Musings from the Oil Patch September 8th 2015

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. Here is a section:

The Bernstein report contained a chart showing LNG terminals in existence, under construction and planned globally as of late 2011. The chart actually understates the number of LNG export terminals in the United States.

One area of concentration is Australia where huge offshore gas reserves and gas from coal fields are feeding into new LNG export terminals that when all are completed will position the country as the world’s largest gas exporter, surpassing Qatar. Virtually all of this gas has been targeting Asian markets, but with the slowing economies there and now the resumption of nuclear power plants in Japan, that may be smaller than previously anticipated. A report from consultant EY shows projected global LNG demand beginning in 2012 through 2030. While the demand from Japan and Korea was projected to grow, it rose very slowly. The more dramatic growth was projected to come from other Asian countries including China. Since this forecast, China and Russia have agreed to a deal to ship Siberian natural gas into the Chinese pipeline system reducing the need for China to buy as much LNG as originally planned

Even with the projected demand growth, the EY report shows that the planned construction of LNG export terminals globally would exceed demand beginning as early as 2015 but certainly by the end of the forecast period in 2025. At that point, all the speculative liquefaction capacity as of 2011 would be surplus for meeting the world’s gas needs.

Here is a link to the full report.

Natural gas is becoming an increasingly globally fungible commodity just like crude oil. With a more efficient global market it is reasonable to expect arbitrages to narrow. This is a significant consideration when long voyages are planned to the destination market not least when such a huge amount of capital has been invested in building export capacity in the USA and Australia. For the USA at least the opening up of the expanded Panama Canal early next year is good news. For Australia relatively close proximity to its destination markets is a positive.

On the plus side, with increased security of supply comes increased demand as natural gas meets the requirements utilities have for base load. For export facilities such as Cheniere, where activist investors are vocal on both the supply and demand sides, prices are important.

.png)

The share rocketed higher from modest beginnings in 2010. At the time it was considered speculative that the facility would ever be built because of the money involved. The signing of an agreement with BG Group to guarantee demand was the catalyst for a repricing of potential. The share rallied from $4.60 to a peak last year near above $80. As discussed at The Chart Seminar acceleration is a trend ending and the drawdown In October last year was large enough to chasten rampant demand. Prices subsequently rallied but failed to make new highs and encountered resistance in the region of the trend mean from early August. It is now extending its break lower. This is good example of a Type-1 ending with right hand extension and a clear and sustained move above $70 would be required to begin to question medium-term supply dominance.

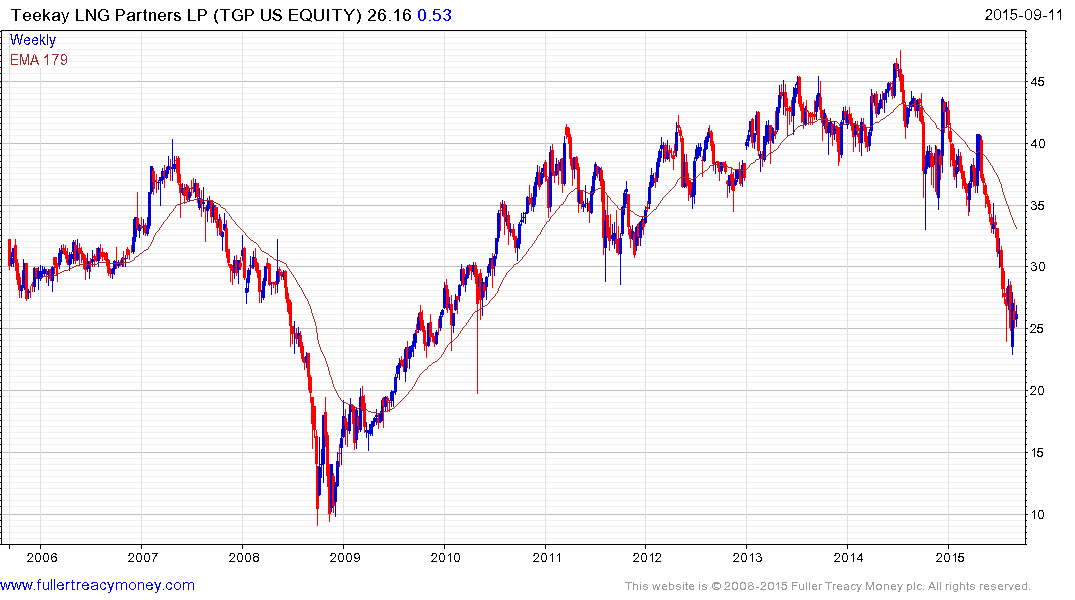

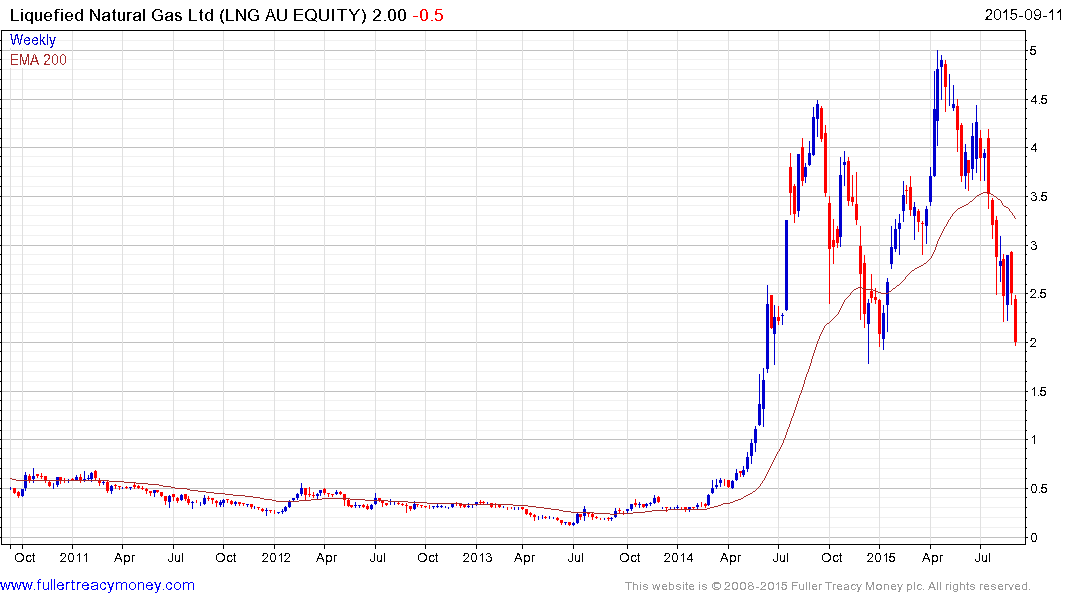

If prices are coming down then demand will eventually improve and transport for the commodity may benefit. A number for US listed companies have experienced steep declines and are in deeply oversold territory. Teekay LNG above is an example and Australian listed Liquefied Natural Gas Ltd is accelerating lower.

Belgian listed Exmar found support in the region of €8 from early this year and continues to sustain a progression of higher reaction lows. It will need to hold the €9 if potential for higher to lateral ranging is be given the benefit of the doubt.

The price action evident among LNG tanker companies suggests the near-term bearish outlook is currently outweighing what could be quite bullish medium-term factors.

Back to top