Musings From the Oil Patch April 18th 2017

Thanks to a subscriber for this edition of Allen Brooks’ ever interesting report for PPHB. Here is a section:

The worst downturn in the history of the oil industry has been followed by the fastest drilling rig recovery in history. From massive layoffs and corporate restructurings, oil and gas and along with oilfield service companies have had to switch gears and figure out how quickly and profitably they can grow along with the current recovery. As someone mentioned, the industry has crammed a year’s worth of rig activity growth into a few months – something that is creating a challenge for the oilfield industry.

As the energy companies are about to start reporting financial results for the January - March 2017 period, numerous oilfield service company managements have already signaled that the numbers will likely not reflect the levels of profitability Wall Street analysts had expected due to the costs of responding to the explosion in activity, especially following OPEC’s surprise output cut to help drive a recovery in oil prices. From the rapid climb in the rig count, it is clear that not only had investors and analysts bought into the recovery scenario, but so too had exploration and production (E&P) company managements.

There is an expression in English literature that “all things come to those who wait,” but that isn’t the case in the oil patch – especially if one wants to make money. In reality, the expression “the early bird gets the worm” is more appropriate to describe how people in the E&P business operate, but it is taking a toll on the pace of the recovery in oilfield service company profits. Service company managers have had to spend money to reactivate equipment and re-crew them before they can actually earn revenue. The more aggressive a company has been, or is, in ramping up its idle equipment, the greater are the costs incurred. At the present time, everyone is comfortable in the belief that the delay in gratification – increased profits – will be worth the effort, and the wait. Whether that proves a correct assumption or not will depend on how the recovery continues unfolding and what happens to well costs, which is what is driving the increased activity. Everyone has to make money going forward for the recovery to be sustained. That doesn’t mean, however, that everyone will enjoy the levels of profitability experienced during the era of $100+ a barrel oil prices. But, unless people make money, the industry will not be able to support additional activity, or possibly even support the current level of work. So where are we in this recovery?

Here is a link to the full report.

Unconventional oil and gas wells are more expensive to drill and have prolific early supply surges which peak quickly. That means operators are uniquely positioned to respond to lower prices by cutting back on drilling and to higher prices by stepping up drilling. It might not be great news for worker job security but it means the USA is increasingly the swing producer in the global oil market.

West Texas Intermediate crude oil rallied impressively to test the recovery highs below $55 but pulled back sharply last week and a clear upward dynamic will be required to confirm support, and the progression of higher reaction lows, near $47.

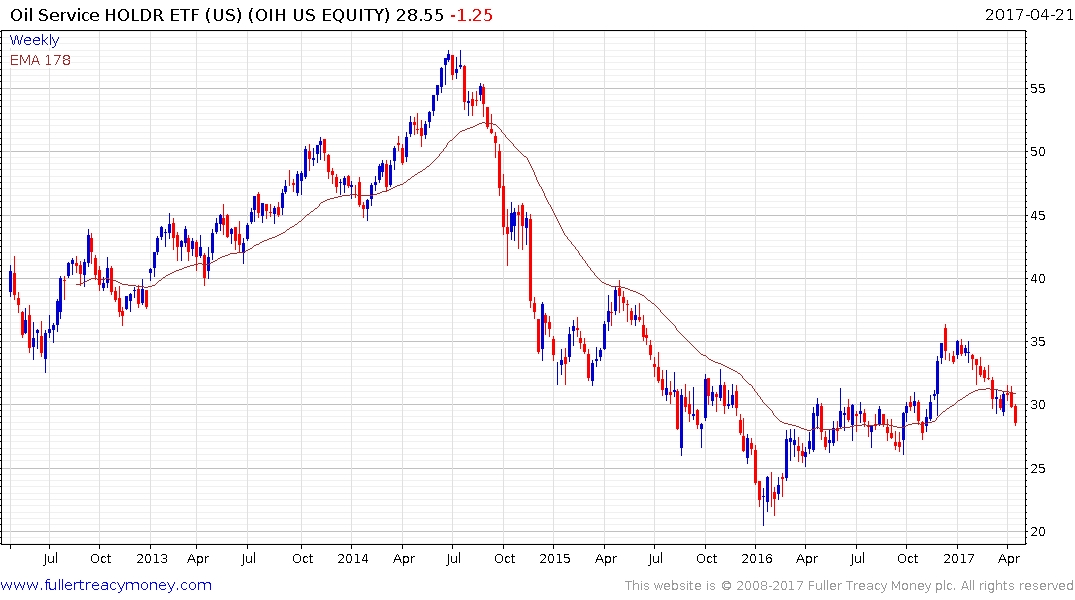

The VanEck Vectors Oil Services ETF has failed to sustain December’s breakout to new recovery highs and is now trading back below the psychological $30 area. A clear upward dynamic and sustained move back above the trend mean will be required to signal a return to demand dominance.