Plumbing the depths...

Thanks to a subscriber for this report from ICBC Standard Bank which may be of interest. Here is a section:

We would be biased long gold into Chinese New Year but only up to around $1,140 We expect the current rally to fade after that the metal to post a new low for the current down-cycle in Q3, followed by a sluggish recovery into year end.

Silver remains a derivative of gold. Trading opportunities are tactical and technical, not fundamental. We recommend buying silver volatility when one-month implied dips below 23%. We would rather own puts than calls.

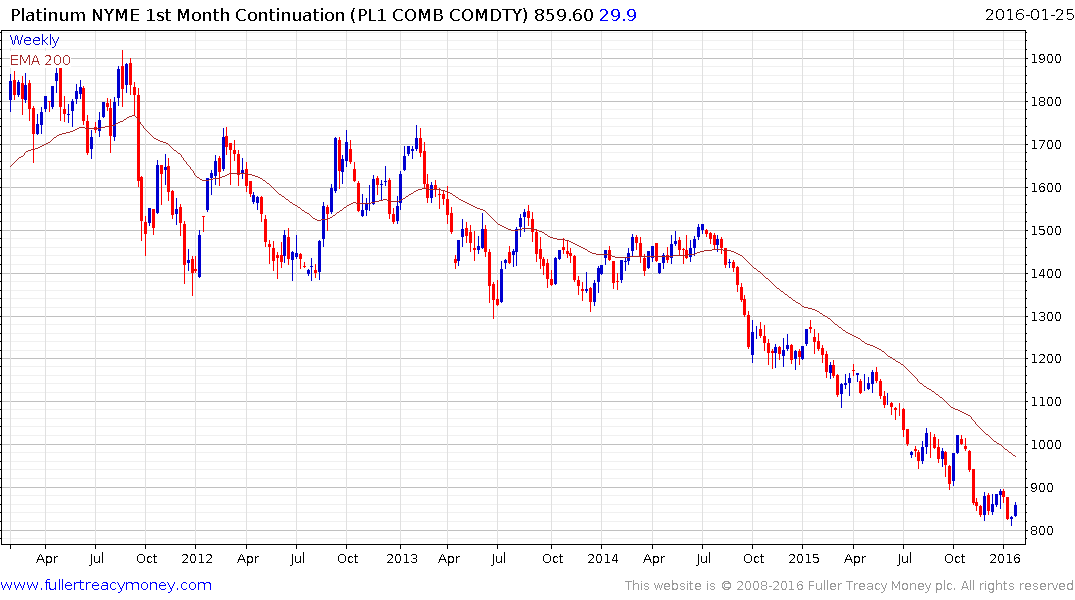

In the short-term we expect platinum to trade below $800 and potentially test the global financial crisis low of $744. The medium-term outlook is improving, however, and we think platinum’s long period of underperformance relative to both gold and palladium will begin to reverse during H2.

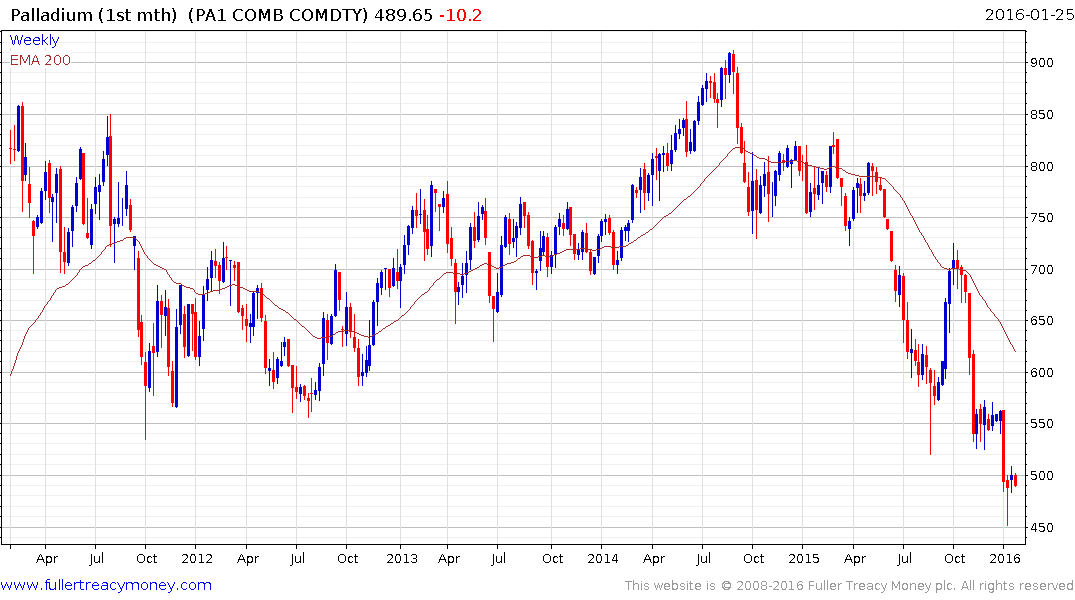

Relative to spot prices we are most bearish palladium. That’s counter to consensus and recent history. But the demand outlook has deteriorated, supply is inelastic, inventories are large, and investor conviction is shaky. Palladium is more likely to trade in the $300s than $600s this year

Here is a link to the full report.

This report is representative of a large number that have crossed our desks recently with the abiding message being that there are short-term risks but medium-term upside potential. In any other circumstances investors would pre-empt a medium-term bullish view by buying now and using further weakness as an opportunity to increase positions. One has to ask why this is not more evident within the commodity complex right now?

The most plausible answer is that investors are unconvinced by medium-term bullish forecasts following sequential years of disappointment and the negative effect oil prices exert on other commodities. Since energy is such a large component in the cost of extracting or growing just about all commodities, low energy prices allow marginal operations to persist for longer than might originally have been expected. That would suggest a low in energy pricing might be the catalyst required for bullish interest in other commodities to also return.

The statement from Saudi Aramco’s chairman today that the company can survive in a low cost environment weighed on energy prices. This article quoting Bank of America’s credit analysts comparing the crash in energy prices to the housing crash represents an additional headwind because we have not yet seen the bankruptcies predicted in the energy sector. Here is a section:

The pattern of the decline in the price of oil that began in mid-2014 is remarkably similar to the 2007-2009 pattern of the price decline of ABX, the credit derivative index that referenced subprime mortgages and, ultimately, the U.S. housing market (Chart 1). The ABX history suggests that oil will see more declines in the next couple of months and find a floor somewhere in the low 20s in the March-April time frame. Both the duration of the decline (1.5+ years) and the scale of the decline (100 neighborhood starting price down to the sub-30 neighborhood) are similar. Given that both housing and oil prices were fueled to spectacular heights in the two periods by massive credit expansion, it’s probably more than just coincidence that the respective “bubble” bursting patterns are so similar.

Platinum failed to hold the move to new lows last week and potential for a reversionary rally continues to look more likely than not. A sustained move above $1000 will be required to question the medium-term downward bias.

Palladium remains deeply oversold relative to the trend mean but it needs to hold the low near $450 if current prospects for mean reversion are to remain credible. .

Gold has almost closed its overextension relative to the trend mean but will need to sustain a move above it to confirm a return to demand dominance beyond the short term.

Silver continues to range around $14 and needs to sustain a move above the trend mean to break the medium-term progression of lower rally highs and indicate a return to medium-term demand dominance.