Secular Themes Review July 2nd 2021

On November 24th I began a series of reviews of longer-term themes which will be updated on the first Friday of every month going forward. The last was on May 7th. These reviews can be found via the search bar using the term “secular themes review”.

News today that Johnson & Johnson’s vaccine is effective against the delta variant should help to allay fears that the world is about to experience a round of upheaval similar to early 2020.

There is no question that the pandemic has acted as an accelerant. It forced migration and adaption to new conditions in a manner that might otherwise never have happened. Some of those changes will stick, others will fade away.

Everyone seems to think that the pandemic has to mean something and that we will never again get back to normal life. I don’t believe it. The surges back into social activity whenever restrictions are lifted is confirmation that humans are social beings. We crave physical contact and fellow feeling. That’s not going to change, even if we have a better appreciation for it today than since the demise of organised religion.

As with every other crisis, the liquidity created to deal with the shock will remain in the system for much longer than it is strictly required. Central banks cannot afford to jeopardise the recovery they worked so hard to create. Meanwhile, populations everywhere are impatient for better conditions.

It’s that impatience which is likely to translate into government policy and additional deficit spending. My measure of global deficits is still running at around $1.8 trillion. Without clear evidence of ill effects, is there any politician who is going to be successfully elected on a balanced budget program?

It’s that impatience which is likely to translate into government policy and additional deficit spending. My measure of global deficits is still running at around $1.8 trillion. Without clear evidence of ill effects, is there any politician who is going to be successfully elected on a balanced budget program?

Meanwhile the risk is that everyone has learned that bailing out consumers directly is much more comfortable than bailing out banks and businesses. Calls to boost social spending and to increase the scope of support programs will be hot election issues in years to come. Ultimately, all politics is local and focuses on giving the people what they want. The pandemic has changed the way bailouts are practiced. That suggests in future crises we can anticipate a much greater focus on people than businesses.

The biggest point is that the crisis of 2020 is unlikely to be repeated any time soon. The world is a lot more vigilant today than it was before the pandemic. All manner of mitigation strategies have been tested and it stands to reason that the responses to a future health scare will be more systematised. That’s also why virus news has been incapable of impacting financial markets.

Instead, we are back on the liquidity gravy train. US money supply is growing at 16% month over month. That’s nowhere near the peak values from last year but the rate of growth is still outstripping the pace ahead of the pandemic. At the same time short-term interest rates are still close to zero.

The result is that financial conditions remain as loose as they have ever been.

.png) The yield curve spread (10-year - 3-month) has hit at least a near-term peak. Growth is recovering and investors are betting that inflationary pressures are indeed transitory. That’s resulting in bond yields compressing which is creating demand for higher growth assets.

The yield curve spread (10-year - 3-month) has hit at least a near-term peak. Growth is recovering and investors are betting that inflationary pressures are indeed transitory. That’s resulting in bond yields compressing which is creating demand for higher growth assets.

.png)

The relative strength of Wall Street supports the view that the US economy is going to bounce back harder and faster than elsewhere. That’s both a function of how deep the decline was and the sheet volume of money printed over the last 15 months.

There have certainly been excessed recorded over the last year and the en masse introduction of retail traders in the market was a big influence of prices in 2020. The VanEck Vectors Social Sentiment ETF was just launched and focuses on companies gaining the most interest on social media. It’s existence is a reflection of how much demand there is for a production to track the enthusiasm of retail traders.

Supplying consumers with additional cash and plenty of time for trading supported the meme stock bull market. It was also a significant influence on the surge in demand for cryptocurrencies in 2020. Cash flowed into the market from all over the world and the sector reached a market cap of $2 trillion.

In 2017, cryptocurrency sector was too small to be of interest to institutions. The price accelerated between Thanksgiving and Christmas because college kids went home and told their parents to buy. The 2020 acceleration was on the back of institutions offering custody services to large clients chasing similar returns. The $10 trillion in additional pandemic money printing spurred significant interest in the sector. It peaked in May and is likely to be a much quieter venue for speculation until about a year before the next halvening. That suggests the time to get interest in crypto again will be in 2023.

.png) The Dollar remains the lynchpin for flows between the USA and the rest of the world. Despite higher growth and the prospect of the Federal Reserve moving to taper assistance at some point over the coming 18 months, the big question is whether that is enough to support the Dollar.

The Dollar remains the lynchpin for flows between the USA and the rest of the world. Despite higher growth and the prospect of the Federal Reserve moving to taper assistance at some point over the coming 18 months, the big question is whether that is enough to support the Dollar.

The ECB might like the respective Eurozone governments to boost fiscal stimulus but how that will be agreed upon remains an open question. To sidestep that challenge the introduction of pan European bonds was a major development in 2020 and suggests the total quantity of Eurozone debt is now open ended. Considering the fact the yields across a broad swathe of Europe are negative it makes sense to massively increase borrowing. The potential for the Green Party to gain electoral success in Germany would help that cause along considerably.

That’s the primary challenge in predicting a big Dollar decline. In order for the Dollar to decline in a big way, another currency region would need to strengthen in a big way.

In the early 2000s the Euro had just been introduced and declined significantly for the first couple of years. Multi-lateral intervention to support the currency led to years of outperformance relative to the Dollar at exactly the same time that the USA needed a weaker currency.

As David used to say “Happiness in the currency markets is having the trend and the central bank on your side” and “the best trades in currencies come with matching the strongest against the weakest”.

The Dollar is competing for the weakest currency crown with Europe and Japan.

The Australian Dollar, Canadian Dollar, Brazilian Real, South African Rand, Russian Ruble all strengthened in line with commodities over the last year.

The Australian Dollar, Canadian Dollar, Brazilian Real, South African Rand, Russian Ruble all strengthened in line with commodities over the last year.

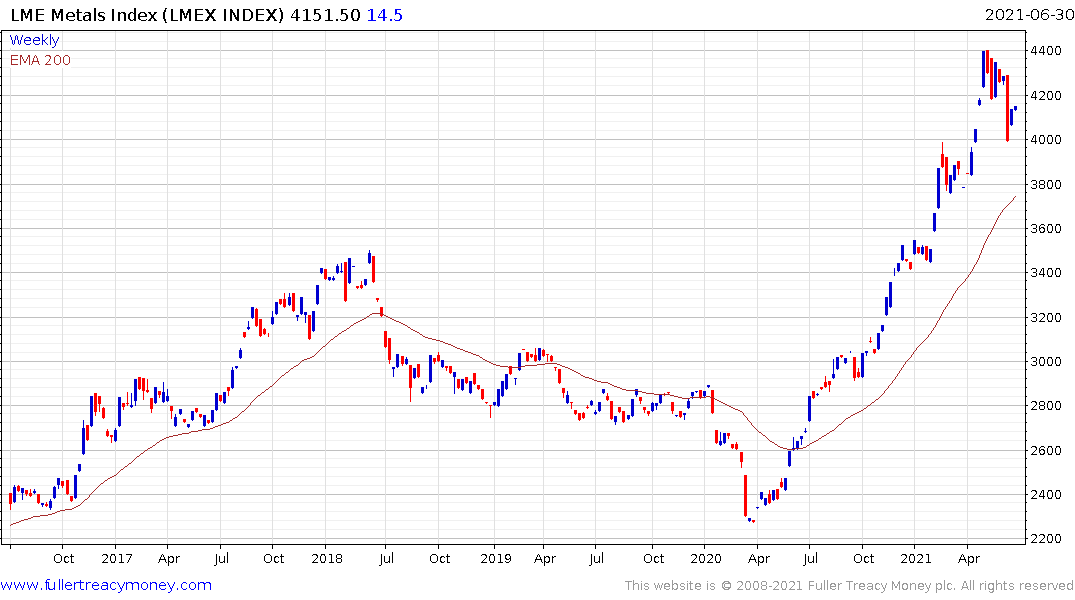

The LME Metals Index and CRB Raw Industrial Resources Spot Index both remain in clear uptrends.

The LME Metals Index and CRB Raw Industrial Resources Spot Index both remain in clear uptrends.

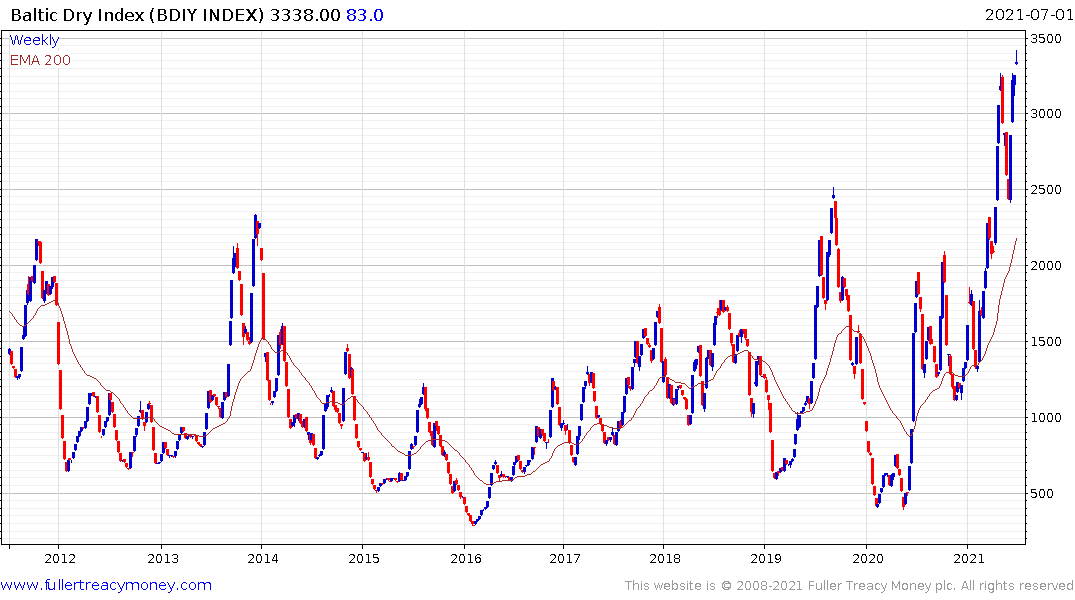

The Baltic Dry Index also continues to extend its breakout from a long-term base formation.

The challenge is that China has committed to selling down about 1% of its strategic stockpile for copper. That is weighing on sentiment in the short term. However, that stockpile was accumulated to provide for geopolitical tensions cutting off the ability to import, not to control prices. This is unlikely to be anything other than a short-term obstacle to price increases.

That represents a tailwind for commodity related currencies.

The Bank of England is expressing disquiet at rising inflationary pressures but does not appear willing to do anything about it other than talk. The Pound is testing the upper side of its base formation against the Dollar, Yen and Euro.

The other factor is the UK government has a vested interest in demonstrating that the decision to exit the EU was a good one. Supporting growth and currency stability are priorities as a result.

The Chinese Renminbi is the lodestone for Asia generally. Most countries in Asia do more trade with China than anywhere else so they are acutely sensitive to movements in the Renminbi. The currency has unwound the majority of the 2018/19 devaluation so the current area is a point of indecision for policy makers.

On the one hand they have the challenge of sanitising the massive inward flows of 2020 and keeping a lid on inflationary pressures. On the other hand, they have to ensure the economic recovery is not impeded by the currency impacting the competitiveness of the economy.

In normal circumstances pairing those competing factors off against one another would be the normal practice of economic management. However, the Chinese administration have committed themselves to bringing the Taiwan question to a conclusion within the rein of Xi Jinping.

Achieving the goal of reunification was the logic used to support Xi’s bid for premiership for life and he will be under pressure to deliver something the longer he remains in power. The increasingly strident language used in official pronouncements is unlikely to be idle chatter aimed at stirring nationalist fervour. The currency is a geopolitical tool to further China’s goals and that is the primary rationale that dictates the value it is allowed to trade at.

On aggregate, there commodity producers and Pound look most likely to trend higher against the Dollar over the medium term.

A preference for weak currencies and low interest rates continues to support growth an innovation.

I posted this video presentation from Tesla’s head of automation earlier this week. One of the most significant developments is they have developed an autonomous labelling system for visual data.

Historically, that has been an extremely labour-intensive job requiring people to individually label every item in an image so an artificial intelligence system can be taught to recognise them. By automating the process Tesla greatly reduces the price and increases the speed of innovation.

The fact they have developed one of the world’s fastest super computers to do that is a testament to just how resource hungry the high-tech innovation sector is. We are way beyond the point where a small team writing code can change the world. Solving machine learning and artificial intelligence problems requires massive investments in capital infrastructure.

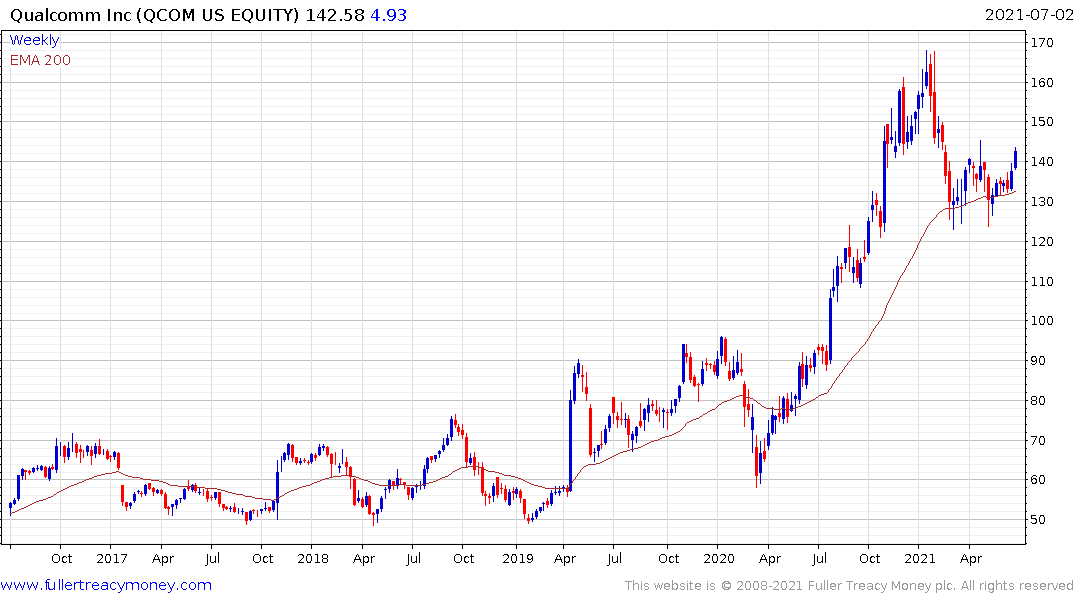

That’s the primary rationale behind the continued outperformance of Nvidia, Qualcomm and Applied Materials. Nothing has happened to change the fact that this portion of the tech sector is cyclical. Once the building boom is over, the shares are likely to come back down. That suggests paying attention to the consistency of their respective trends is more important than ever following such large moves.

That’s the primary rationale behind the continued outperformance of Nvidia, Qualcomm and Applied Materials. Nothing has happened to change the fact that this portion of the tech sector is cyclical. Once the building boom is over, the shares are likely to come back down. That suggests paying attention to the consistency of their respective trends is more important than ever following such large moves.

Google is investing heavily in developing quantum computing. Honeywell, IBM and China are doing the same thing. The pace of innovation in this sector is astounding and is an aid in further accelerating the pace of technological innovation for the wider economy too.

The application of machine learning and artificial intelligence to massive data sets created by the healthcare sector is an additional source of innovation that is significantly faster than Moore’s Law.

These innovations promise to enhance productivity and create a lower industrial footprint over time. It runs squarely into the populists calls to boost the role of labour in the economy. The challenge for the union movement is they have historically blocked the introduction of labour saving devices with the short-term aim of preserving jobs. Medium-term that only increases the scope for the factory to close to move to more accommodative locations.

Germany, Japan and South Korea preserved domestic manufacturing by championing the adoption of technology and automation. The only way to come close to competing with either low costs of emerging markets or high efficiency of developed markets is to adopt the same or better technology. Quite how that sits with progressivist labour unions will be a big determinant of how successful reshoring efforts will be.

As we look to the outlook for the markets over coming years. The outlook for yields and the Dollar are pivotal. We are in a very liquidity rich environment and that supports the argument for asset price inflation.

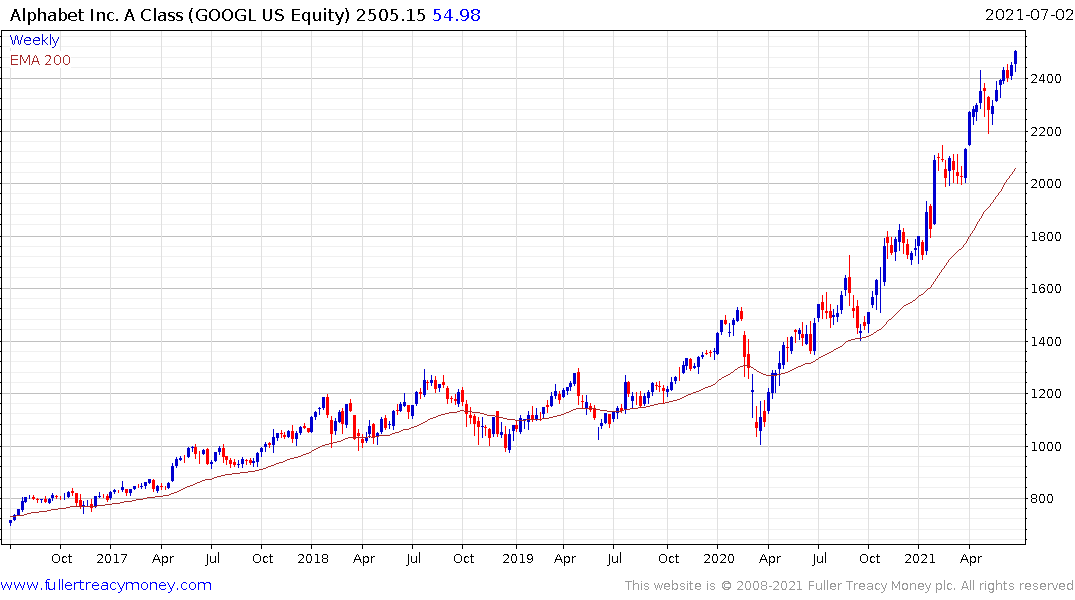

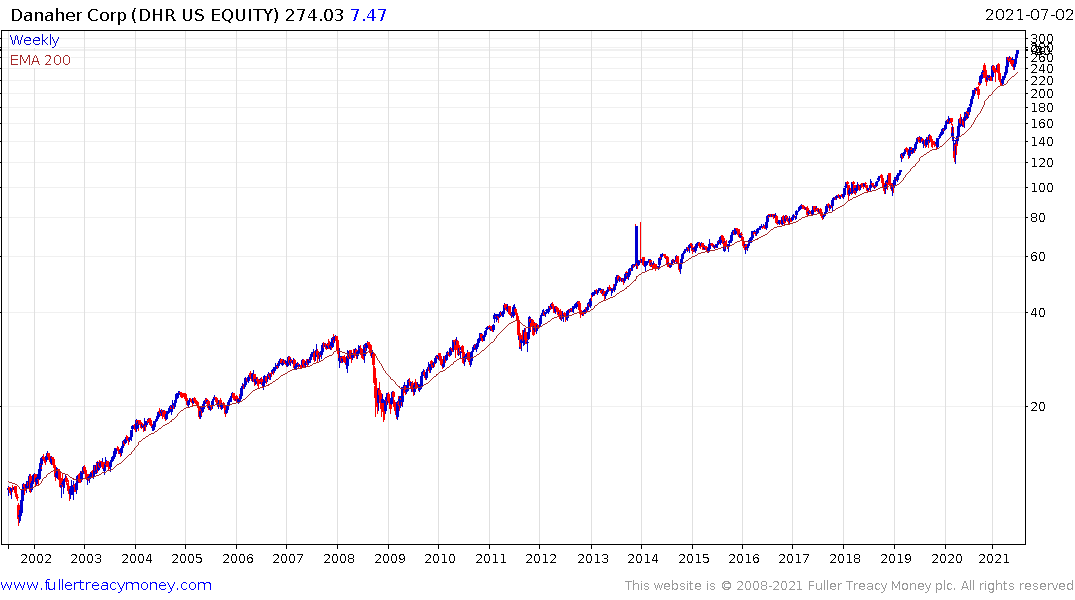

Private equity has been among the best performing asset classes over the last forty years because the downtrend in yields made the returns in private markets progressively more attractive. Companies with private equity-like business models, where they invest heavily in developing or buying niche technologies remain among the best performers. Danaher, Roper Technologies, Thermo Fisher, Samsung Electronics, Taiwan Semiconductor, Alphabet, Amazon, Apple, Facebook or Brookfield Asset Management fall into that category.

Private equity has been among the best performing asset classes over the last forty years because the downtrend in yields made the returns in private markets progressively more attractive. Companies with private equity-like business models, where they invest heavily in developing or buying niche technologies remain among the best performers. Danaher, Roper Technologies, Thermo Fisher, Samsung Electronics, Taiwan Semiconductor, Alphabet, Amazon, Apple, Facebook or Brookfield Asset Management fall into that category.

The strength of the sector is unlikely be challenged by market forces but if interest rates turn it will alter the viability of the investment model.

The resolve of governments all over the world to build back better remains a tailwind for commodity demand growth. The Blackrock World Mining Trust bounced emphatically from the region of the trend mean over the last two weeks and remains on a clear recovery trajectory.

The big question for many investors is whether you can have a commodities bull market without oil prices also making new highs. The last two big commodity bull markets were led higher by oil prices so it is a big question. There is nothing to suggest that we are on the cusp of a supply shortage for crude oil. The impressive rebound from the 2020 lows has been impressive but is predicated on OPEC+’s supply discipline.

Secular bull markets in commodities are defined by the rising cost of marginal production. Prices breakout when demand increases and supply takes time to respond. That suggests a new oil bull market will not take place until the supply excess has been chipped away and a new source of demand emerges.

I believe the next big new source of demand will come from the construction and manufacturing sectors rather than transportation. The world is already devoting massive resources to battery manufacturing and development. The refusal to retool to favour platinum over palladium in catalytic converters is a reflection of the lack of investment in internal combustion engines.

The materials sector is bringing down the cost of producing carbon fibre, plastics and innovating to produce long lasting, light weight, strong polymers that are on the cusp of competing with lumber, cement and steel. TREX has been highly successful in selling long-life decking materials. However, I also saw cellulose shotgun cartridges and 9mm polymer rounds over the last few weeks. They are price competitive with what is currently available. This are niche sectors today but provide the proof of concept for more challenging uses.

That would provide a new use case for oil but in the transportation sector it will continue to be targeted for outsized taxation whether through carbon or value added taxes.

Gold remains an attractive asset in an environment where asset price inflation and valuation expansion is predicated on a race to the bottom in the currency market.

Gold remains an attractive asset in an environment where asset price inflation and valuation expansion is predicated on a race to the bottom in the currency market.

The price has been in a corrective phase for the last 10 months but may now be in the process of putting in a higher reaction low. That’s the first step to confirming a recovery is underway. I am particularly encouraged by the fact that sentiment is turning very negative. Only today I saw a prediction that gold will trend lower until 2024. That suggests to me that the hot money has left the market.

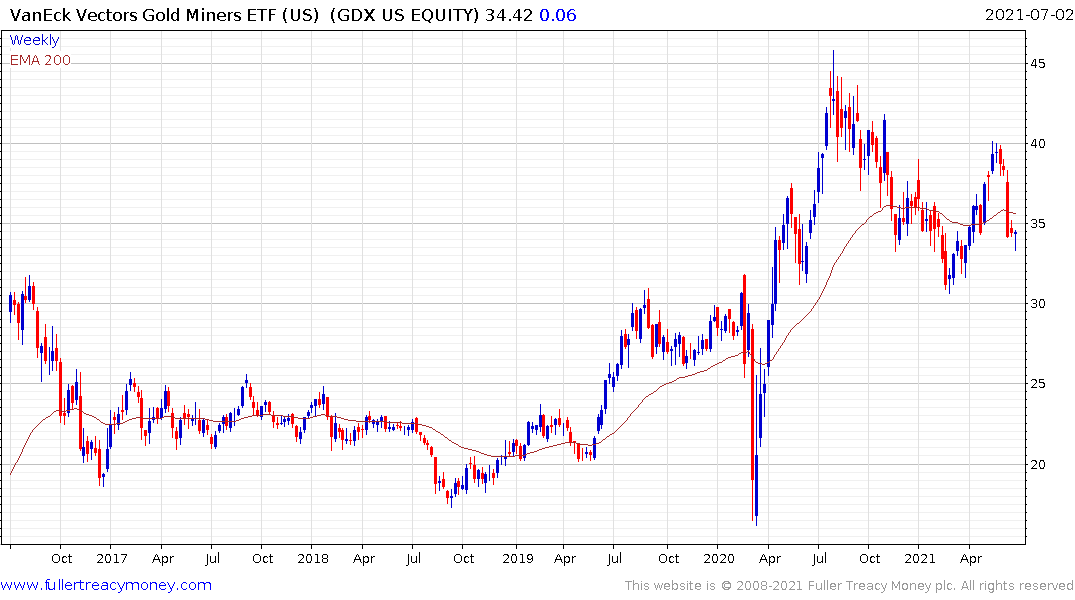

The VanEck Vectors Gold Miners ETF is also potentially forming a higher reaction low.

The VanEck Vectors Gold Miners ETF is also potentially forming a higher reaction low.

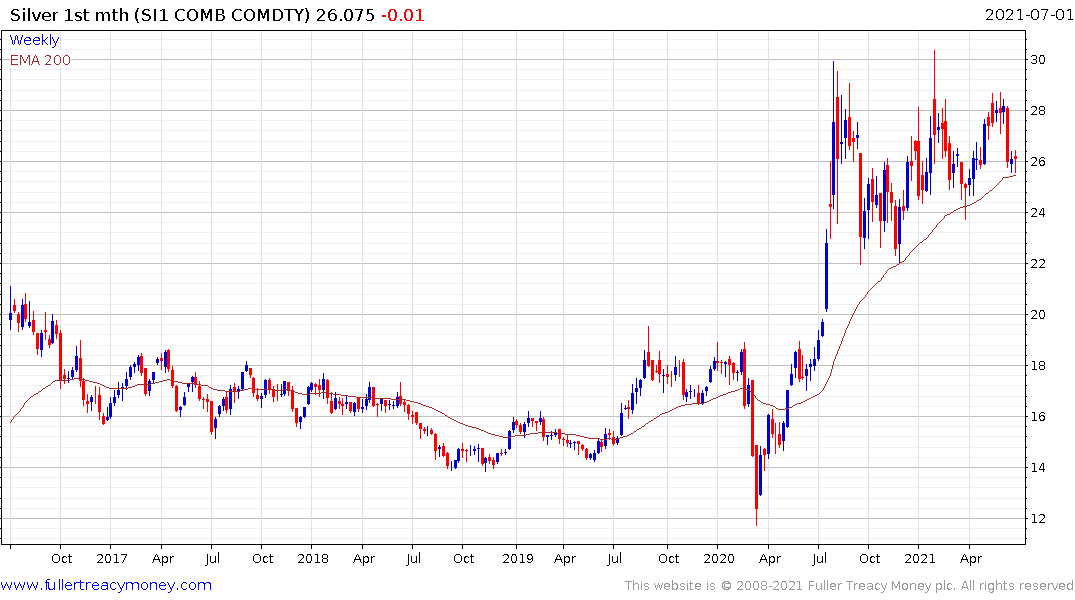

Silver continues to hold the region of the trend mean and can be expected to outperform over the remaining balance of this evolving secular bull market.

Silver continues to hold the region of the trend mean and can be expected to outperform over the remaining balance of this evolving secular bull market.

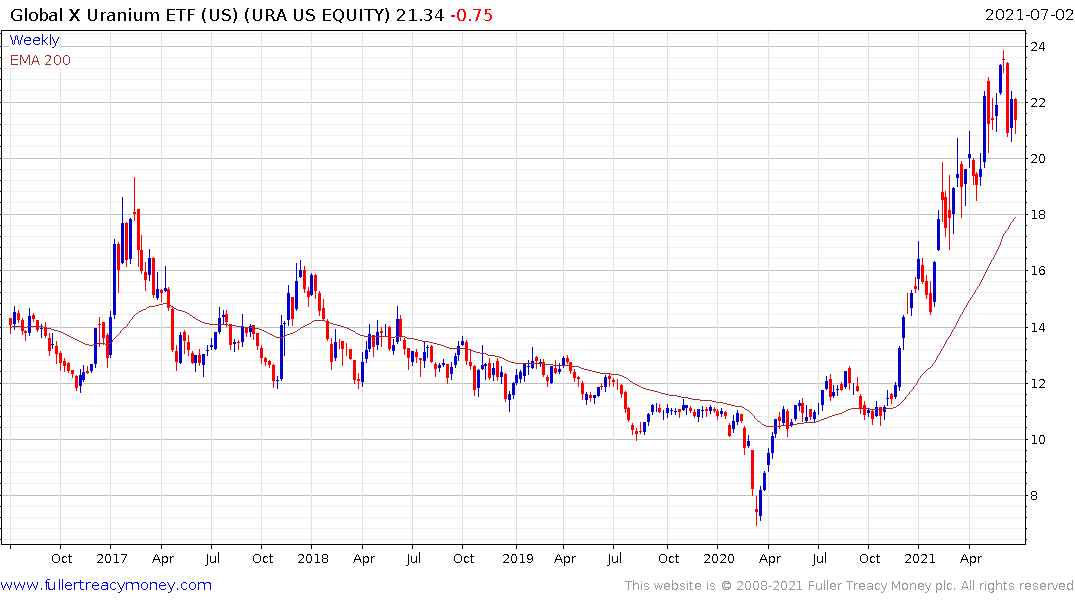

The intermittency of solar and wind where on full display this month with California needing to ration power and asking people to only charge electric vehicles at night. The market for a carbon neutral base load electricity provider remains a secular growth story.

Uranium is a contender and not least as innovative new reactor models are built and tested.

Hydrogen might be viewed as an energy storage story since the majority of production plans are focusing on renewable energy. Just this week Kazakhstan permissioned a 45 gigawatt project. Since the Asian Renewable Energy hub has run into difficulties with planning, that puts Fortescue’s plans for a project of similar scale (14GW) into jeopardy too.

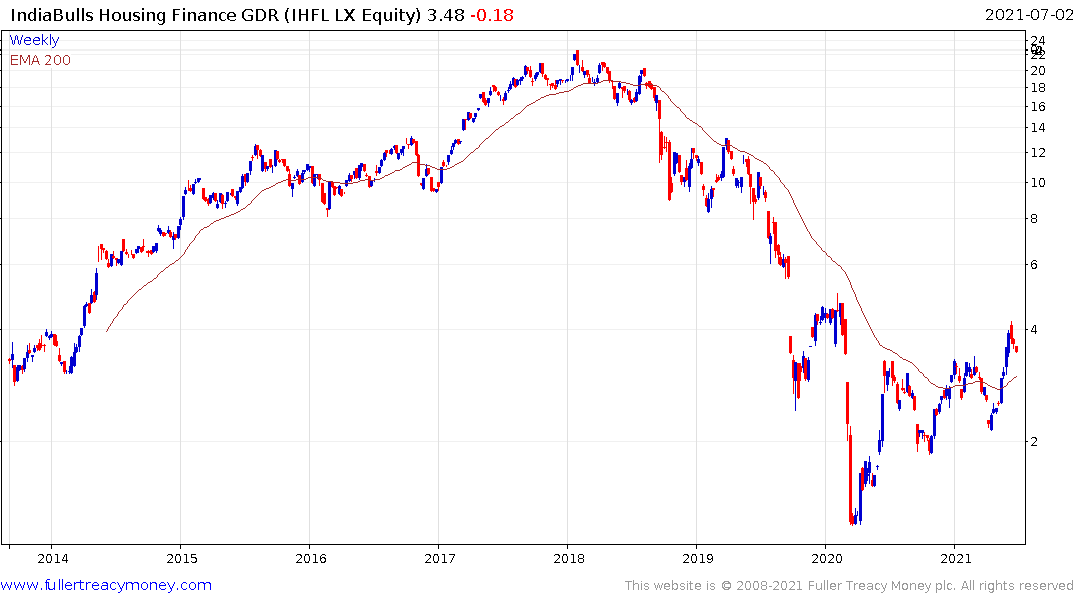

As we look at the emerging world, the Dollar’s recent strength questions the appetite for investment among international investors. However, there is still ample opportunity around the world. The Indian property market has been consolidating for at least the last five years and a number of high profile bankruptcies have shaken confidence in the sector. However, despite the negative perceptions relating to the coronavirus, a number of related sectors are breaking on the upside to complete base formations. That suggests the India property market might be turning higher.

As we look at the emerging world, the Dollar’s recent strength questions the appetite for investment among international investors. However, there is still ample opportunity around the world. The Indian property market has been consolidating for at least the last five years and a number of high profile bankruptcies have shaken confidence in the sector. However, despite the negative perceptions relating to the coronavirus, a number of related sectors are breaking on the upside to complete base formations. That suggests the India property market might be turning higher.

For a second month in a row, I see no need to repost charts of lead indicators for future recessions. None are currently noteworthy so for the majority of uptrends, occasional weakness can be viewed as a buying opportunity.

Back to top