Musings from the Oil Patch August 29th 2017

Thanks to a subscriber for this edition of Allen Brook’s ever interesting report for PPHB. Here is a section on lithium and cobalt:

We don’t know the details behind the Morgan Stanley electric vehicle forecast, but we know there are both more and less aggressive forecasts. We wonder if those forecasters have considered the potential constraints from lithium carbonate supply. There is a greater issue with cobalt, which accounts for 58% of a battery by weight, more than the lithium in a battery, and consumes 42% of all cobalt output. The problem is that cobalt supplies are smaller and about 60% comes from the Democratic Republic of Congo, which is controlled by war lords and relies on child labor for mining the ore. The governments we will have to deal with to meet the demand for rare minerals to meet electric vehicle forecasts present many moral and financial question marks. In fact, when we were in Tibet earlier this summer, we followed Chinese trucks hauling bags of lithium carbonate from mines to shipping depots. That supply is likely committed to the Chinese electric vehicle industry, which needs it to meet its anticipated growth outlook.

As a result of the growing demand for lithium and other rare minerals, their prices are climbing, and in some cases at alarming rates. Since 2015, lithium prices have quadrupled, while cobalt prices have doubled. What will rising prices and limited availability mean for the forecasts of ever cheaper batteries?

Here is a link to the full report.

Forecasts for where lithium and cobalt demand is going to be in 2025 are being used to drive investment in new supply today, but it takes years to bring new supply to market. In that window between when demand increases and supply responds there is room for prices to increase meaningfully; in a rerun of the Supply Inelasticity Meets Rising Demand dynamic that animated the commodity bull market from the early 2000s.

Cobalt might best be described as a minor metal so it is challenging to find a pure play on it. The majority of cobalt is derived as a by-product of nickel mining. That sector has been a conspicuous laggard in the industrial metals complex over the last 18 months but is now beginning to show signs of life.

Nickel has been trading for more than a year in the region of the psychological $10000 and the 2008 lows. It has rallied over the last six weeks to test last year’s peak and a sustained move below $10000 would be required to question medium-term recovery potential.

UK listed Glencore rallied through 350p for the first time since 2012 last week and a clear downward dynamic would be required to check potential for additional upside.

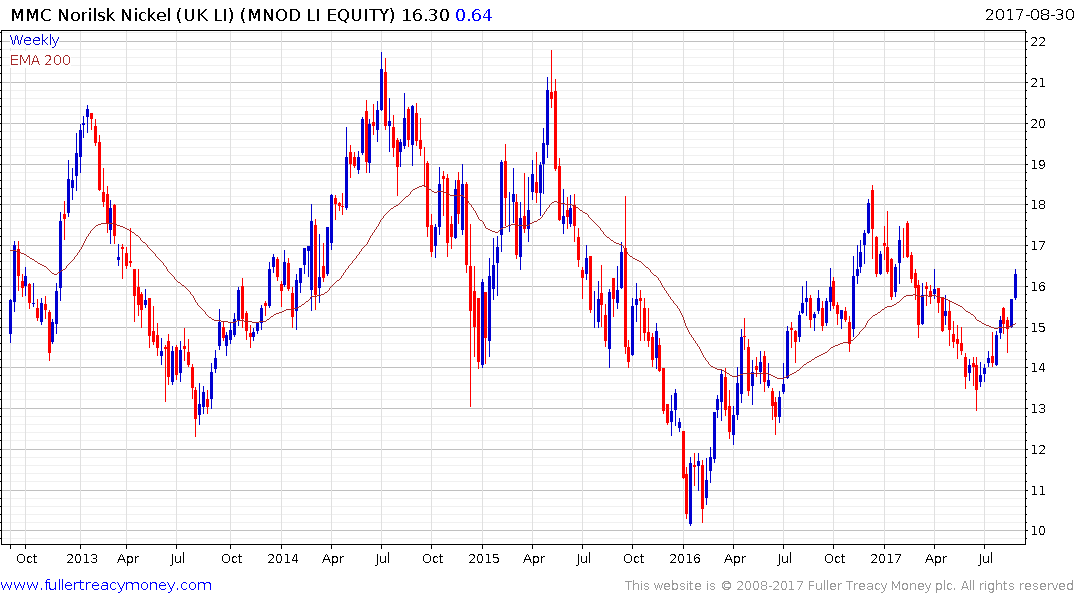

UK listed Norilsk Nickel has been ranging in a volatile manner, below $20 since 2012. It rallied over the last three weeks to break this year’s downward bias and a sustained move below $15 would be required to question potential for a further test of overhead trading.

Canadian listed Sherritt has rallied for the last seven consecutive sessions to break back above the psychological C$1 level to confirm a return to demand dominance beyond short-term steadying.