Tesla Stock Is the Cheapest Ever After This Year's 52% Slump

This article from Bloomberg may be of interest to subscribers. Here is a section:

“My biggest concern is the slowdown they’re seeing in China,” Matt Maley, chief market strategist at Miller Tabak + Co. said, adding that “as long as Elon Musk is spending a lot of time with Twitter, it’s going to keep a lid on the stock.”

Bloomberg News reported Friday that Tesla plans to suspend output in stages at its Shanghai electric car factory from the end of the month until as long as early January, amid production line upgrades and slowing consumer demand.

Meanwhile, Twitter is more than a distraction. Musk’s bankers are considering replacing some of the high-interest debt he layered on Twitter with new margin loans backed by Tesla, people with knowledge of the matter told Bloomberg.

I saw in another article that SpaceX is valued at approximately $140 billion. The purchase of Twitter has stretched both Elon Musk’s time and finances. If his creditors impose a margin loan there is clear scope he will be denuded of his Tesla holdings if Twitter does not turn around quickly. That may result in a rush to IPO SpaceX to raise cash.

Additionally, Musk has a clear conflict of interest in depending on China for sales of Tesla vehicles while owning one of the West’s biggest media dispersion venues. That suggests his free ride in terms of media attention/adoration is coming to an end. Being boosed for several minutes at a gig with Dave Chappelle over the weekend is not great news for his popularity

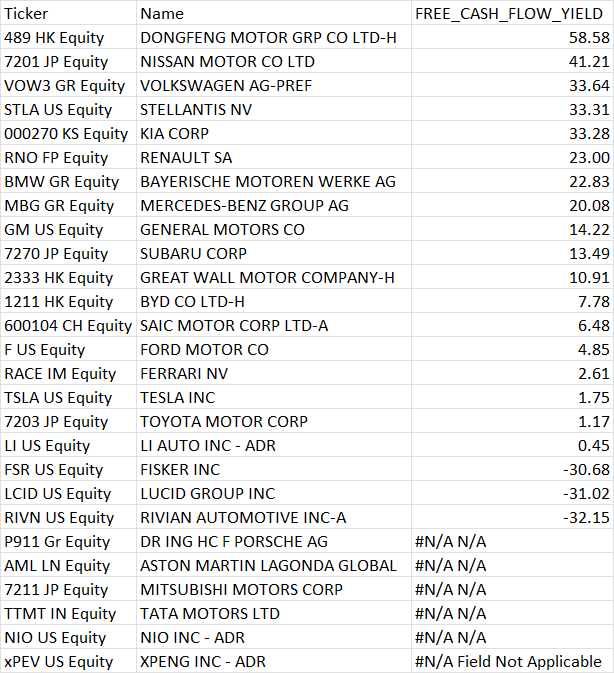

Tesla has traded at a growth multiple and not least because of Musk’s magnetic personality. At its peak that enthusiasm assumed it would be the only automaker to survive the “energy transition”. As it stands, there is simply not enough copper, nickel and lithium mined annually to fulfill the utopian ideal of ending reliance on internal combustion engines.

The company’s free cash flow yield is at the lower end of a global comparison chart and China is increasingly building better batteries. The share remains in a downtrend.