Secular Themes Review September 2021

On November 24th I began a series of reviews of longer-term themes which will be updated on the first Friday of every month going forward. The last was on May 7th. These reviews can be found via the search bar using the term “Secular Themes Review”.

If it walks like a duck and quacks like a duck, it must be a duck. Wall Street is behaving like it is in a bubble. The most important thing is the bubble is still inflating.

Retail investors are now a dominant force in the market and the put/call ratio is trending lower. The measure is not at the extremes of the late 1990s but it is trending in that direction.

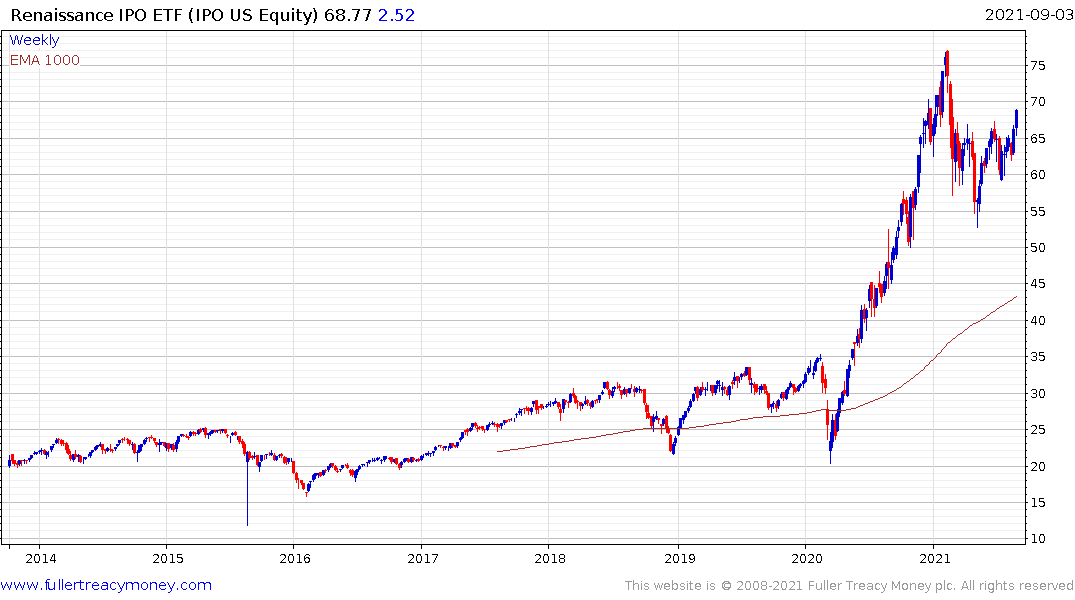

Supply of new shares, either by SPAC, IPO or follow-on listing is surging. Supply always increases as the bull market matures because the incentive to list is powerfully attractive. Additionally, the performance of recently minted IPOs continues to impress which adds further fuel to the bullish fervour.

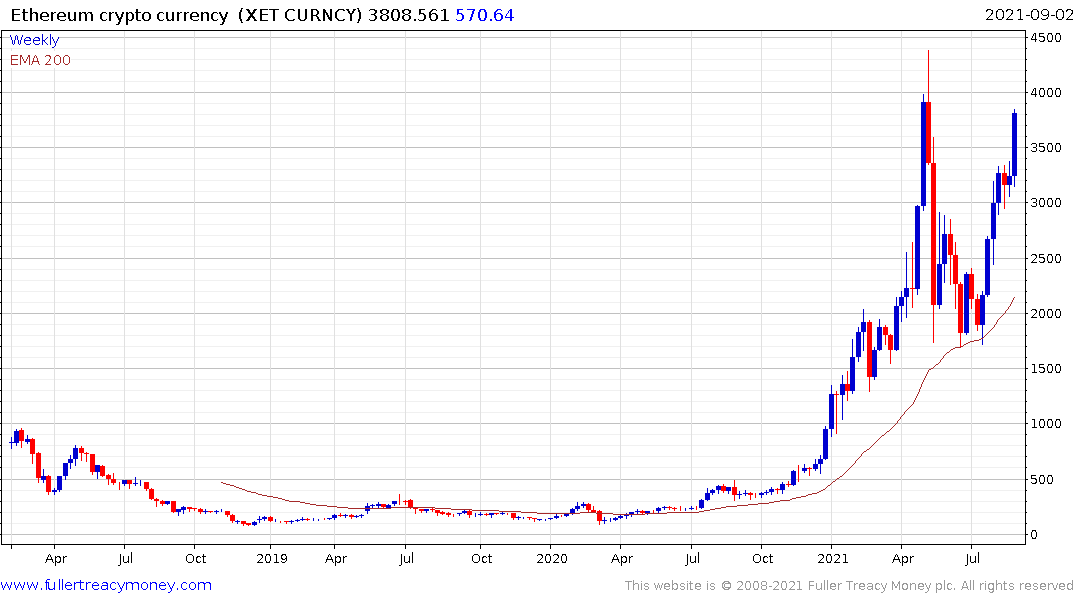

This bull market has the added spice of hosting a new market for speculation in cryptocurrencies and NFTs. The appetite for new listings is strong despite the full knowledge that what is being traded has no real-world utility.

I am reminded of the “trading sardines” story from the days of the Alaska gold rush. At the time cans of sardines were trading hands for princely sums, but no one was eating them. When someone eventually opened a tin to find they were rotten he was informed those sardines were trading not eating.

The wisdom of using cryptos to buy cryptos and to mint new cryptos is unquestioned at present, but it forms the basis for a market contradiction that will eventually be puzzled over by market historians. The fact that a pixelated graphic is worth more than Picasso’s Mother and Child is a reflection of where we are in this cycle.

Nevertheless, cryptocurrency prices continue to rebound and the recent outperformance of alt-coins highlights just how much speculation is now dominating the market.

It’s also worth considering that banks are competing for graduates and offering significant salary increases. There was even a story of a Chinese quant house offering a $300,000 salary to a PhD student. Meanwhile Fidelity is in the market for 9,000 new client facing employees by the end of the year.

These are all straws in the wind to highlight we are in the 3rd psychological perception state of this bull market. It is not especially useful to identify a bubble, the only real question is when will it pop? This is the time to remember one of David’s Fullerisms:

“Major bull markets don’t die of old age; they are assassinated by central banks”

The total assets sitting on central bank balances sheets continue to trend higher. That’s the clearest indication that we remain in a liquidity rich environment. As long as that remains the case, the surprises are likely to be on the upside.

The main topic of conversation over the last month has been the intention of the Federal Reserve to taper the number of bonds they are buying every month. It is likely to be easier said than done.

There are still a large number of uncertainties circulating. The first is that no one knows how the end of the moratorium on evictions will go. The second is no one knows if the removal of outsized unemployment benefits will suddenly fix the mismatch between the jobs being offered and the unemployed people applying for them. The fact that Amazon is no longer screening drivers for cannabis use highlights just how acute that mismatch is.

The third is political polarisation has not gone away. Civility is at a low ebb and the capacity of significant protest movements to arise is non-trivial at the first sign of any further hardship. Massive stimulus paved over a lot of cracks in the social fabric of most countries in 2020. Even a hint of fiscal austerity is likely to bring a lot of pent-up frustration to the surface.

For most of the last decade central bankers have been begging politicians to be more proactive in fiscally stimulating the economy because monetary policy can only do so much. It seems like politicians finally get the message. My custom figure for cumulative major economy deficit spending is currently sitting at $2.4 trillion. There is always a fresh rationale for fiscal profligacy, in this cycle we have the hubris to call it Modern Monetary Theory.

For most of the last decade central bankers have been begging politicians to be more proactive in fiscally stimulating the economy because monetary policy can only do so much. It seems like politicians finally get the message. My custom figure for cumulative major economy deficit spending is currently sitting at $2.4 trillion. There is always a fresh rationale for fiscal profligacy, in this cycle we have the hubris to call it Modern Monetary Theory.

When we combine the threat of social unrest with the reality of massive deficit spending, the simple reality is central banks are going to have a very difficult time in normalising interest rates. Instead, they are betting they can improve social conditions by embarking on massive environmentally inspired socio-economic experiments which will require trillions in additional spending.

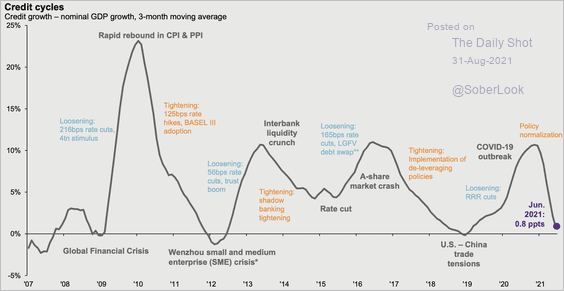

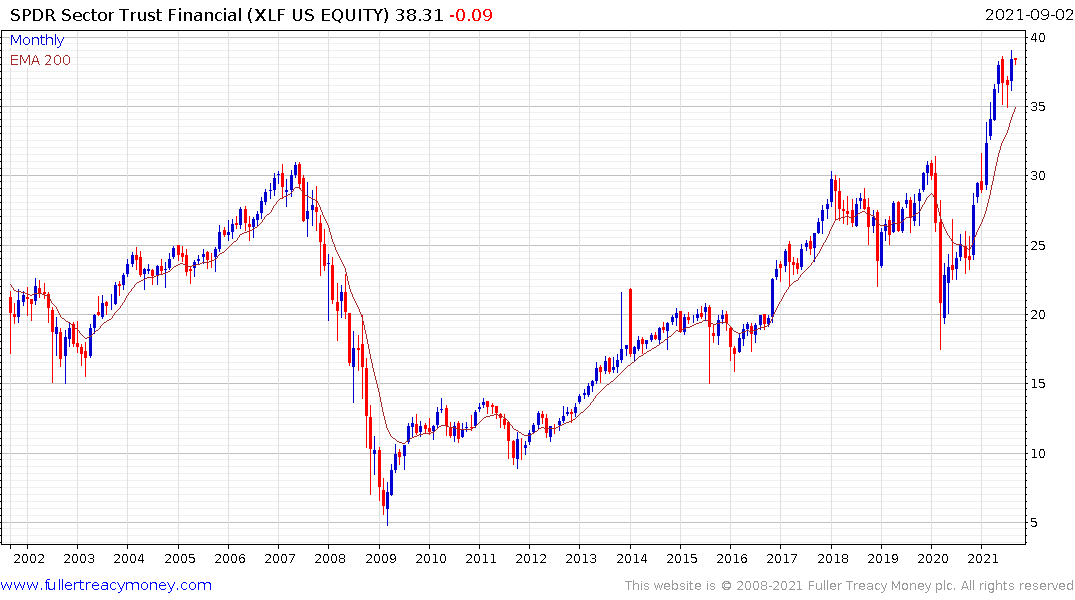

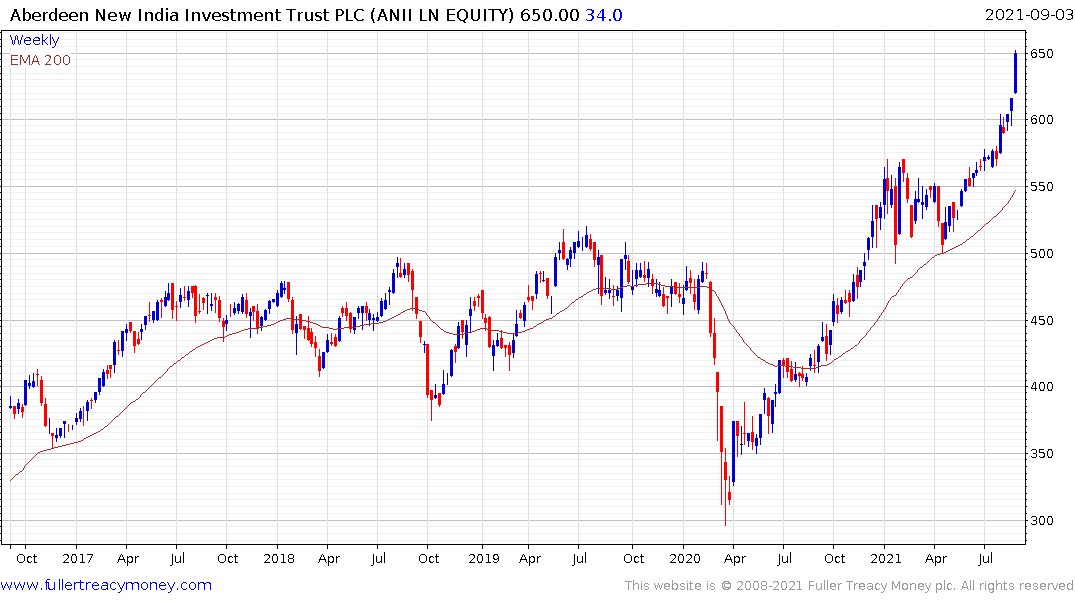

It is also looking increasingly likely that the credit cycle has bottomed in India and is currently bottoming in China. Together with what is going on in the rest of the world this suggests the global economy is on the cusp of a major credit expansion which has the capacity to fuel ever more outlandish valuations.

That’s why the banking and financial sectors are continuing to surprise on the upside.

There is already evidence of inflationary pressures. Central banks believe this is transitory in just the same way that inflation proved temporary after the shock of the global financial crisis. Commodity prices surged between 2008 and 2011, only to crash subsequently. It seems that central banks are betting this will happen again.

The counter argument to that conclusion is the global financial crisis was a major liquidity event which curtailed leverage for years afterwards. The commodity surge was fuelled by China’s determination to spend its way out of trouble by building on an unprecedented scale.

In 2020, a liquidity event was avoided and property prices have continued to increase which has greatly boosted the perception of wealth among consumers. Meanwhile infrastructure development is a priority for most countries on this occasion.

Also, the deficits being run at present are very different to what we saw in the aftermath of the credit crisis. Therefore, the odds are in favour of a more prolonged inflationary bias.

Gold has been in a medium-term corrective phase for more than a year. The fact it is has held the majority of the 2019/20 gain and is currently firming from the $1800 area supports the view that this is just a pause in an ongoing secular bull market.

Silver has been underperforming gold for most of the last year but if gold continues to firm, it will not be long before silver returns to a position of outperformance as speculative appetite reignites.

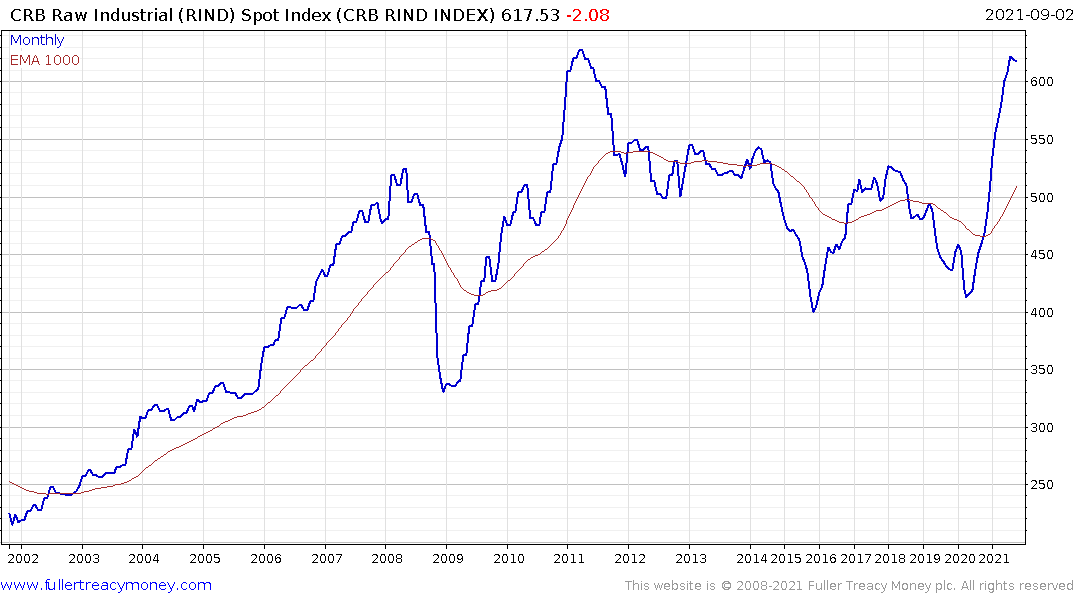

Shipping rate and raw industrial commodities have surged over the last year.

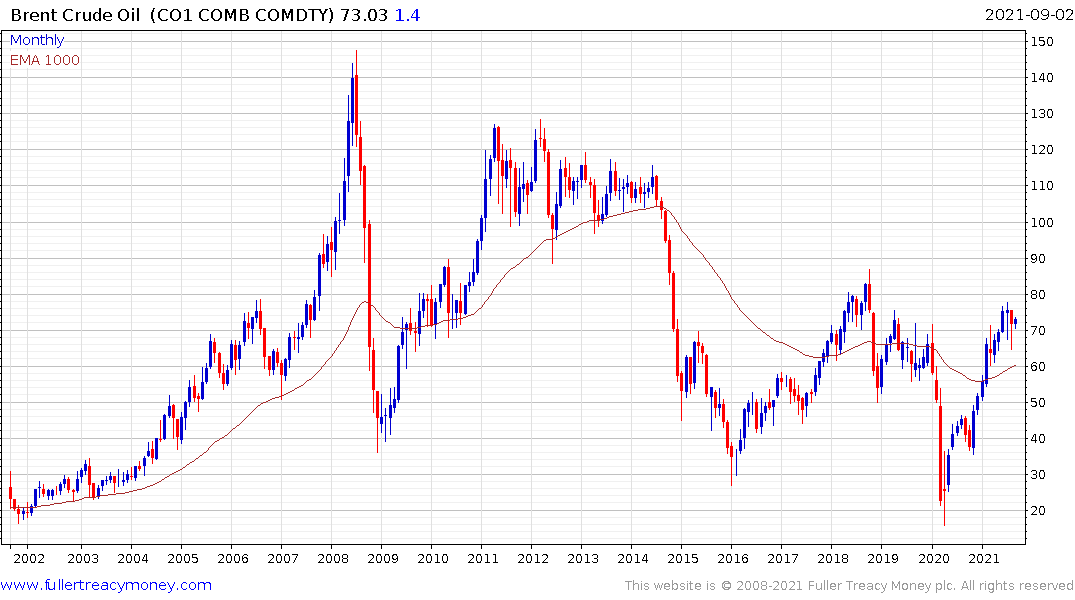

At the same time crude oil prices are in the region of the upper side of their base formation. The shale revolution in the USA successfully kept a lid on crude oil prices over the last decade as US domestic production became the marginal source of additional supply for the global market. Any threat to that condition would represent a significant headwind in terms of global inflationary pressures. There is some speculation that production in the primary shale regions is peaking. This may yet be a result of less drilling and difficulties associated with the pandemic but it is an important story to monitor.

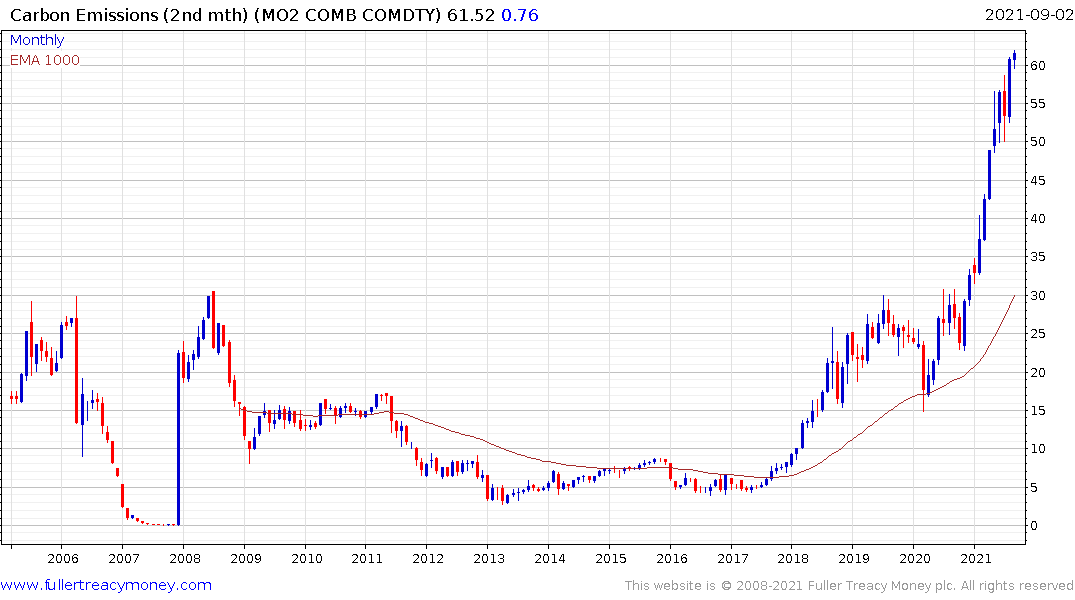

The other big difference in this cycle is the continued integration of carbon prices into the cost basis for all industries. The EU’s determination to become energy independent and to force protectionist environmental conditions on its trading partners means its politically driven carbon prices is the global benchmark. The stated ambition is to achieve a price of €100 from today’s €61.

The other big difference in this cycle is the continued integration of carbon prices into the cost basis for all industries. The EU’s determination to become energy independent and to force protectionist environmental conditions on its trading partners means its politically driven carbon prices is the global benchmark. The stated ambition is to achieve a price of €100 from today’s €61.

That represents as much of a tax on consumption as an oil bull market and is therefore a leading cause of inflationary perceptions. The simple conclusion is the persistence of inflationary pressures need to be undeniable before central banks will be forced to act. Prior to that time, they will be forced to be very cautious lest they upset the recovery.

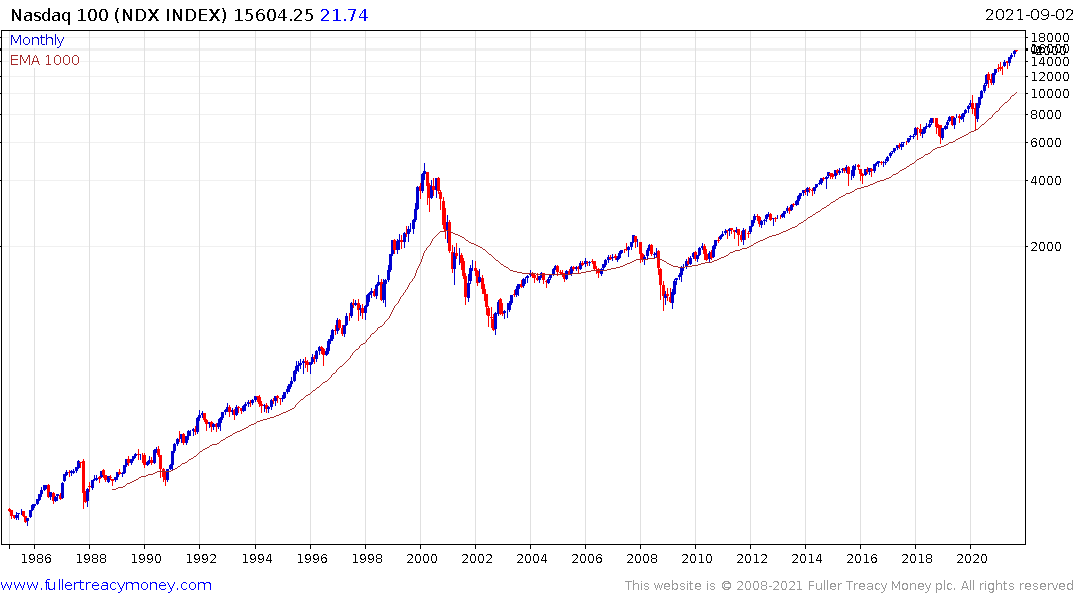

The relative performance of the FANGMAN (Facebook, Apple, Netflix, Google, Microsoft, Amazon and Nvidia) mega-caps has turned back upwards. That suggests there is room for additional upside for this bull market, despite short-term risk of another dip.

The Nasdaq-100 is now more overextended relative to the 1000-day MA than at any time since the last 1990s and shows no sign yet to peaking.

With abundant liquidity and governments spending with abandon sovereign bond yields are starting to back up. A significant deflationary event would be needed for yields to retest the 2020 lows.

That’s also starting to weigh on the Dollar again since the US is printing and spending faster than just about everywhere else.

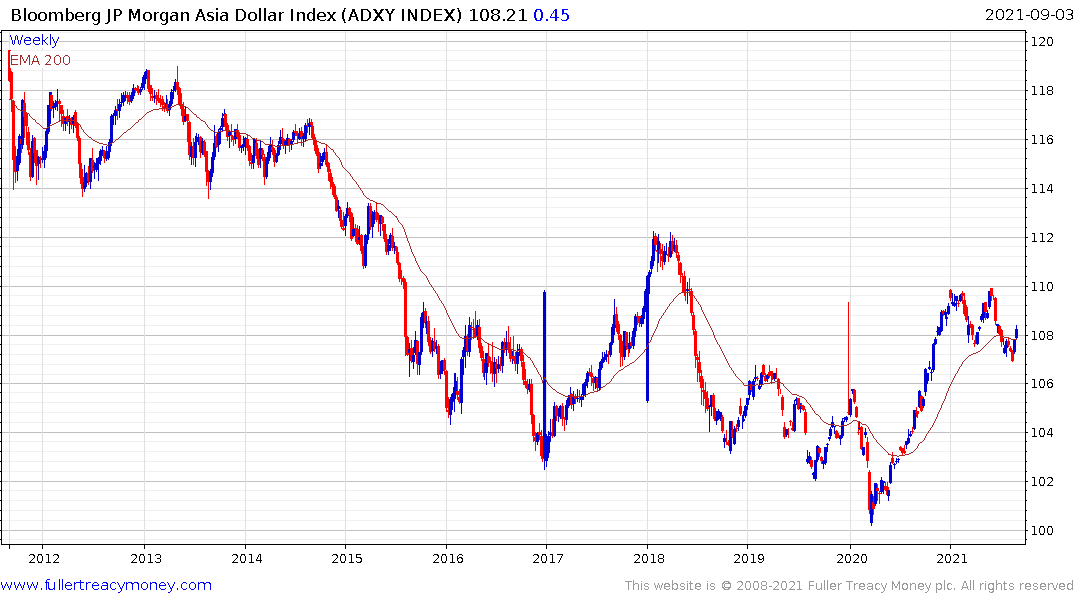

The Asia Dollar Index has perked up as a result which is helping to support regional stock markets.

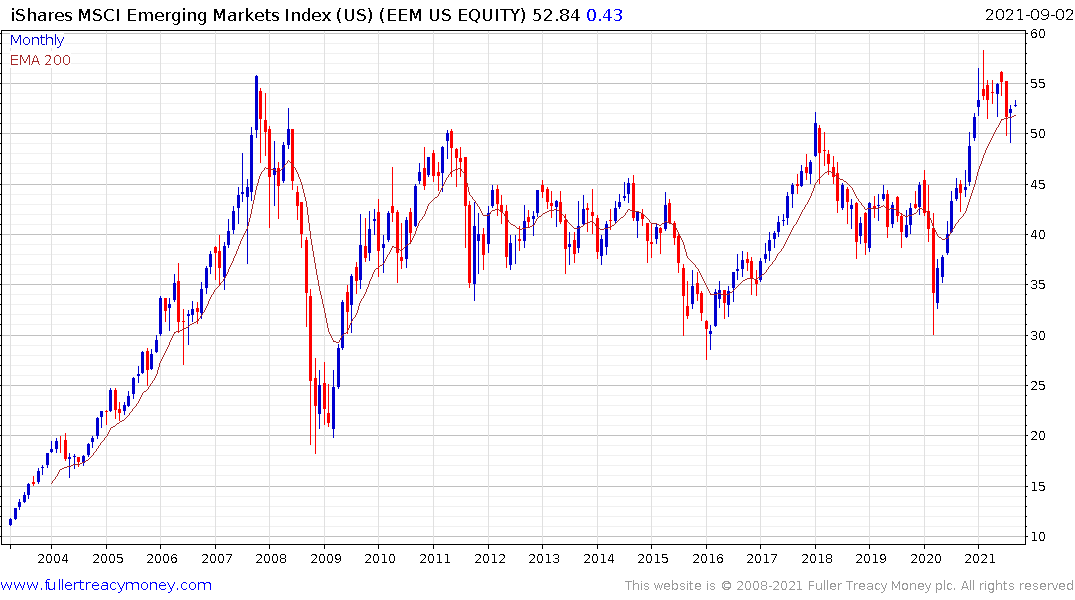

The MSCI Emerging Markets ETF has popped on the upside as some of the worried about China’s clamp down on markets have abated.

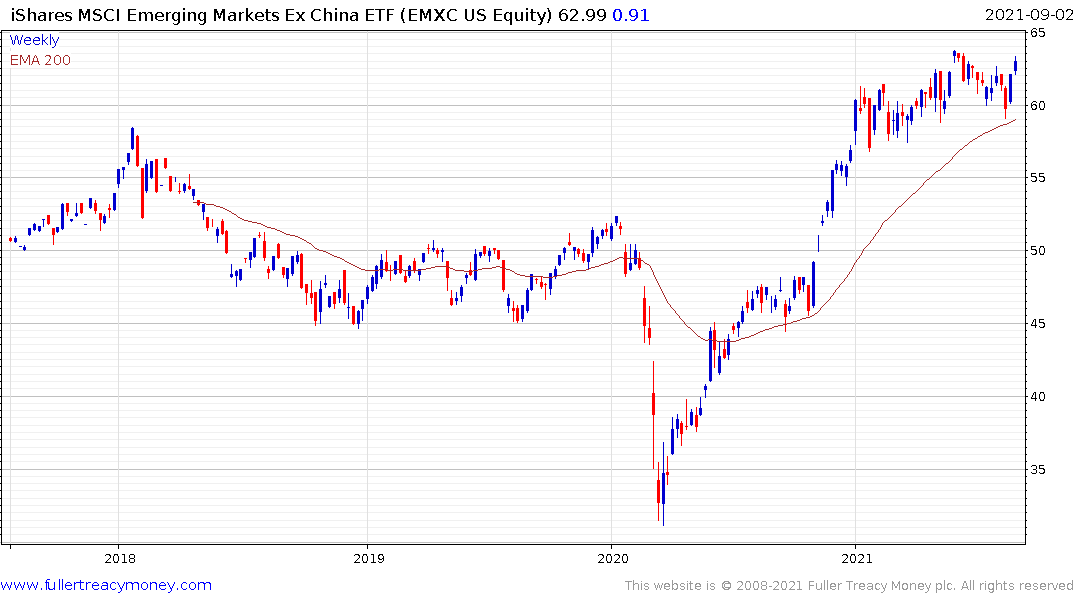

The MSCI Emerging Markets Ex-China also remains in a consistent medium-term uptrend.

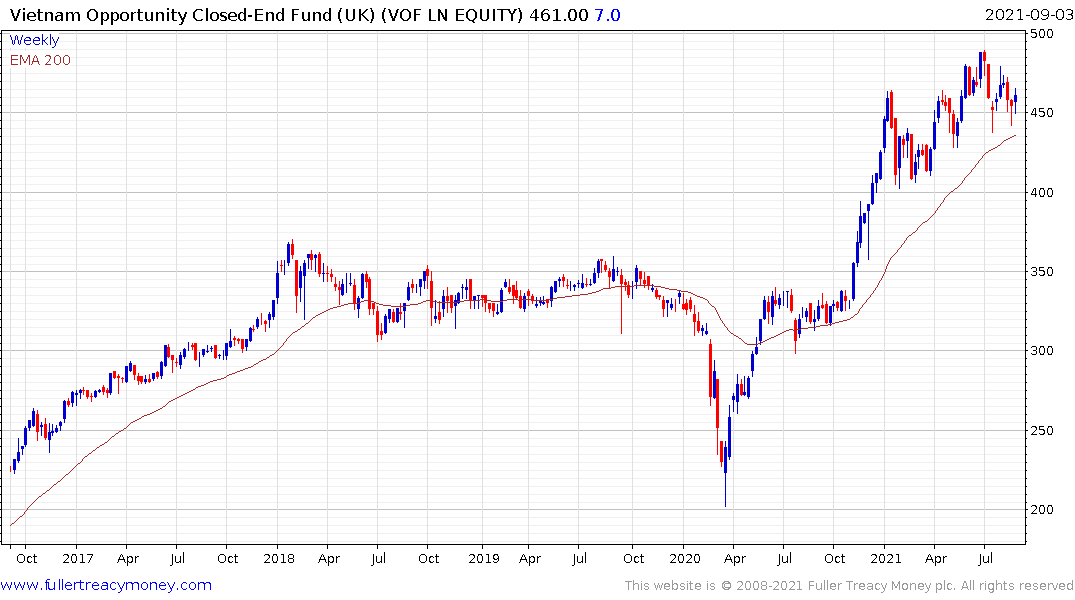

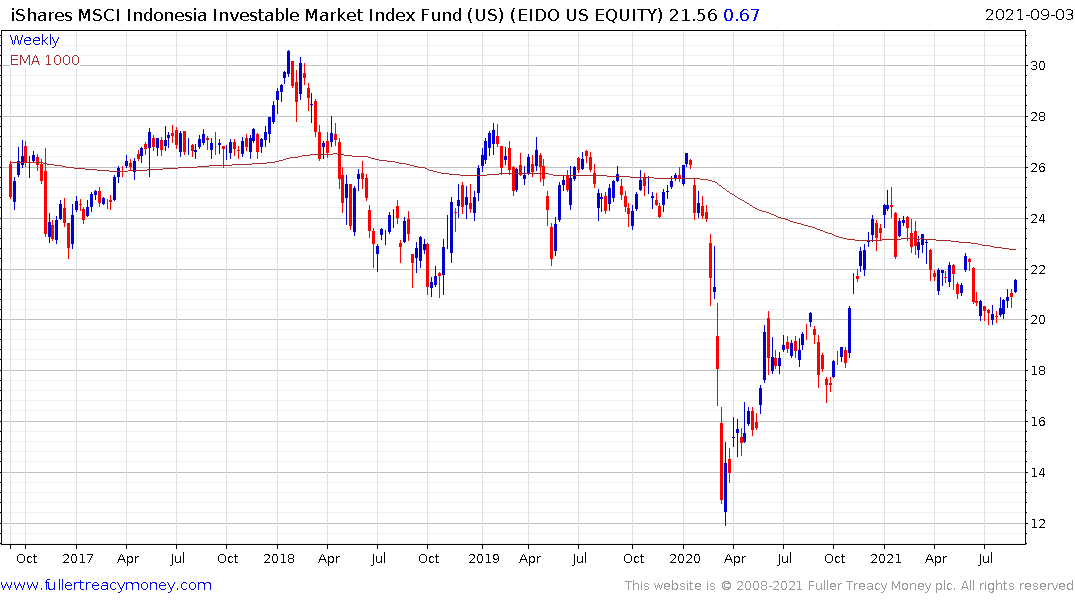

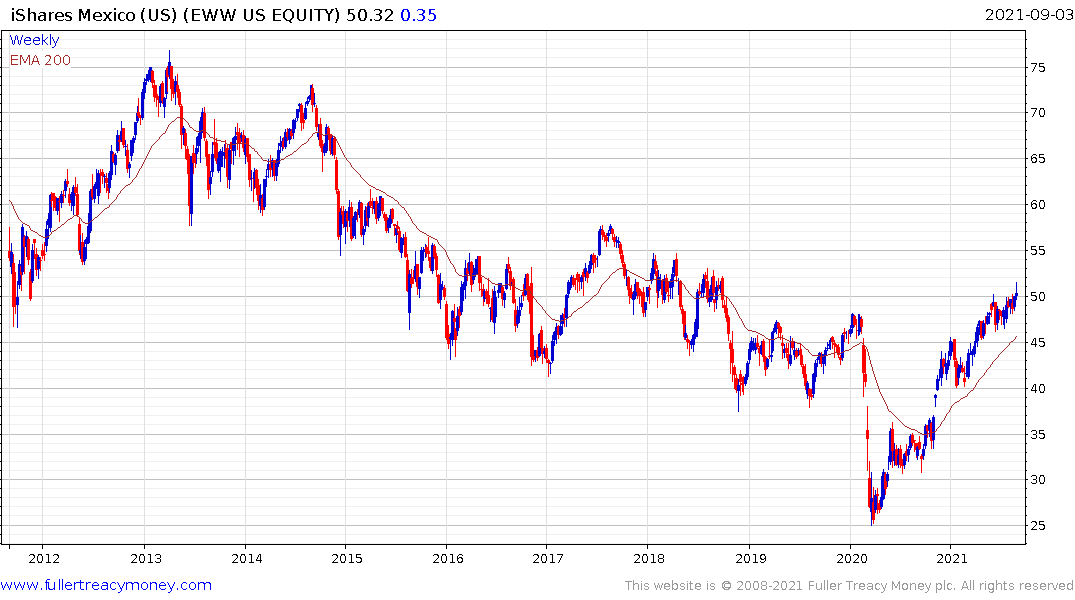

India, Vietnam, Thailand, Indonesia and Mexico remain among the biggest beneficiaries of a migration of manufacturing away from China.

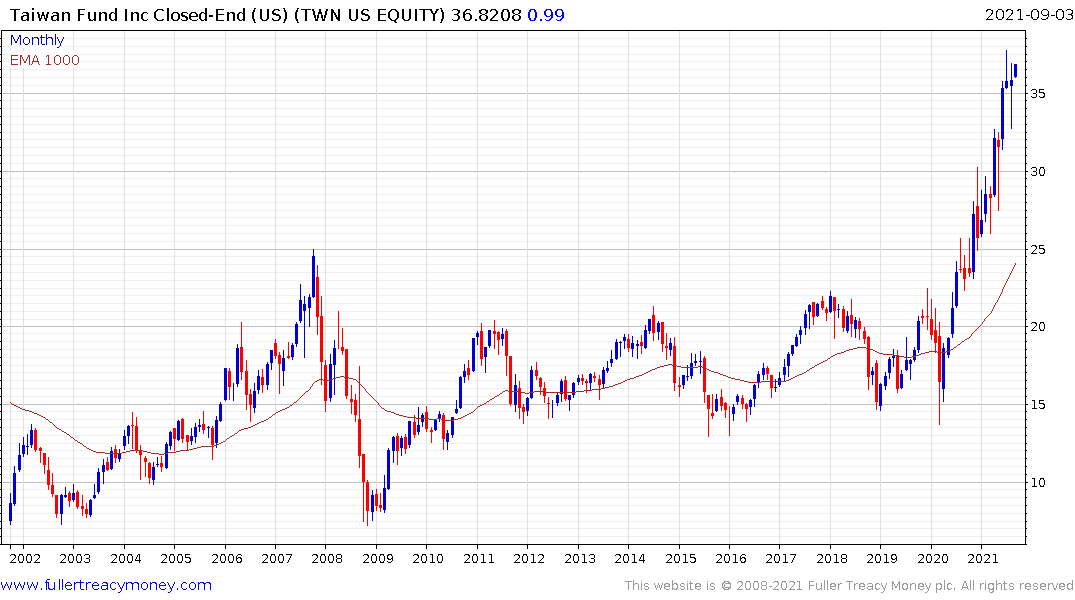

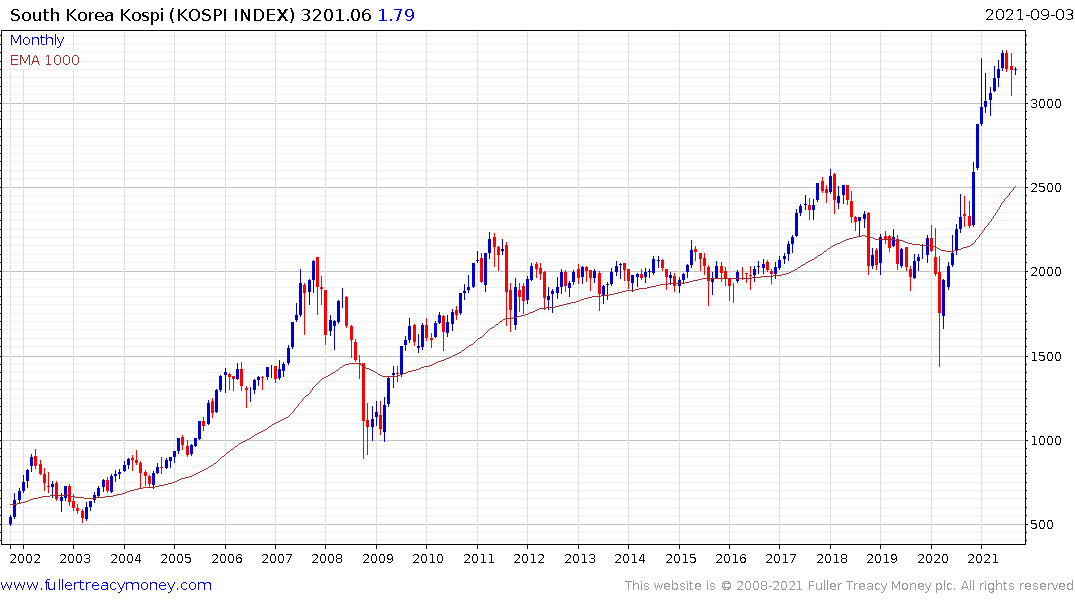

Taiwan and South Korea continue to benefit both from their regional positions but also from the speculation on tech stocks on Wall Street.

As I look around the world, there are three primary ways to approach the market environment. The first would be to ride the rising wave of speculation on Wall Street in the hope of exiting at the right time. That includes speculation in cryptocurrencies.

The significant outperformance of private equity and innovation plays is an additional iteration of this theme. The focus on innovation is based on the hope that the technological innovation cycle does not coincide with the interest rate cycle. Obviously, this is by far the riskiest in the event that central banks do eventually move to raise rates.

I view the evolving ESG bubble as part of this theme because so much of what is promised about the utopian future is as yet unproven technology. However, that is unlikely to stop the world from spending trillions to find out. The additional rationale is that most of what is deemed to be an ESG investment are tech companies.

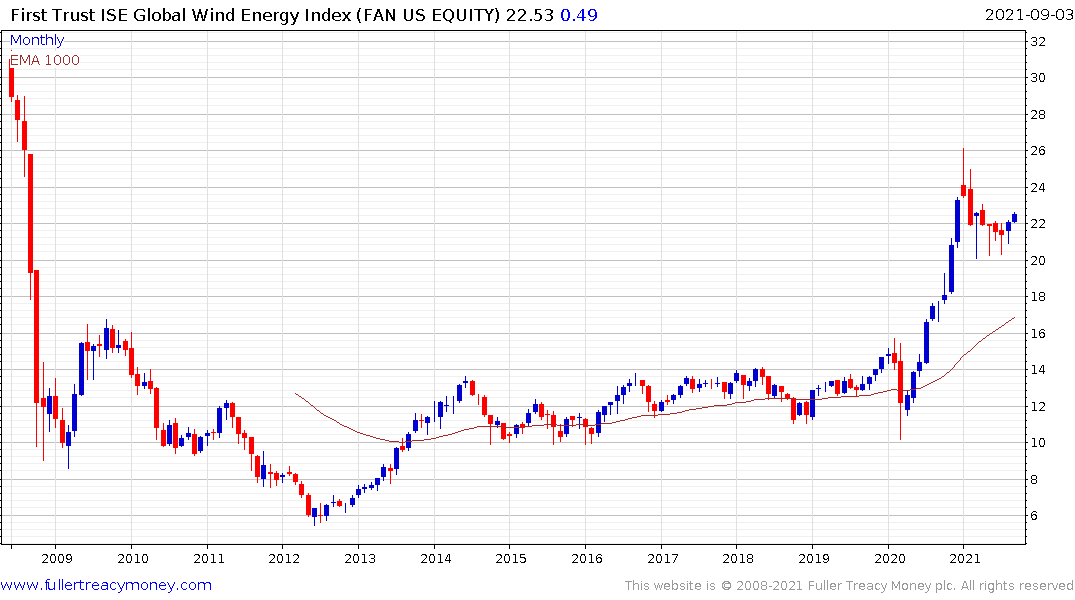

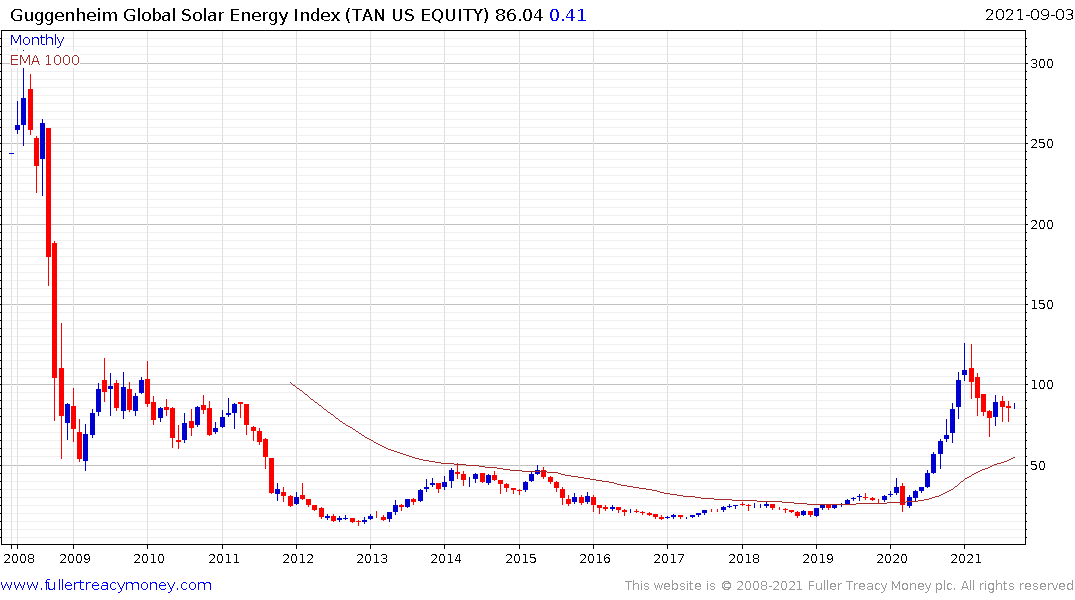

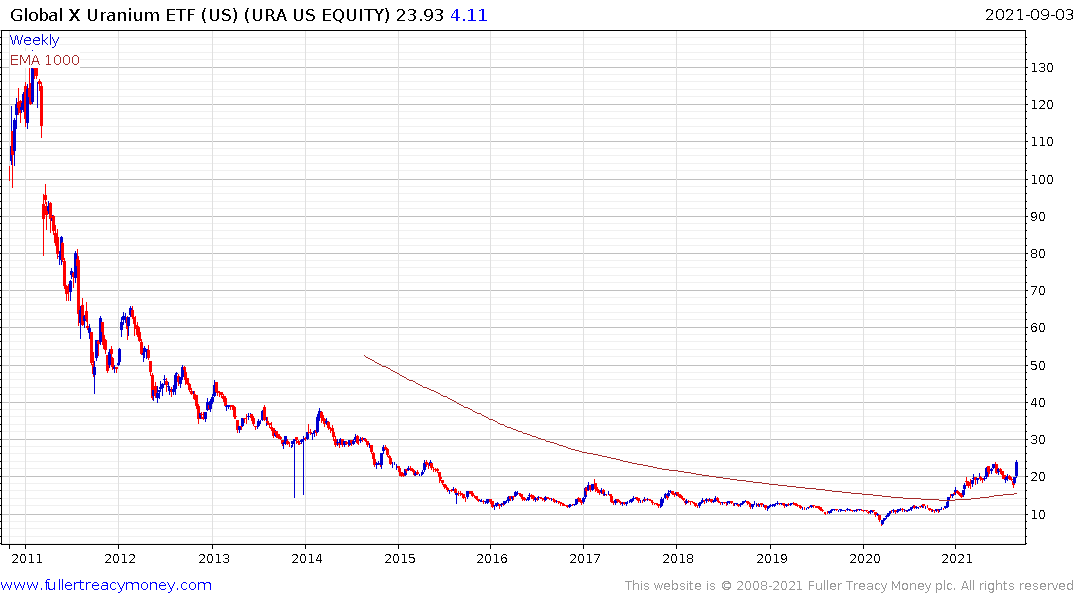

Within the energy sector the wind, solar and uranium sectors continue to rebound from their respective trend means.

The chemicals sector is also likely to be a key beneficiary of efforts to substitute oil use in the development of all manner of products.

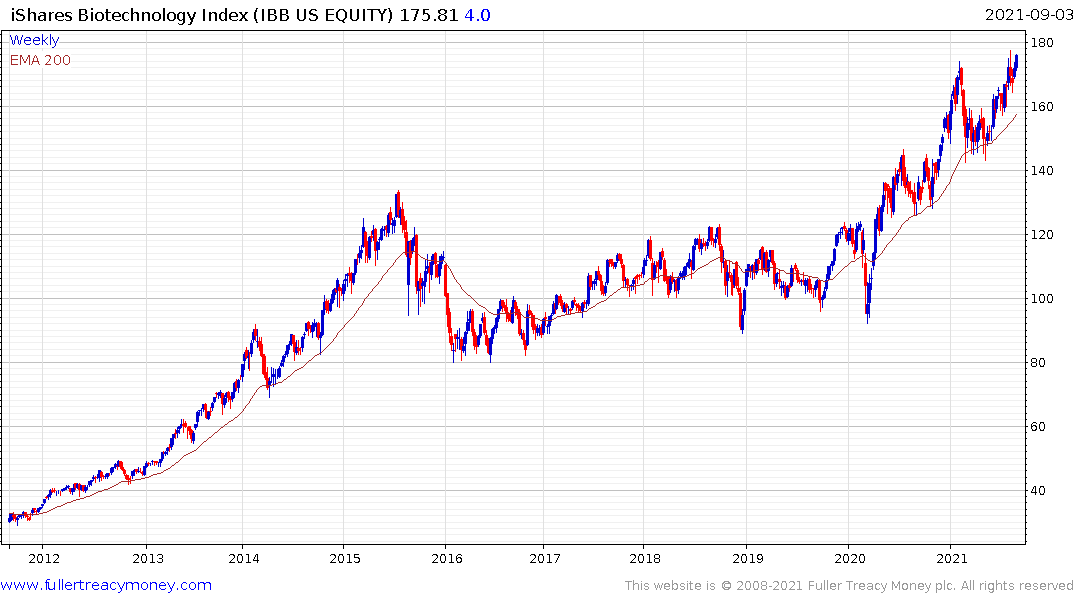

Meanwhile there continues to be significant interest in the promise of revolutionary medicine.

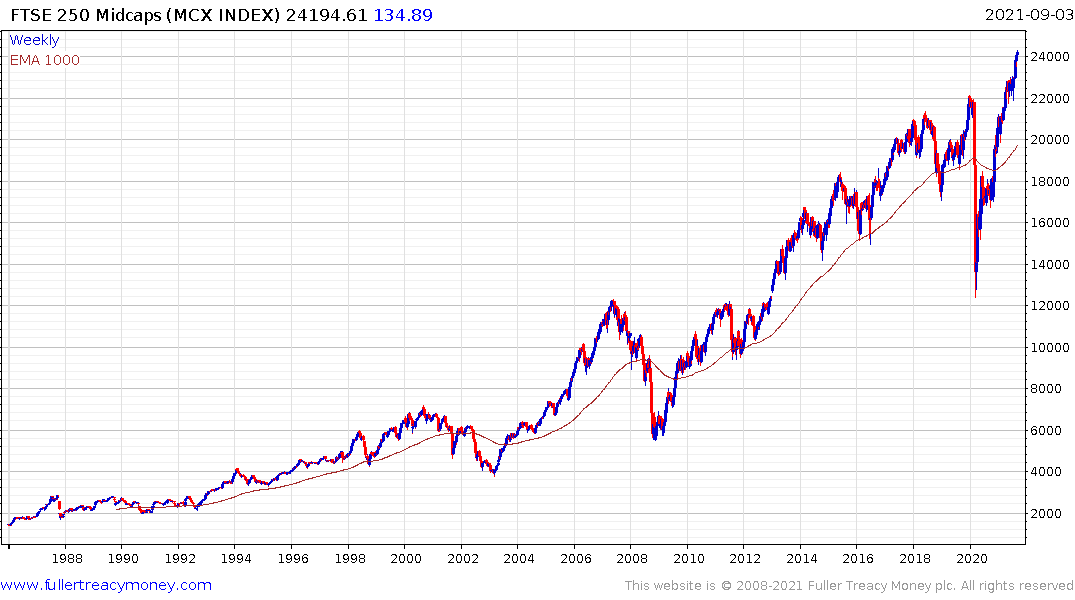

The second is to focus on value propositions among catch-up plays. That means focusing on the potential for Europe, the UK and Japan to continue to extend breakouts from very long-term base formations. The rationale here is these markets should do well from the same factors that are propelling economic growth but are trading at lower valuations. At least part of the reason these markets underperformed is because they engaged in varying degrees of fiscal austerity so they have ample scope for play catch up as they hitch themselves to the liquidity gravy train.

The third would be to hedge exposure to the first two themes by focusing on competitive devaluation of fiat currencies. Gold shares are cheap, having record margins and the capacity for rising metal prices. The VanEck Vectors Gold Miners ETF is currently firming from the upper side of its base formation.

It’s said that bull markets climb a wall of worry. There are still plenty of things investors are worried about; and not least because the visceral experience of the pandemic is still fresh in everyone’s minds. Nevertheless, global liquidity is still incredibly accommodative and is likely to remain so. That’s suggests the odds are still in favour of continued upside for the majority of assets.

Back to top