currency is stable to create a viable haven from distress in the global market.

The Russian Ruble is not being updated on Bloomberg, but it is back at pre-invasion levels. With talk of war crimes and tens of thousands of dead civilians it is extremely unlikely Russia will have open trading lines with the OECD any time soon. That has created an alternative currency system which challenges the petrodollar system.

That idea is gaining traction internationally. For example, this video kindly forwarded by a subscriber offers an (Indian?) perspective. Sri Lanka is defaulting, Egypt is experiencing chronic food shortages and more countries will inevitably fall victim to commodity inflation stress.

India has its own inflation issues and China relies on commodity price stability more than any other major economy. They have no choice but to pick up commodities from Russia at a discount to prevailing prices. International sanctions take a backseat to necessity. It’s no longer a choice, emerging markets will need to deal with Russia and that means using an alternative transfer mechanism.

Pozsar talks about four types of money. These are par, interest, foreign exchange and price levels. All are useful ways of thinking about money and the current inflation is worrisome for the ability of central banks to keep orderly markets. However, there is a fifth. Military might. Transitions between hegemonic regimes do not happen peacefully. To instill a new world order, you have to win the war. The losers then end up covering your debts.

Current talk of hypersonic weapons, capability to shoot down satellites, and to also launch new ones at pace, all point to a new arms race. This report from Bridgewater discussing the ramifications of sanctions on Russia may also be of interest.

Stock market trends are no longer consistent. Recovery is very dependent on liquidity remaining both cheap and available.

The Nasdaq-100 paused today but is still distributing below its 200-day MA.

The Nasdaq-100 paused today but is still distributing below its 200-day MA.

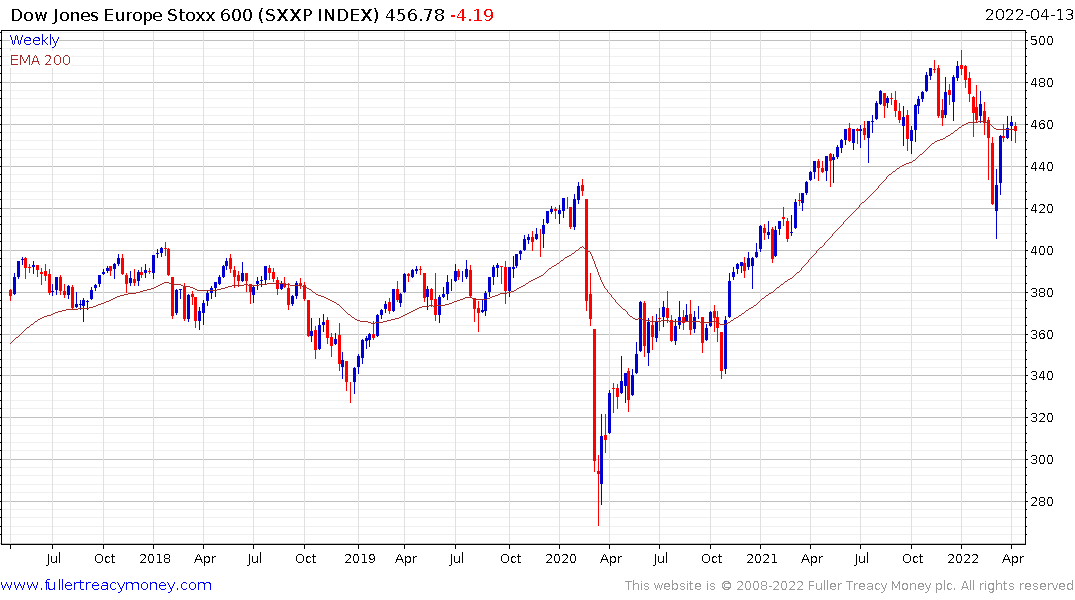

Most European stock markets experienced Type-2 massive reactions against their prevailing trends. The Europe STOXX 600 is currently steady below the trend mean and has unwound its oversold condition. It will need to sustain a move above 470 to confirm a return to demand dominance beyond steadying.

Most European stock markets experienced Type-2 massive reactions against their prevailing trends. The Europe STOXX 600 is currently steady below the trend mean and has unwound its oversold condition. It will need to sustain a move above 470 to confirm a return to demand dominance beyond steadying.

Defensive sectors like healthcare and consumer staples continue to outperform.

Commodities generally also outperform strongly in the latter stages of a bull market.

The clear conclusion is if central banks persist in combatting inflation asset prices will suffer. If their determination wavers for any reason, asset prices will quickly reinflate. Bitcoin’s successful rebound from the psychological $40,000 today supports the view investors are willing to bet interest hiking enthusiasm has gone too far.

Back to top