Musings From the Oil Patch April 20th 2015

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. This edition has more of interest than usual and I commend it to subscribers. Here is a section on the surge in private equity interest in the oil sector:

We came away with several impressions from the two presentations and our discussions with fellow attendees. First, as we mentioned earlier, the vultures who circle over every disastrous industry are circling over energy with high expectations that road-kill victims will soon be available. Second, there are a lot of smart investors looking for the right opportunity to “buy into the energy industry at the bottom.” To us, that means there is too much money chasing a limited number of quality investments. That also likely means pricing on deals initially will be too high. The private equity investors believe these early investors may have to wait longer for the returns they are traditionally expecting. Fortunately, or unfortunately, the availability of public money is delaying the typical industry cycle pattern for private equity returns.

The uniformity of thinking among private equity players is a bit scary. Group-thought is usually not a successful strategy. The volume of public capital is not only surprising, but discouraging if one believes the industry needs to experience pain before a true recovery can begin. Lastly, in looking at the presenters and the audience, there were very few present that experienced the 1980’s forced re-structuring of the energy business following the bullish experience of the 1970’s. In our discussions that day, we encountered another old-timer who referenced the 1980’s downturn starting in 1982, three years before when most who look at the industry’s history think it began. We were there then, and this guy had it exactly right. This industry is headed for significant change.

Here is a link to the full report.

One of the problems faced by fundamental or value investors at a time when interest rates are low, liquidity abundant and valuations elevated is that there is a dearth of opportunities. When a decline such as we have seen in the energy sector occurs, they have little choice but to deploy capital because there are so few other low prices opportunities. This at least partially explains the ease with which private equity firms have been able to raise capital. The problem is that with so much money chasing opportunities prices will rise for troubled assets and the eventual rationalisation of the sector will be delayed.

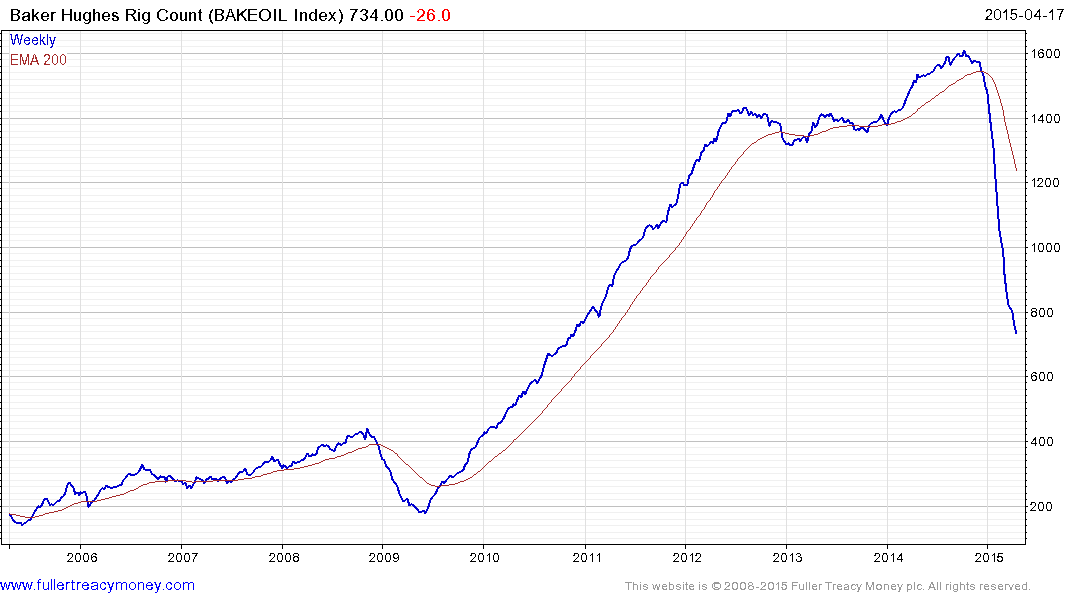

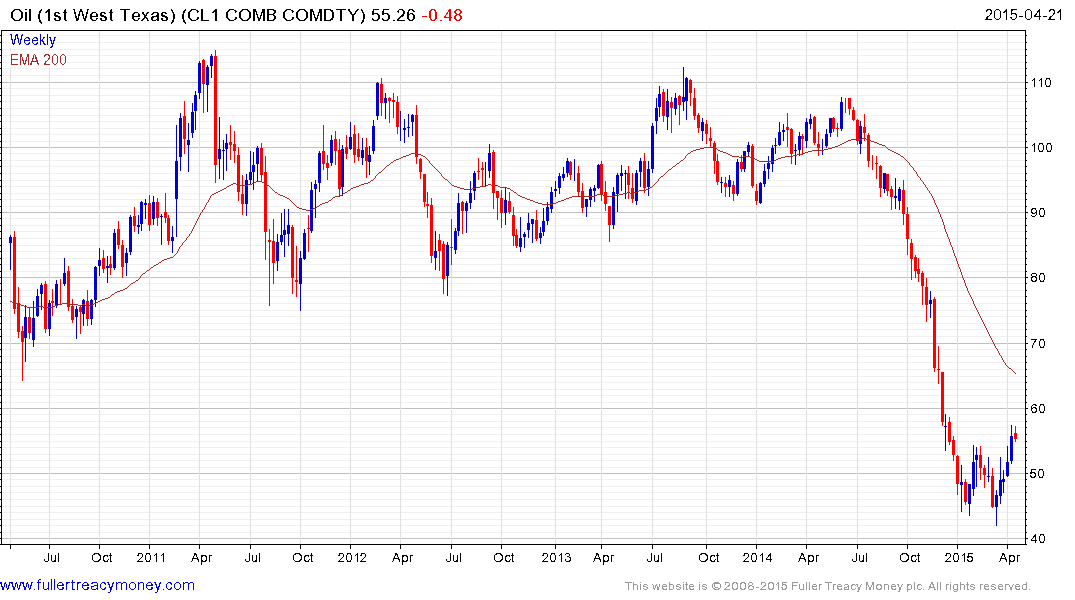

The Baker Hughes Rig Count continues to represent a tailwind to prices but when it eventually turns upwards it is likely to signal that any supply cut will soon be reversed. This could then act to inhibit the capacity of oil prices to continue to bounce. As I have mentioned before, and as Allen Brooks highlights in the above report, natural gas’s inability to sustain a rally since the evolution of unconventional supply represents a potential outcome for oil prices. As a result the price at which the rig count turns upwards is likely to be important from the perspective of monitoring the oil price and its trading environment over the medium term.

Back to top