Musings from the Oil Patch August 15th 2017

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. Here is a section:

In total, between 2010 and 2040, the EIA expects energy demand to grow by 54.4%. Liquids fuels are projected to grow over this period by 37.7%, while natural gas growth will soar 78.7%. In physical terms, natural gas (93 QBtus increase) consumption will grow by nearly a third more than oil’s use (68 QBtus), while coal consumption (34 QBtus) will increase by barely over half of the growth in liquids’ consumption. Nuclear power increases the least of all the fuels (19 QBtus), but posted one of the largest percentage gains (+67.9%) due to its small base in 2010. Most interestingly, the Other category, which includes renewables, is predicted to increase consumption by 74 QBtus, or an impressive 128.5% gain.

A consideration that should not be overlooked is where this growth is happening. Exhibit 3 (next page) shows energy consumption divided between the developed countries of the world (OECD) and the developing ones (non-OPEC). The difference in energy demand growth between these two groups is astounding. The OECD economies will increase their energy use by 15.8% compared to the 87.5% growth projected for non-OECD economies. For a domestic exploration and production company, this may seem to be a worthless consideration, but now that the United States has become an oil exporter, the health of the global oil market should be of increased interest to the executives of these E&P companies.

What the EIA forecast demonstrates is that the portfolio shifts underway at several major integrated oil companies – BP, Royal Dutch Shell (RDS.A-NYSE) and TOTAL S.A. (TOTF.PA) – from crude oil to natural gas resource exploitation, are founded on the expectation that the world’s energy market has entered a new era that will be dominated by natural gas.The quest for cleaner fossil fuels, in response to global pressure to reduce carbon emissions, has focused on increased use of natural gas, which has considerably fewer carbon emissions than either crude oil or coal. That explains why natural gas was initially embraced by environmentalists as the “bridge fuel” to a cleaner energy mix until renewable fuels could mature sufficiently to become the “carbonless fuel” for the future. The double-digit price at that time may explain why the environmentalists loved natural gas as it provided a price umbrella over expensive renewables.

Here is a link to the full report.

The major oil companies have been reporting reserves on an energy equivalent basis for more than a decade which tends to paper over the transition that has been made from oil to gas production. It’s no exaggeration to state that companies like Royal Dutch Shell, Total and Exxon Mobil might better be described as major gas companies rather than major oil companies.

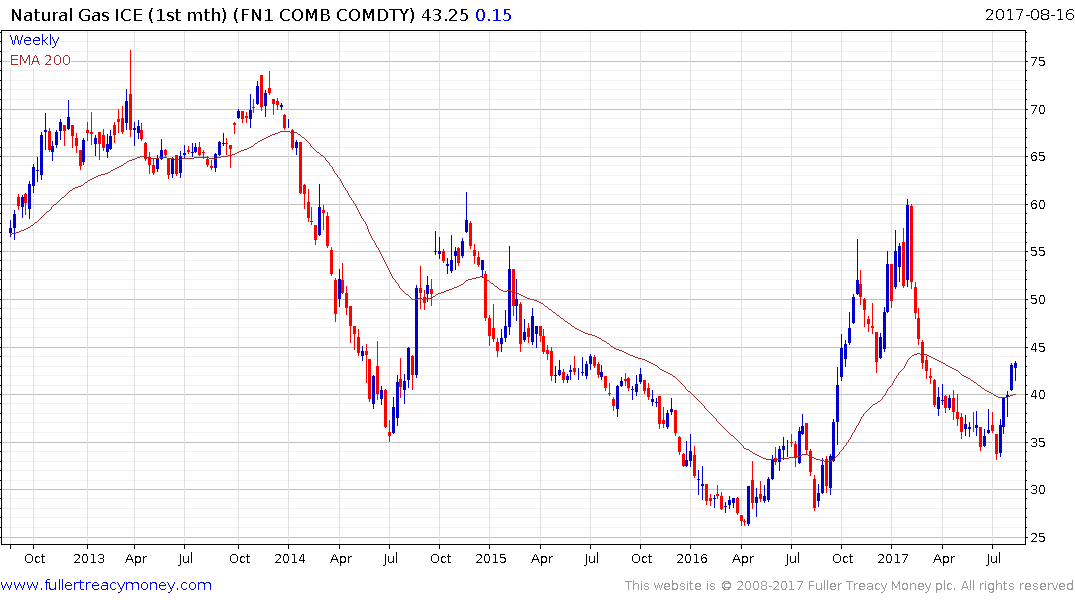

A sharp divergence has emerged between US and European gas prices which may be influencing the relative performance of the companies selling into those markets.

Henry Hub hit a medium-term peak near $4 at the beginning of the year, continues to hold a progression of lower rally highs and will need to sustain a move above $3 to signal a return to demand dominance.

UK Natural gas also pulled back sharply from early this year but has staged an impressive rally over the last month and is now trading back above the trend mean.

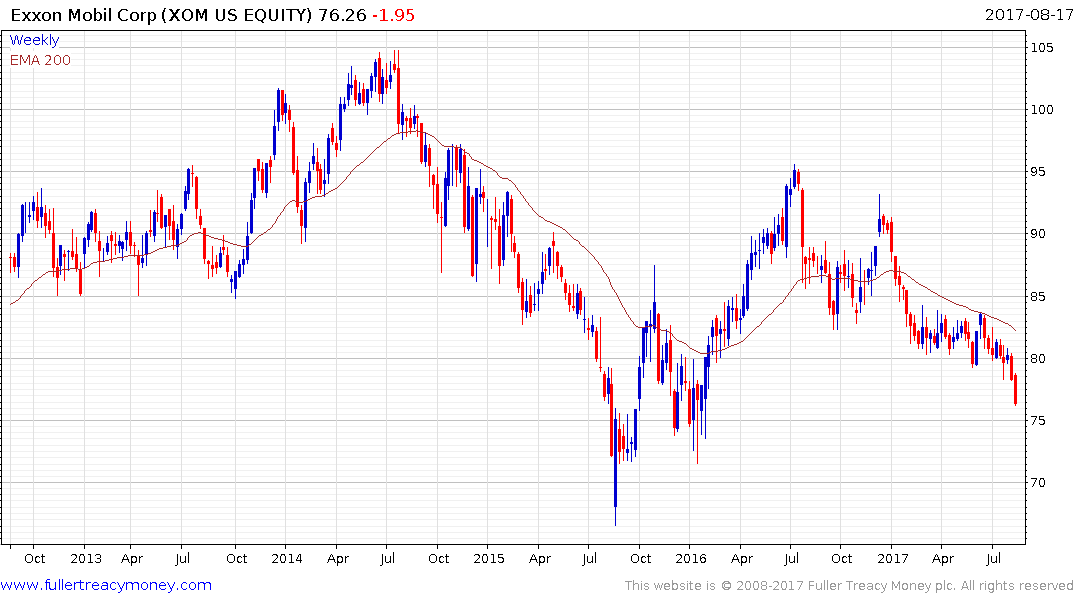

Exxon Mobil (Est P/E 22.38, DY 4.02%) has held a progression of lower rally highs since January and extended its downtrend this week. While somewhat oversold in the short-term, a clear upward dynamic will be required to check momentum beyond a pause.

Royal Dutch Shell (Est P/E 16.08, DY 6.9%) hit a medium-term peak near 2400p at the beginning of the year and has been ranging between 2000p and 2250p since February. It is currently pulling back from the upper side of that range and will need to hold the lower boundary if top formation completion is to be avoided.

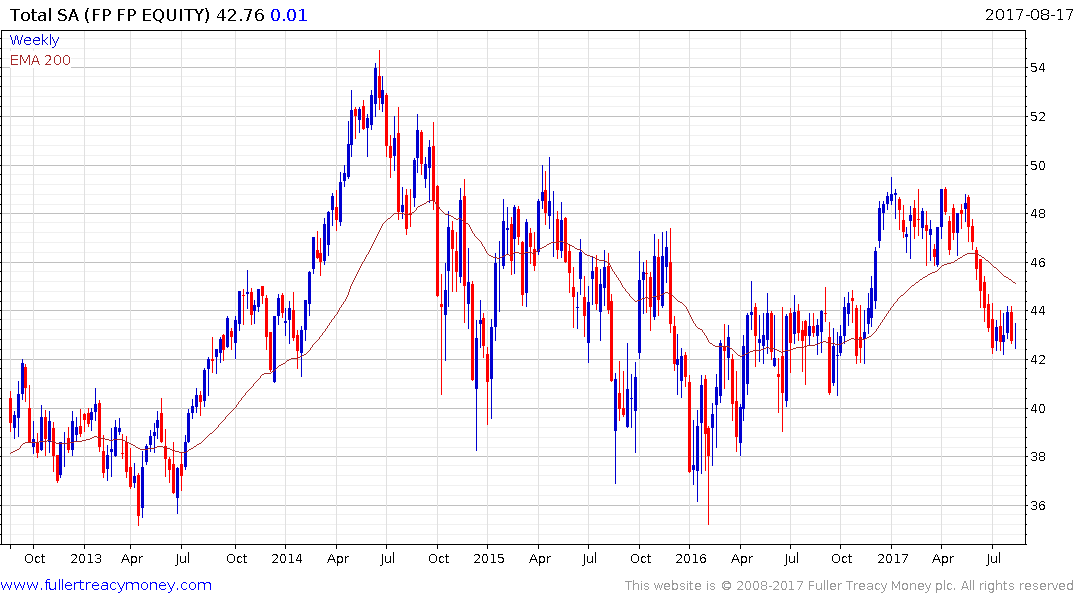

Total (Est P/E 12.64, DY 5.78%) has been subject to the same kind of volatile range as the oil price over the last couple of years and will need to sustain a move above €45 to signal a return to demand dominance.