Secular Bull Market Investment Candidates Review February 2021

On November 24th I began a series of reviews of longer-term themes which will be updated on the first Friday of every month going forward. The last was on January 8th. These reviews can be found via the search bar using the term “secular themes review”.

Highlighting secular themes has been a hallmark of this service for as long as I have been a part of it. I first met David Fuller in Amsterdam in 2003. He was giving a talk to Bloomberg’s clients and we went out for dinner that evening. His way of looking at markets, with a focus on suspending ego to see what the market tapestry is telling us, answered all of the questions I had about how to interpret markets. I felt honoured when he asked me to come work with him a few months later.

The easy way to find secular themes to is to look at long-term ranges. Prices can so sideways for a long time, sometimes decades, and the whole asset class can be forgotten by investors. These kinds of markets need a catalyst to reignite demand. Once that new theme gathers enough pace, prices break on the upside because the supply side is not capable to responding in a timely manner to the new phenomenon. Sometimes that’s because they don’t believe in the new trend, or it may be because they simply do not have the financial wherewithal to expand. As the power of the new catalyst gathers, it takes time for supply to respond and the market will proceed higher until there is a robust supply response. That can take a long time because demand continues to grow as the new theme increases its dominance of investor attention.

In the last few months, large numbers of international stock markets, which have been ranging for more than twenty years broke on the upside. That’s not a mistake and it is happening for a reason.

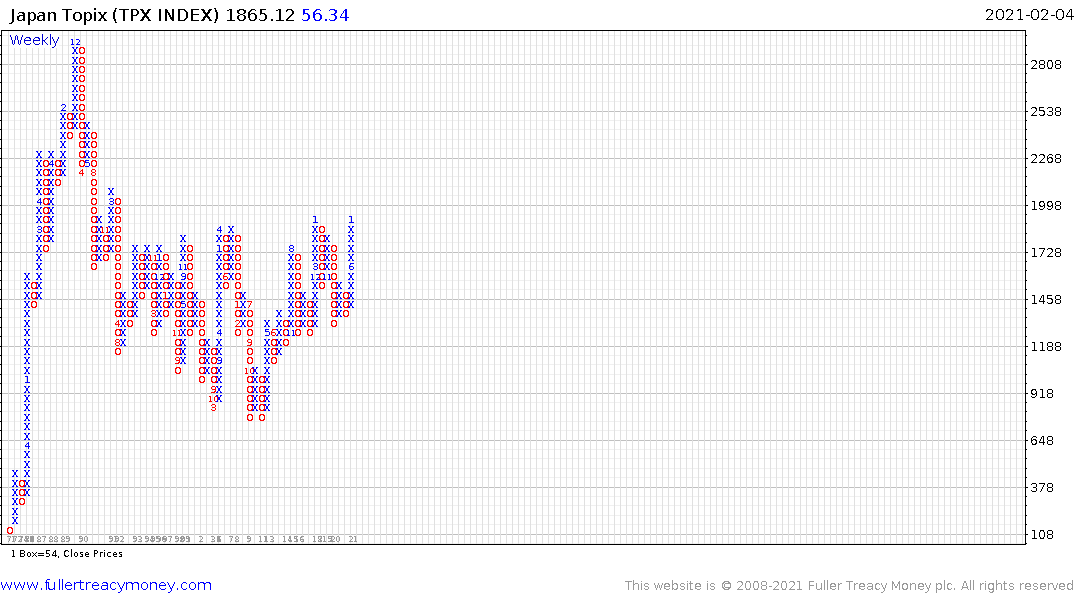

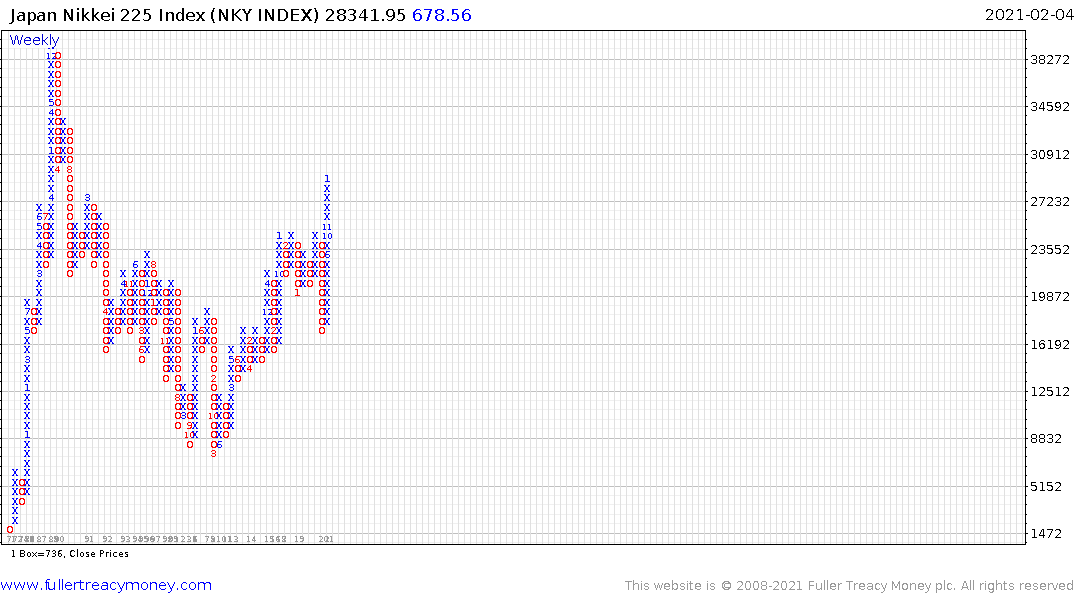

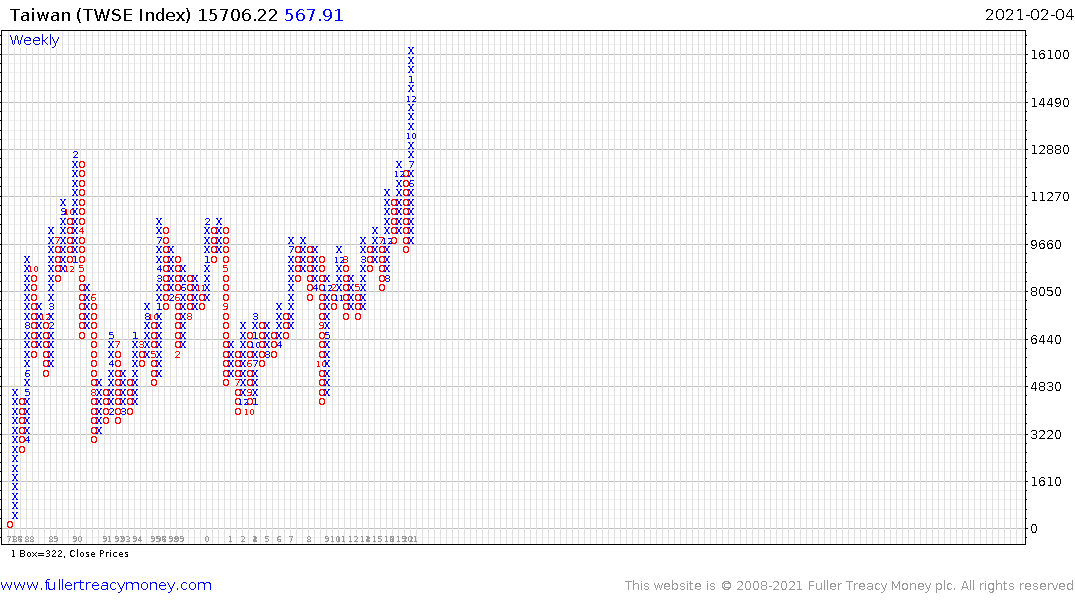

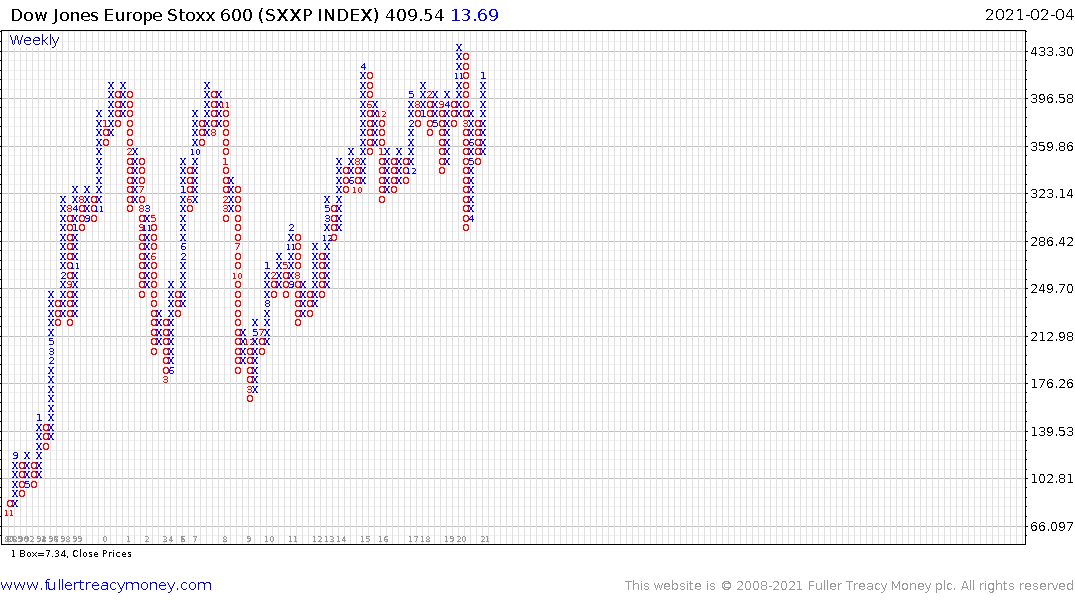

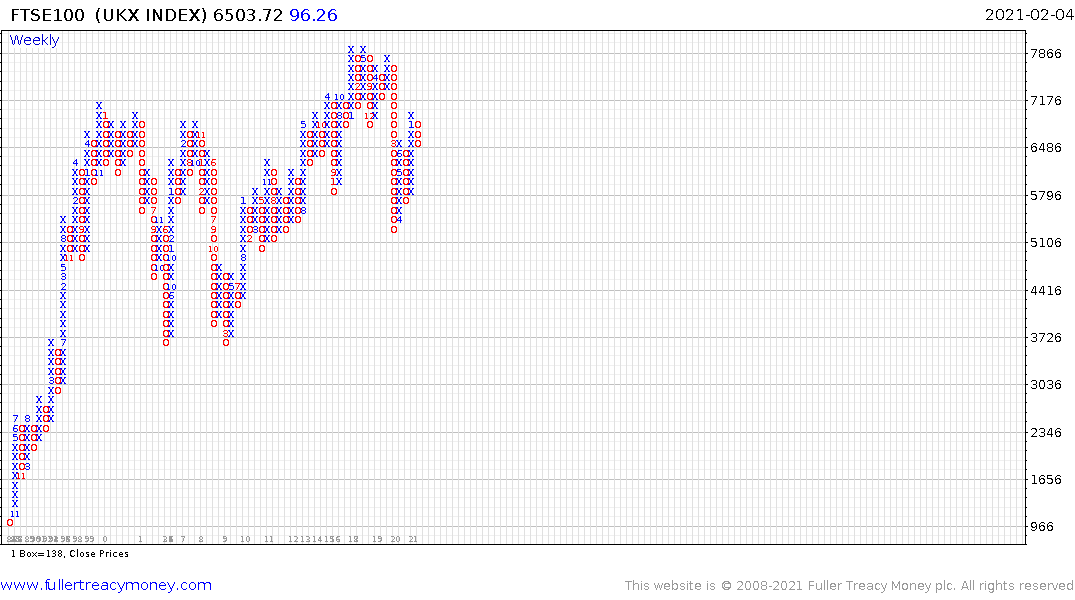

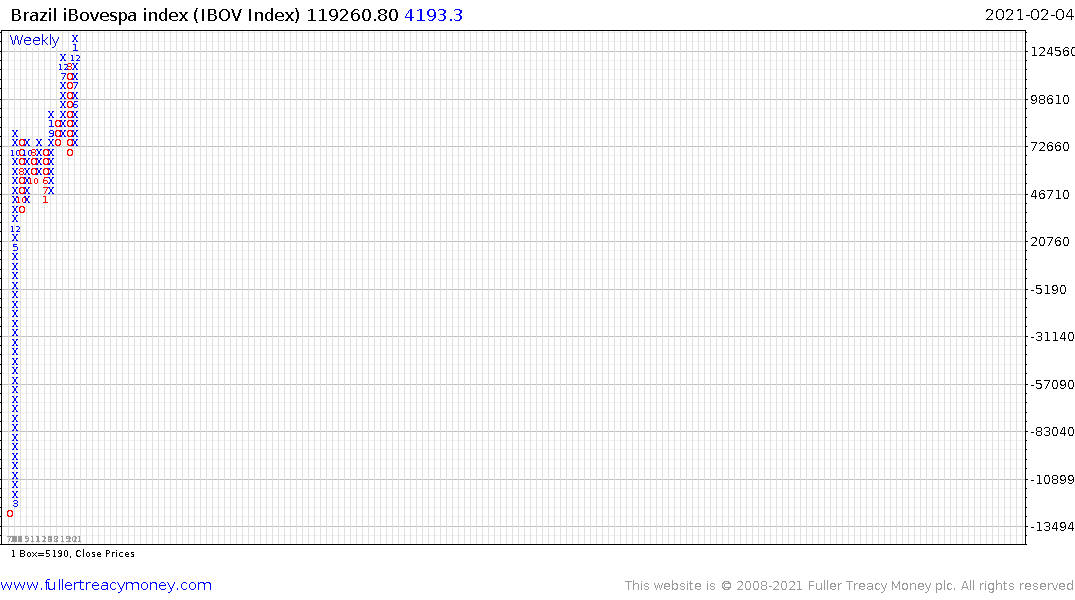

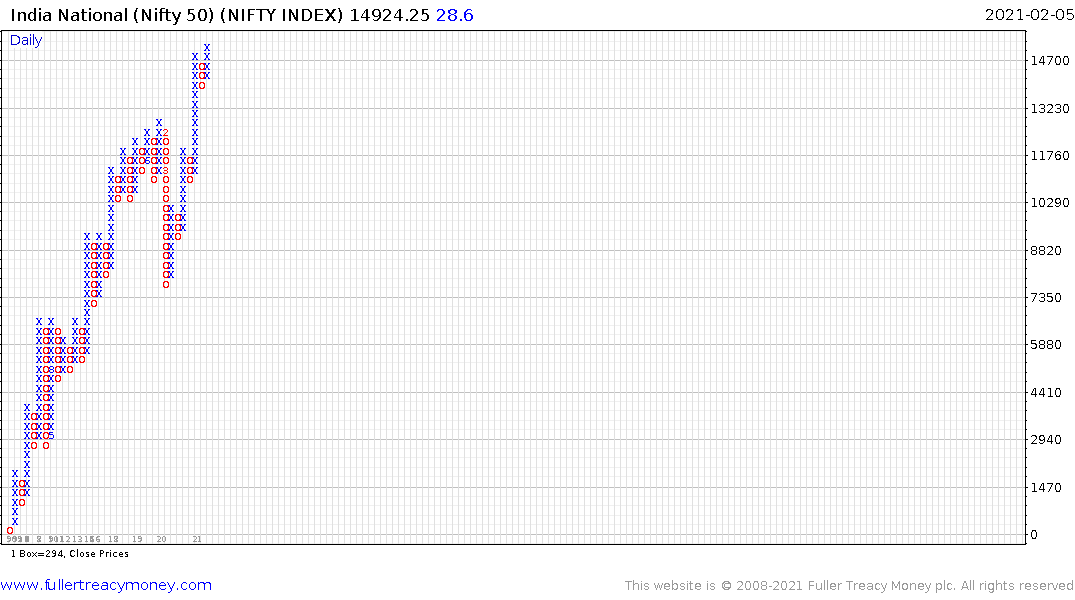

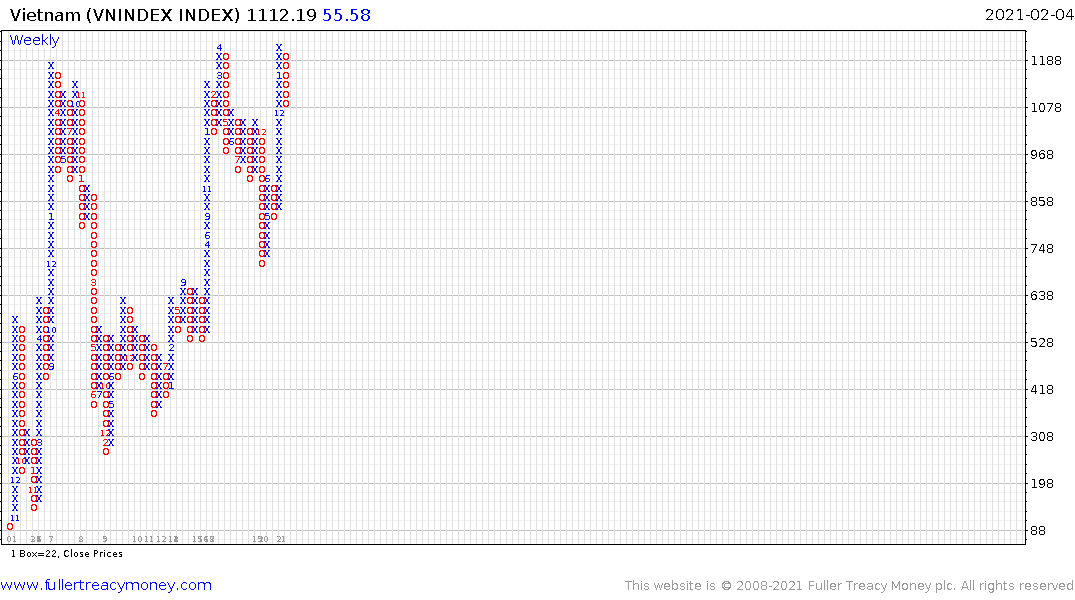

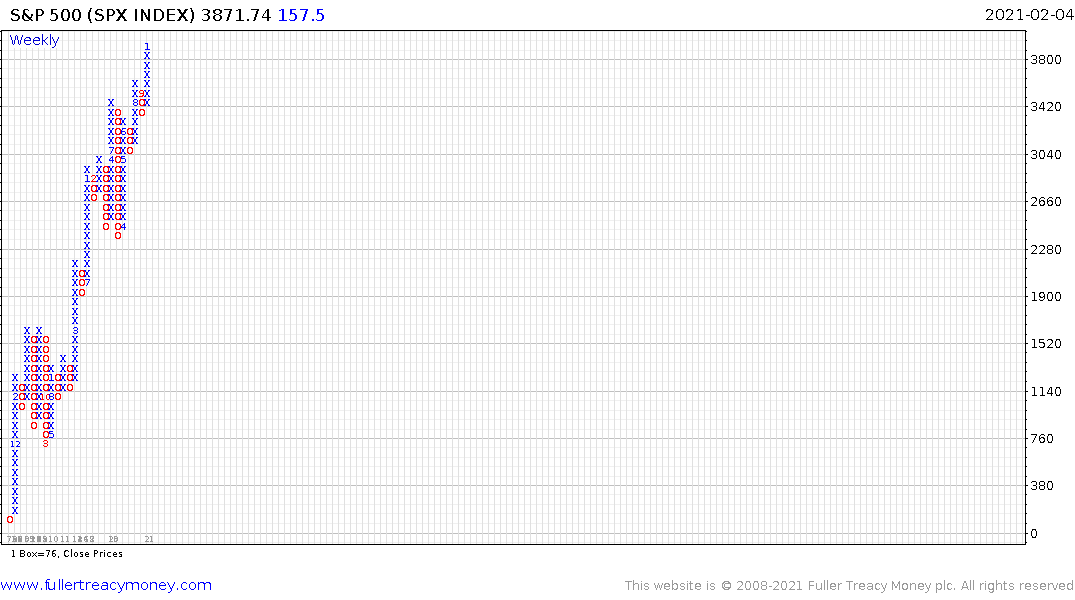

I thought this month I would focus on long-term point and figure charts. They compress time but help to clearly illustrate base formation completions and long-term trends.

Japan, Taiwan, Europe, the UK, Vietnam, South Korea, South Africa, Brazil, India, Vietnam, the S&P500 and Nasdaq-100 have all broken out to new highs.

.png)

There is a clear difference between the trends in the US markets versus everywhere else. Wall Street, led by the technology sector has been the market leader since 2008 and it continues to perform in nominal terms.

In relative terms two things have changed in the last few months. The first is that small caps have moved to outperformance versus the mega-cap heavy Nasdaq-100.

The second is that international markets are rallying at the same time as their currencies are appreciating.

Combined these two trends suggest that there is a migration out of the one-way bet on continued outperformance of Apple, Amazon, Alphabet, Microsoft, Facebook and Tesla. That doesn’t mean they are about to collapse but they are much less likely to outperform now that they represent such a large weighting in the primary indices.

The one sector which is particularly susceptible to the fate of companies like Tesla is anything to do with the Environmental, Social and Governance theme (ESG). The reason it has been able to generate such strong returns is because of holdings like Tesla which are trading on extraordinary multiples. Many investors feel good about having ESG positions but few have any conception of what is generating the higher returns in these portfolios.

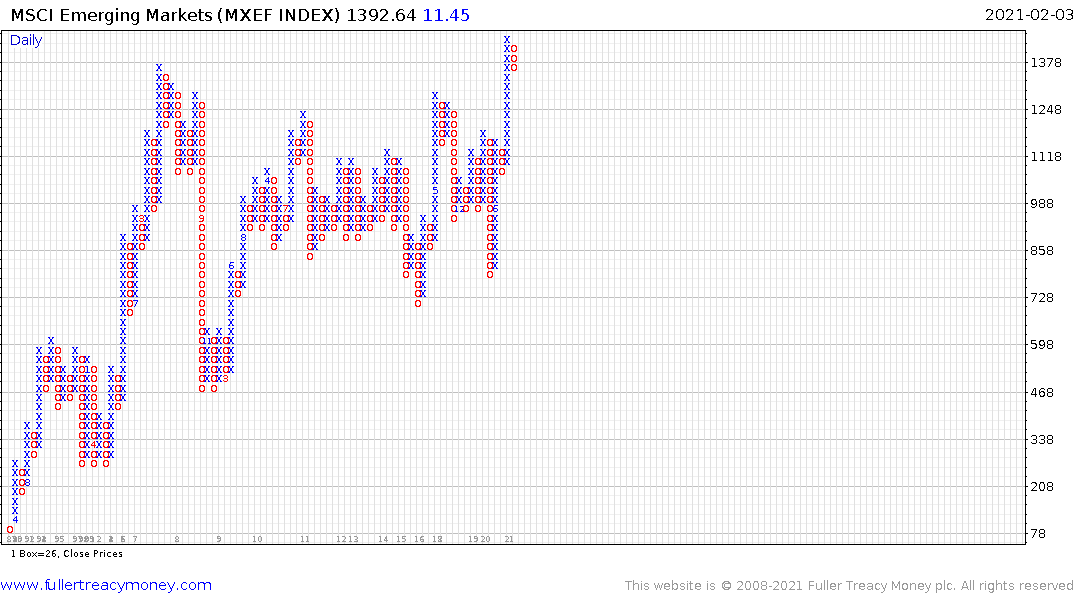

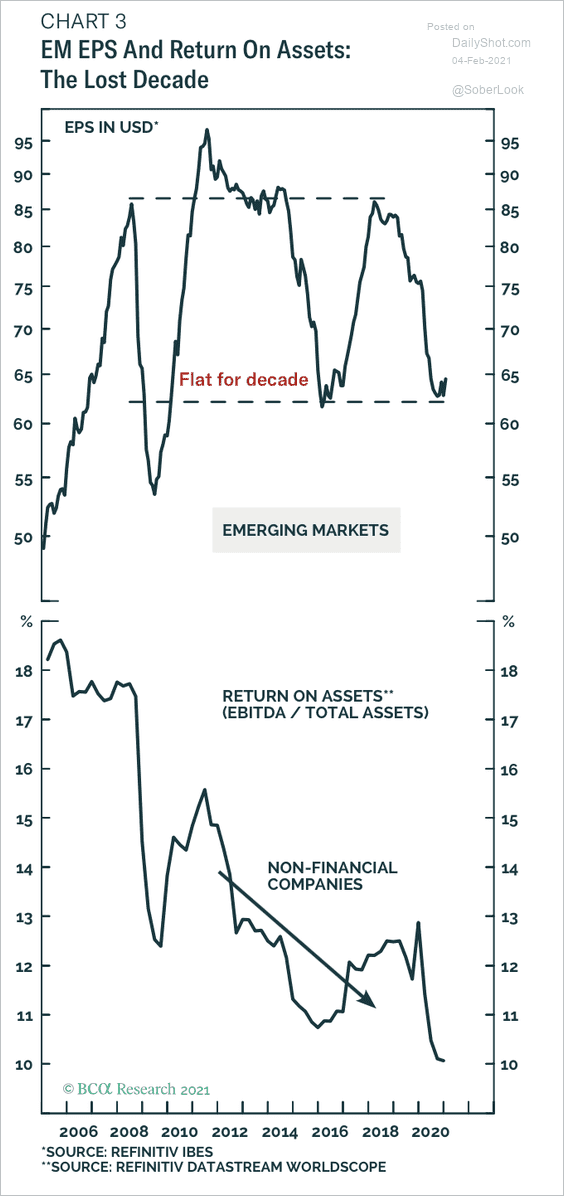

High valuations alone do not lead to one market peaking and another breaking out. Emerging markets have not had a good decade. They were over reliant on demand Western demand for their products and the sedate pace of consumer demand growth in the developed world led to a lengthy period of subpar earnings growth in emerging markets. China’s 40% weighting in the MSCI emerging basket has also contributed to that condition.

The fact that emerging market stock markets are breaking on the upside suggests that situation is now changing. The reality is Asia has taken less of a hit from the pandemic, the economies are now more focused on regional trade and they have large young populations to create demand for all manner of goods and services.

Instead of high valuations driving investors to Asia, it is probably more a story of high debt. The biggest challenge for the continued outperformance of the USA is the massive debt burden. The country was running a substantial deficit heading into the pandemic and it ballooned in 2020 to at least 15% of GDP. There is no plan for how to repay the debt, how to remove new larger unemployment benefits or how to reintroduce evictions and foreclosures. These kinds of debts don’t just fix themselves.

The only way to tackle debt mountains is default, restructure or inflate. Countries that can both print and issue debt in their own currencies do not default. The pain for restructuring social commitments never happens without a crisis to force it, so the logical course of action is to inflate. That is what the Fed’s new inflation target is aiming for. We are going to be in a negative real interest rate environment for the next decade.

There is a running argument at present about whether the Fed will in fact hold to its interest rate policy when inflationary pressures mount. The bigger question is whether they will have any choice. The alternative is worse. Europe is in a similar debt condition but stock market valuations are much lower on aggregate.

Inflationary pressures build over years and the early stages of the cycle tend to be positive for the stock market which is exactly what we are seeing today. Inflation helps to boost wages, gives companies pricing power and creates the façade of prosperity. The bounce back from the pandemic is being priced in at present. There has been a significant boost to savings, and people are thirsty of social contact. They tend to stream into social settings as soon as lockdowns are relaxed and there will be a joyous return to life as normal when the threat, perceived or otherwise, is behind us.

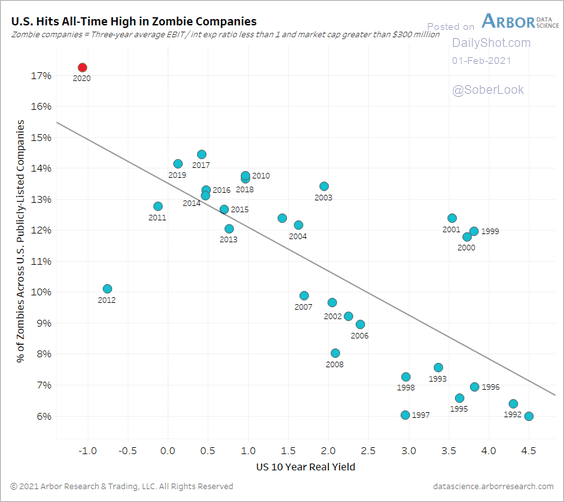

It is only later that the ability to service debts becomes a problem. At present more than 17% of all US companies are categorised as zombies. Against that background, there is just no way the Federal Reserve can raise interest rates. That’s positive for the stock market but the Dollar will ultimately provide the pressure release valve.

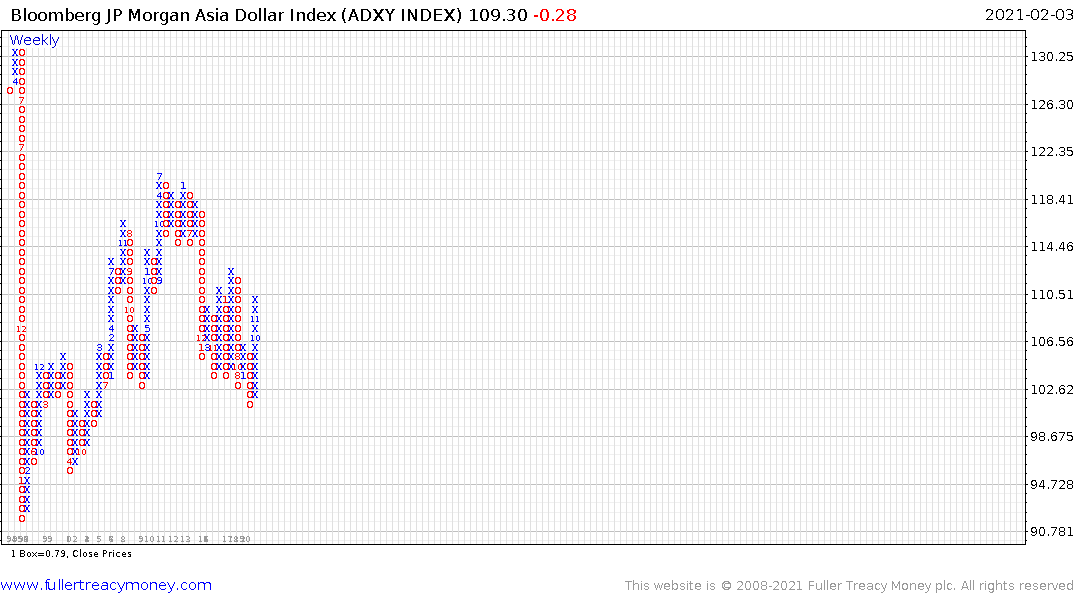

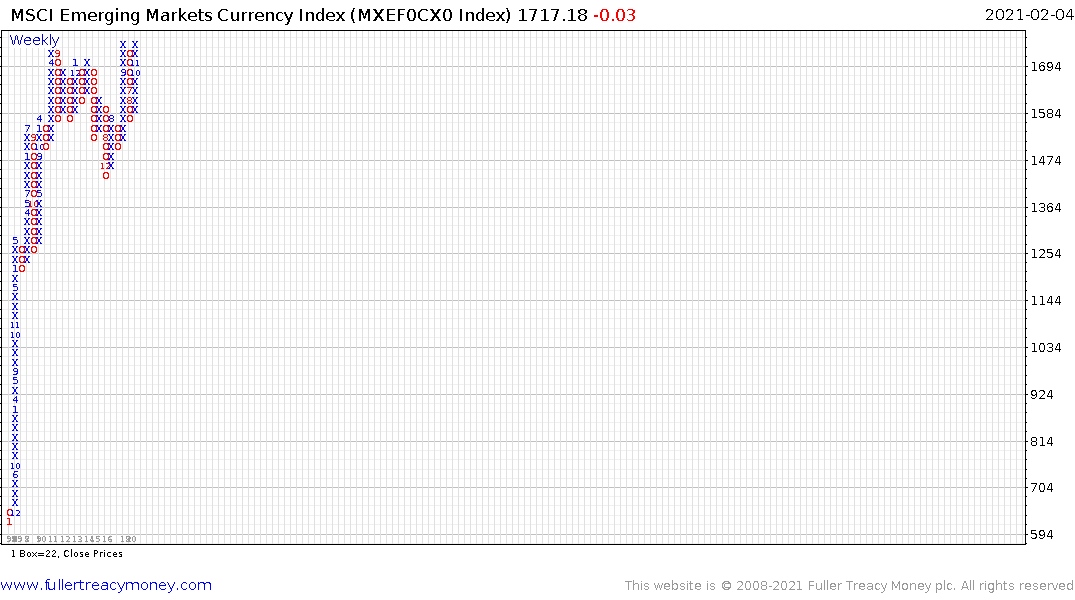

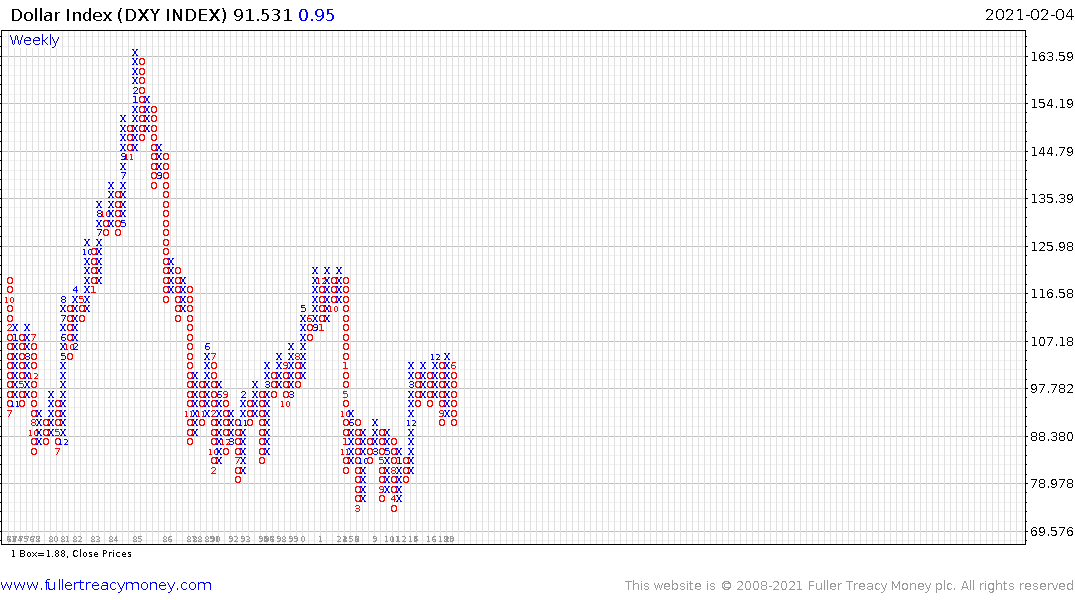

The Dollar Index tends to move in 7-year trends with some messing around in between. Right now, it is experiencing a short covering rally but that is unlikely to last as yields rise. It is only a matter of time before the next injection of liquidity to support the government and boost liquidity.The Asia Dollar Index has base formation characteristics but the MSCI Emerging Markets Index and the MSCI Emerging Markets Currency Index have been ranging for a decade and look primed to break on the upside.

The easy conclusion is that global markets are more likely to do well when inflationary pressures rise than the USA because of the valuation and debt issues.

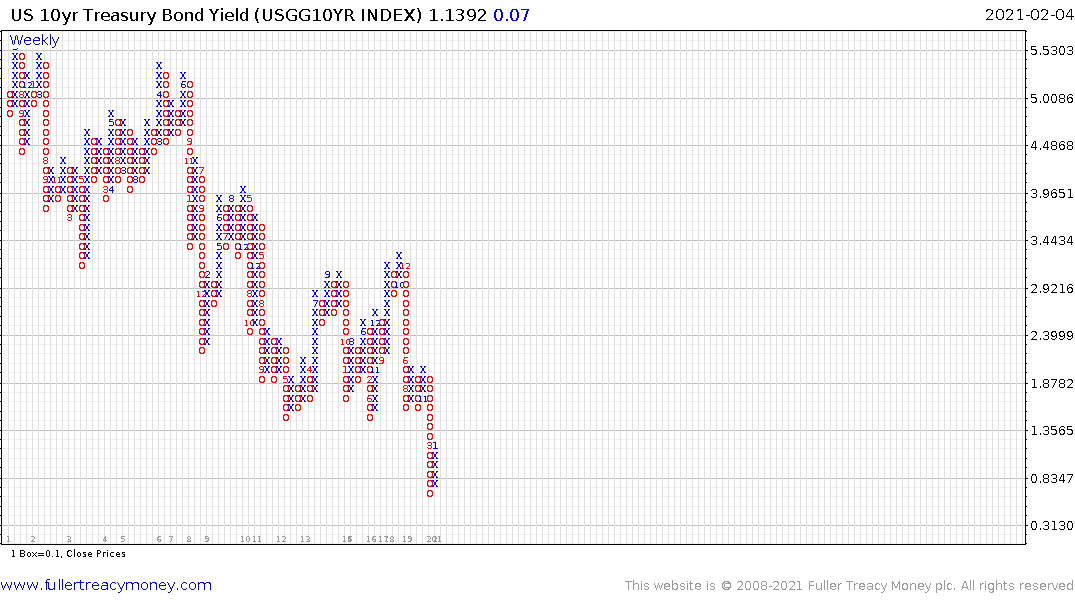

Meanwhile Treasury yields continue to exhibit base formation completion characteristics and the 10-year Breakeven Index is trending higher.

Concurrently there is no perception of risk in the corporate bond market as high yield spreads plumb new depths. The rationale, of course, is that the Fed will bail out any and all problems that may arise with companies unable to meet their obligations.

Back in March 2020 Treasuries yielded 192 basis points less than the S&P500. Today that figure is -32 basis points. Since 2009 whenever Treasuries yielded +100 basis points more than equities it signalled the onset of a significant correction. The big question at this stage is whether that 100-basis point level is still relevant given the large quantity of debt now outstanding.

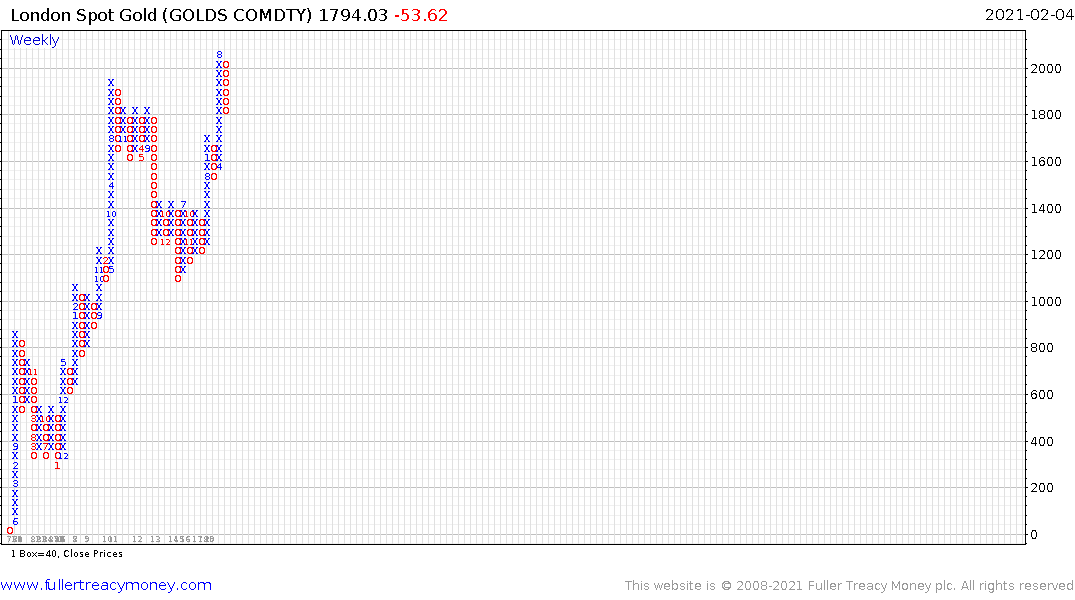

Gold is in a secular bull market because of these broad macro issues. As a hard asset its value should rise in line with the pace of purchasing power destruction. At present, risk assets are still trending higher so the desire for a safe haven asset is moderating. That is setting up the next favourable entry point for the asset class.

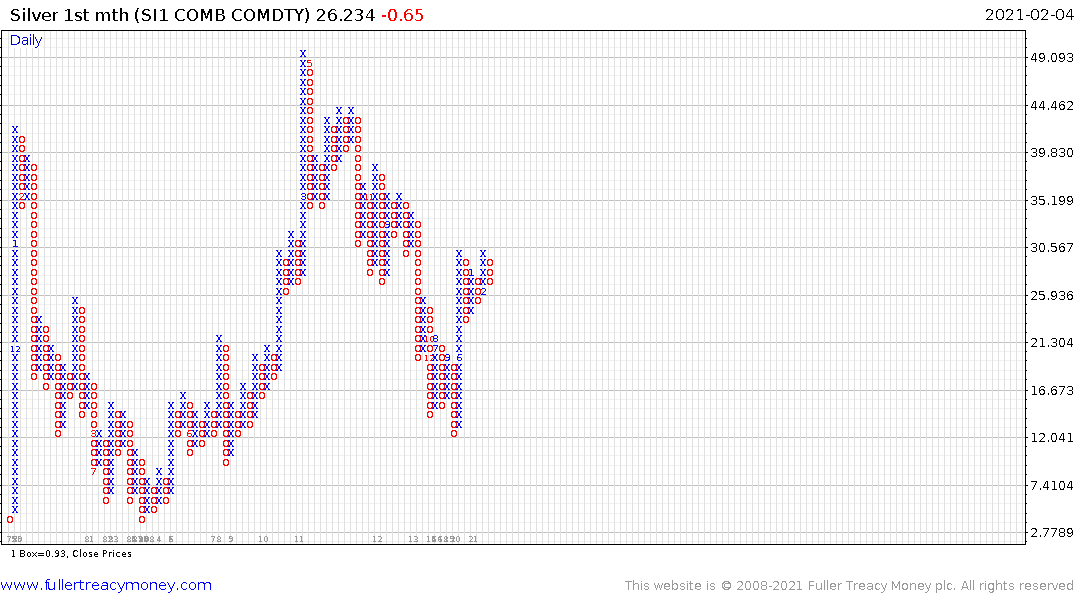

The relative strength exhibited by silver during this correction is consistent with my view that it will continue to lead into the peak of an emerging secular bull market. These moves do not occur in a straight line and there will be bumps along the way, some will be severe, but the trend is clear.

All of these markets have plenty of back history so we have some context to frame a view of long-term cyclicality. However, we also live in an age of accelerating technological innovation. That means we often do not have a long-term history to rely on for clues to future potential.

To understand the potential of technology we need to look back at past cycles of change and apply the lessons we have learned from past technological eras. There is some argument about whether this is the 3rd or 4th Industrial Revolution but each one before us coincided with a secular bull market.

I found this article from Federal reserve Bank of New York focusing on bitcoin to be a measured look at the sector. The point made that blockchain is a wholly new transaction method is relevant because it speaks to the long-term potential for the market. In the past transaction enhancements where writing, telegraph, telephone or internet resulted in paradigm shifts. That is most likely for the financial sector as the range of possible functions that can be fulfilled by blockchains and other networks increases.

Fintech ETFs which do not rely on cryptocurrencies continue to perform well and represent an additional angle on this rapidly emerging sector which has significant scope to disrupt the payments sector. The Invesco KBW Fintech ETF (FTEK UK) or the ARK Fintech Innovation ETF (ARKF US) have similar patterns and focus on holdings in Square and PayPal among others.

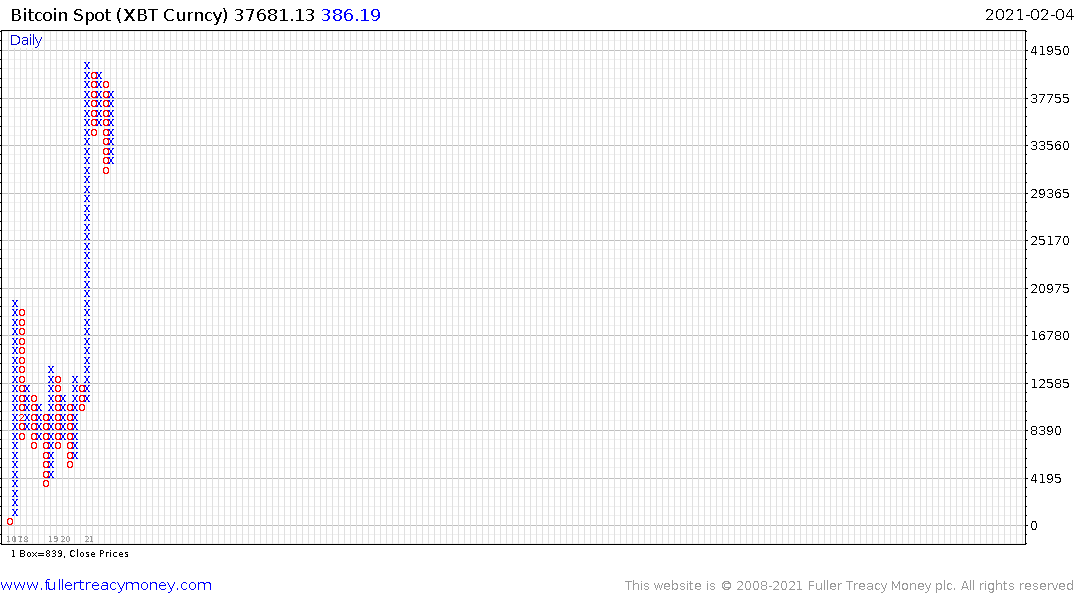

Bitcoin’s primary consistency characteristics are that following medium-term peaks it finds support in the region of the 1000-day MA. Today that’s at $8740.

After the peak we have seen a number of medium-term ranges that have last from between 2 and 3 years with breakouts occurring after the cyclical halvening events. The last halvening was in May 2020.

The most consistent thing in any trend tends to be size of the reactions. During the bull market in 2017 reactions of 40% were normal. The current reaction is sitting on about 30%. That’s larger than the 20% reactions seen since March, so the $28000 level will need to hold if the upside is to be given the benefit of the doubt.

There is also some evidence that as institutional participation grows, bitcoin’s correlation with other assets will increase. For example, it peaked a month ahead of the S&P500 in early 2018 and bottomed two days ahead of it in March 2020.

It is reasonable to assume that bitcoin has been a major beneficiary of low interest rates and abundant liquidity. Together with Tesla it has been a lightning rod for speculative flows. When its consistency changes it will be a warning sign that the liquidity of the wider market is also changing.

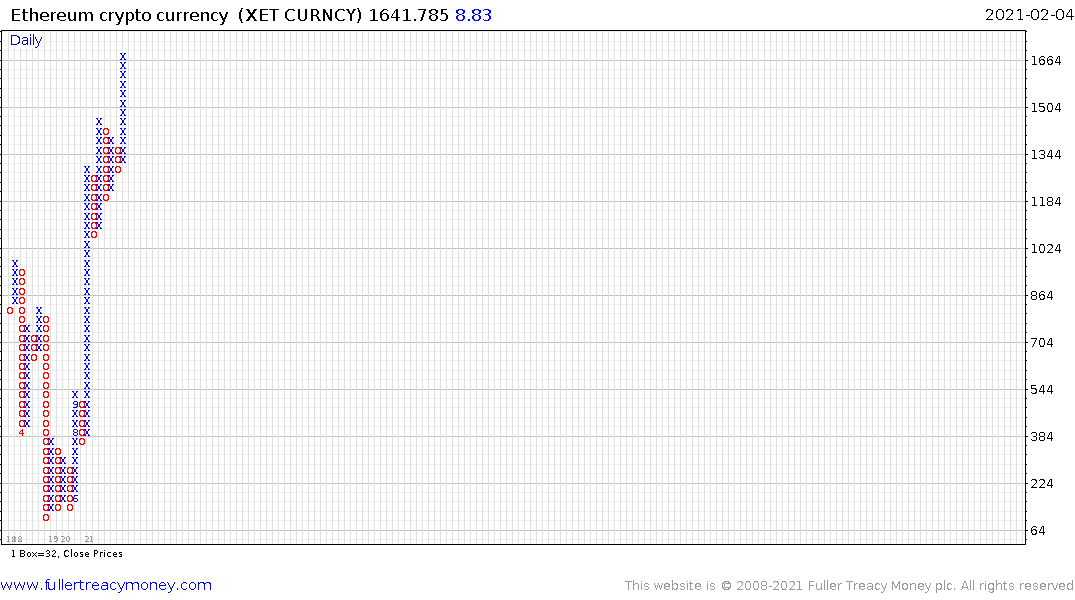

In much the same manner that silver is high beta gold, Ethereum is high beta bitcoin and is continues to outperform.

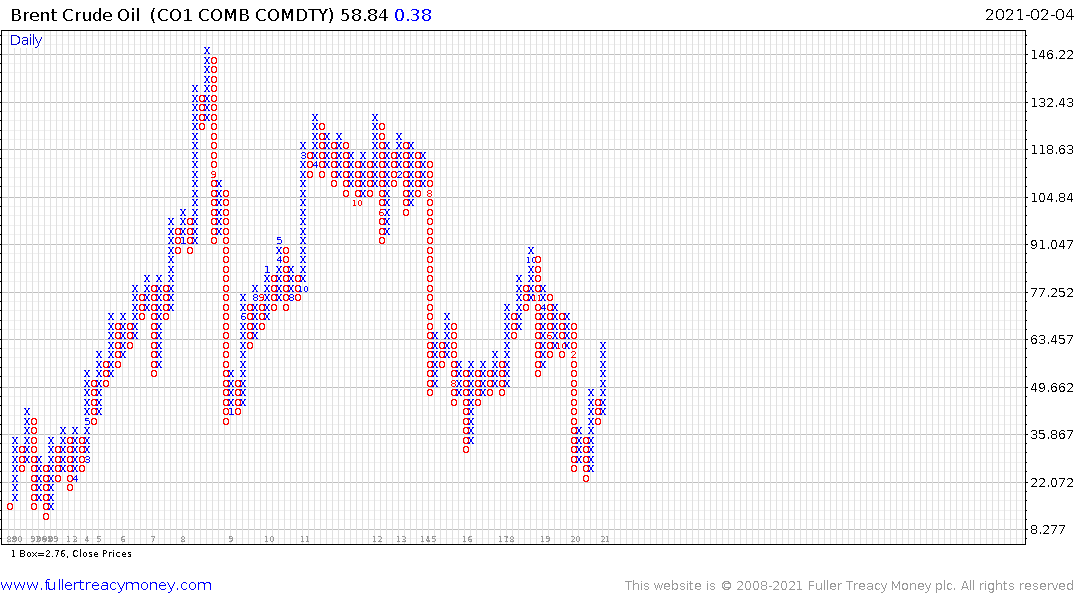

The big theme in many people’s minds today is the energy transition. Oil is thought of in much the same terms as coal was a decade ago. Yet even though attitudes towards coal continue to sour, the commodity is still actively traded and new coal fired power stations continue to be built. There is a perception that oil will be irrelevant as the globe electrifies. Instead, higher cost producers will be shut out of the market and the most efficient producers will garner market share. The simple fact is gasoline is more energy dense than the best batteries and that is likely to remain the case for the foreseeable future.

Oil prices remain on an uptrend as the outsized decline in 2020 continues to be unwound. $60 is about where breakevens reside so supply shortages would be required for prices to trade sustainably above $80.

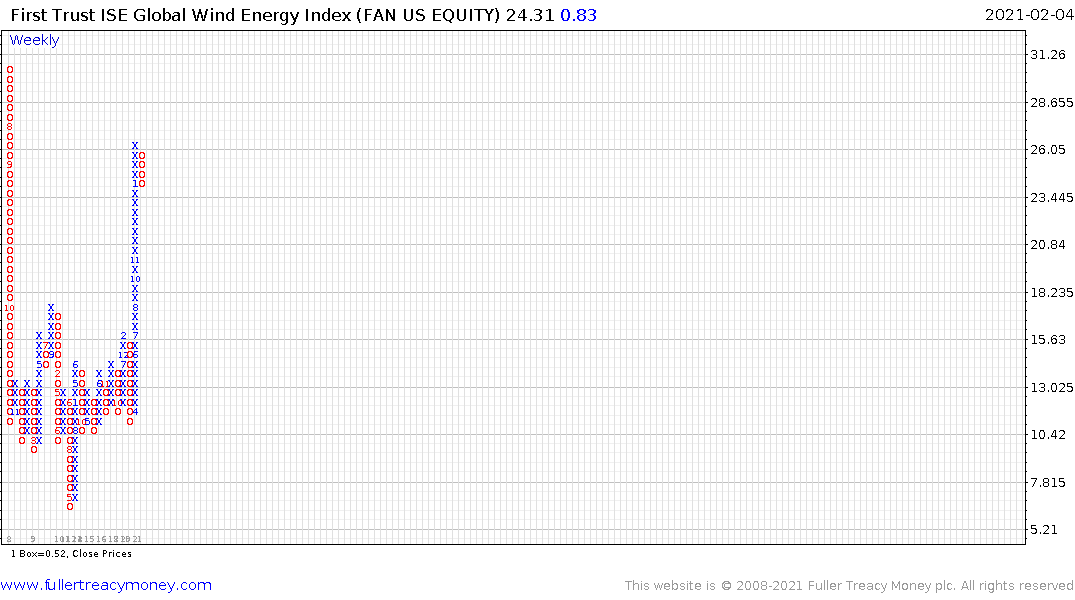

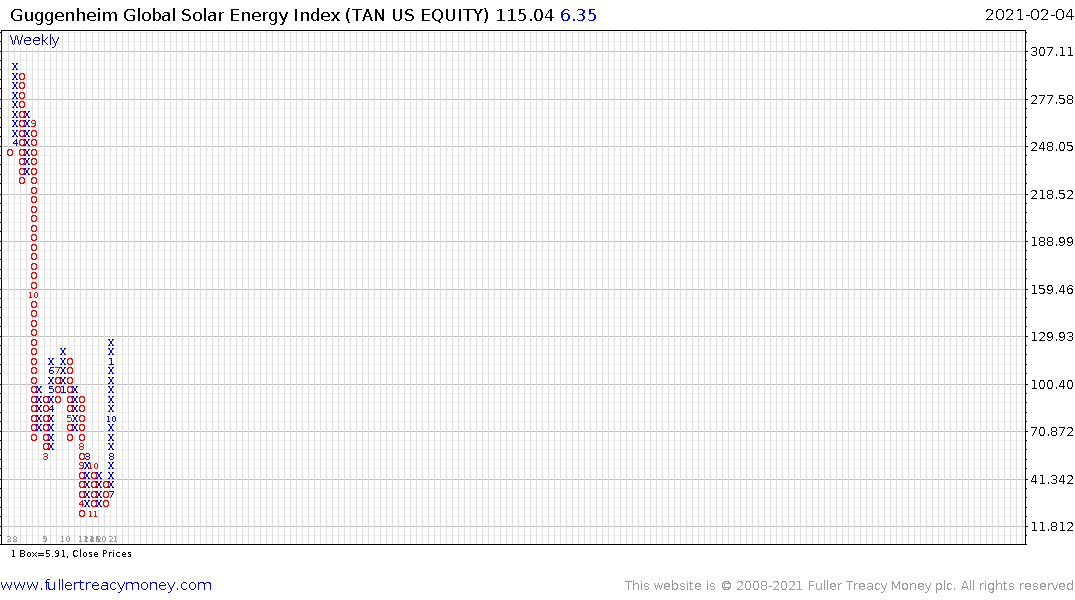

Meanwhile the trajectory of evolution in the solar and wind sectors remains positive. The efficiency of both continues to improve and economies of scale have delivered lower prices. The continued desire to reshape the global economy on a low emissions basis is fuelling demand for both sectors. The respective ETFs continue to extend breakouts from their respective base formations.

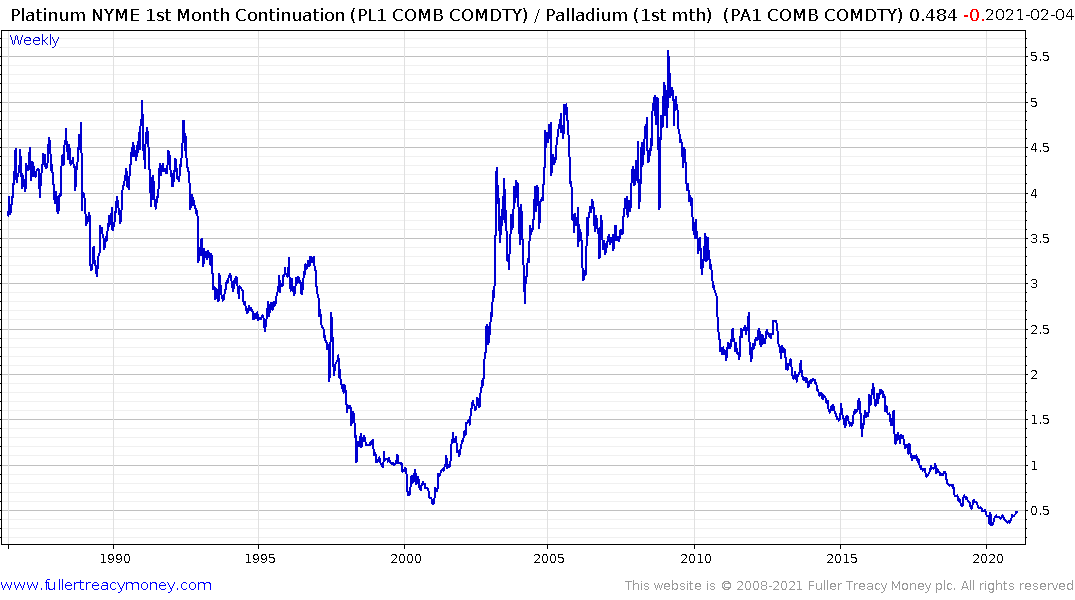

The platinum/palladium ratio has reversed. If this recovery continues it will signal a clear trend of migration from support for catalytic converter metals and into hydrogen fuel cells. It’s about the best graphic representation I can think of for the transportation migration that is only now beginning to gather attention.

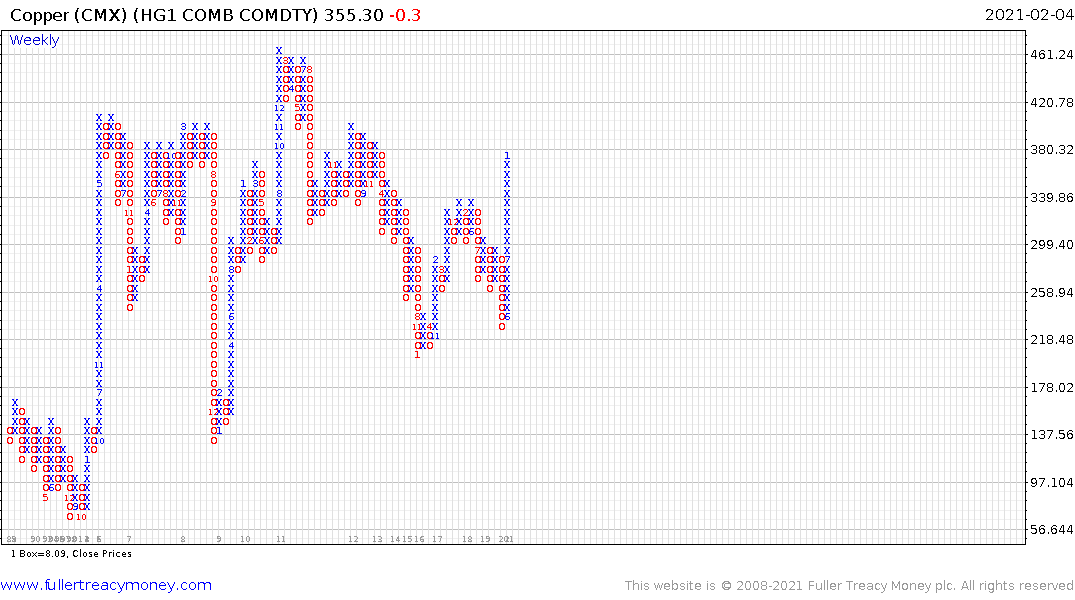

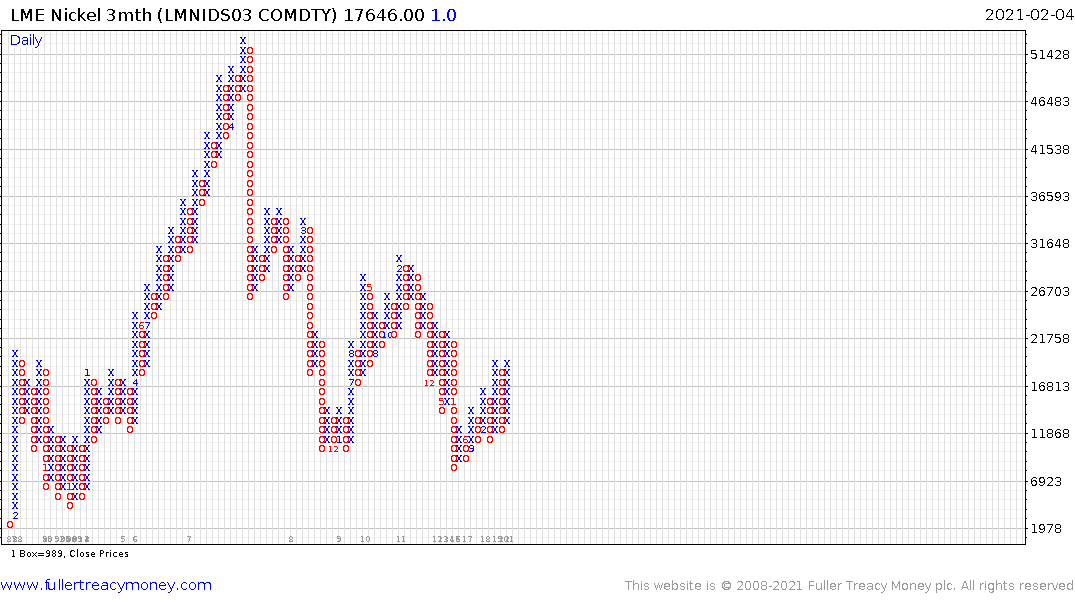

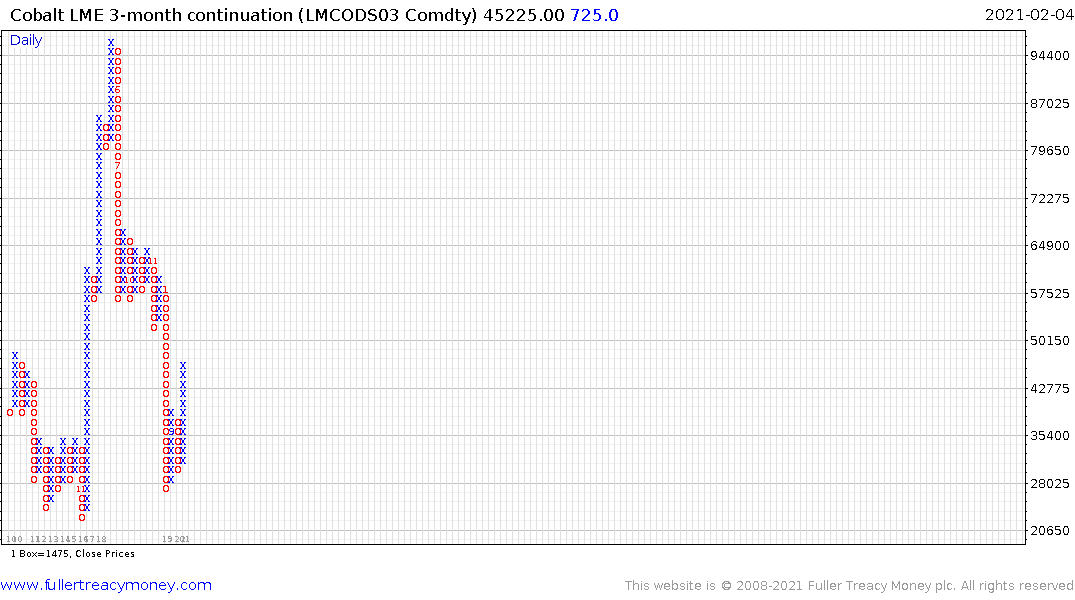

As we look at Asia continuing to take the lead in economic recovery and the massive investments required to build out electricity generation, charging facilities and electric vehicles there is going to need to be significant investment in commodity supply. That’s particularly true for copper, nickel, lithium and cobalt. If a new commodity-led bull market is going to emerge, these four metals will lead the way.

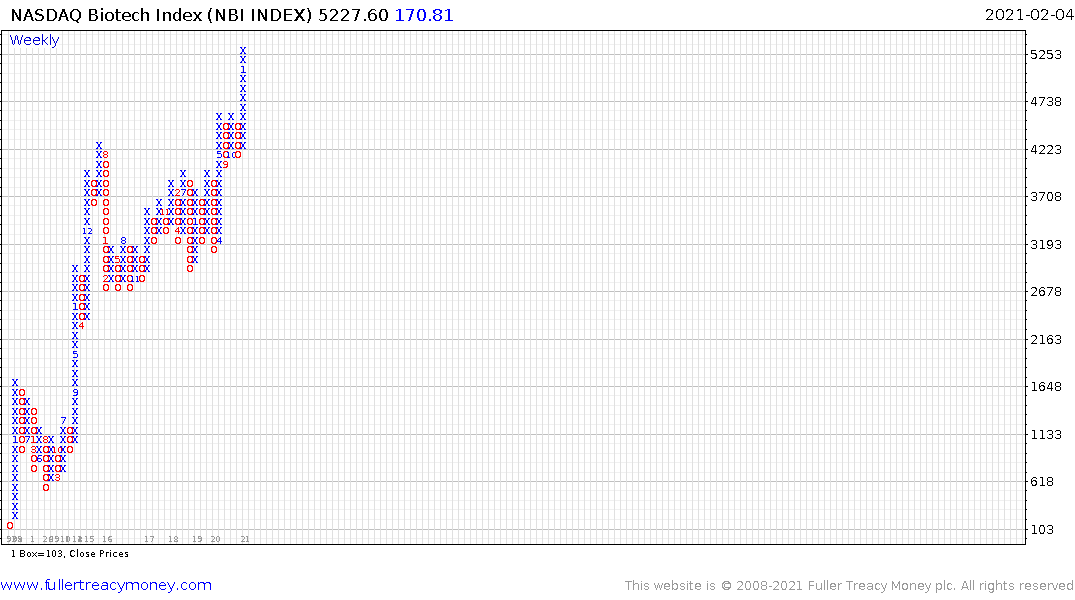

As we think about what the future holds, the pace of technological innovation is only accelerating. In the near-term liquid biopsies are going to garner a lot of attention. Today blood samples provide too much conflicting data to be useful for diagnosing cancer. We rely instead on taking samples from solid masses with less dispersion of information. Technology has progressed to the point where the data from blood samples can be analysed for cancer markers. That’s going to increase the scope for testing, reduce the time to finding cancerous growths and enhance early treatment options. Illumina acquired Grail last year to gain this technology and Exact Sciences is also in the sector.

The speed with which companies have successfully developed vaccines for COVID-19 also helps to illustrate how far genetic solutions have evolved. 2020 was a massive proof of concept exercise for the biotechnology sector and it came through with flying colours. That points to a bright future.

.png)

The legalisation and normalisation of cannabis also remains a secular theme and it will receive a significant leg up if the USA removes the federal prohibition.

If liquid biopsy is a near-term success story, quantum computing and autonomous vehicles represent massive untapped market opportunities waiting in the wings. Alphabet is a leader in both and claims exponential exponential growth in quantum computing. The deep learning algorithms pioneered by the company’s Deep Mind section are the most efficient in solving the protein folding problem. Success in shortening time scales in this one field has the potential to have multiplying effects on all manner of other sectors from materials to life science.

SpaceX and Blue Origen pioneered reusable rockets which has brought the costs of lifting a kilo of material into space down from several hundred thousand dollars to two thousand. Satellites are now also smaller and less expensive so we can anticipate that the sector is going to grow significantly. At present it is rather difficult to invest in because the most promising companies are not publicly traded.

That helps to highlight how long the potential queue for new listings could be. Just today China’s latest short-form video stock Kuaishou Technology, surged on the first day of trading. There is ample demand for new companies offering exposure to the promising, if foggy future.

There is little doubt that the multiplication factors of deep learning and the increasing ability of computers programming themselves means the global economy will increasingly rely on digital tools. For mature individuals we still tend to think of social media as intrusive. For young people it is a normal part of life. The same will occur with digital assistants.

Even so, support for continued innovation is dependent on abundant liquidity and the farther a company is from positive revenue, the more leveraged they are to interest rates.

As we look around the world, we see trends beginning in Asia and in commodities. There is evidence of some froth in parts of the technology sector. The thing to remember is that the largest companies in the world today benefitted most from the rollout of 4G and broadband.

The next batch of companies to succeed in a very big way will need to leverage the transition to digital finance, big data, connected devices and the next several billion global consumers for whom all this will be normal. The challenge is in how the interest rate environment plays out. If inflation finally makes a comeback, on a sustained basis, the buy high to sell higher momentum strategy which has been working for the last year will need to be revisited.