Lithium | 2021 supercharge?

Thanks to a subscriber for this report from Canaccord Genuity. Here is a section:

We estimate 2020 supply lifted 11% YoY to 340kt, noting lower capacity utilisation as largely a function of bottom-of-the-cycle pricing through 2020. We anticipate that a majority of the ~460kt of cumulative potential capacity that was delayed/deferred over the last ~18 months could remain suspended pending a recovery in pricing to higher levels. Recent consolidation among concentrate operations (i.e. Altura>Pilbara, Wodgina>Albemarle) now sees control of large scale, marginal cost production lies with a small number of established producers who, in our view, lack incentive to switch on large volumes of new supply.

We further note that long lead times to delivering new capacity means that the +US $4.4bn in new equity raised by lithium companies since the start of 2020 is unlikely to lead to a meaningful supply response until the mid-2020s, by which point we expect the market to move into deficit. Our revised market balance forecasts now call for more modest market surpluses (5-7% over 2021-23), with our higher rates of demand growth now expected to outpace supply growth out to 2025. Beyond 2025, we continue to forecast significant market deficits, noting a ~7x increase in supply (i.e. ~240ktpa average increase in capacity) is required to meet our 2030 demand forecast.

Here is a link to the full report.

Supply Inelasticity Meets Rising Demand is the foundation of commodity bull markets. Lithium has been through one big boom and bust cycle already and perhaps the major producers have learned their lesson. The initial mining investment boom occurred almost a decade ago. That resulted in a lot of new supply hitting the market which depressed prices. It has taken significant growth in demand for electric vehicles to soak up that surfeit.

Today, there is a lot of money flowing into additional new lithium projects so we can look out a few years to when that supply hits the market. Between now and then there is scope for the miners to continue to do well.

In the short-term, we have seen explosive breakouts from well-defined bases. Shares like Baconora, Orocobre or Livent are now experiencing some consolidation of those gains. Sustained moves below their respective trend mean would be required to question medium-term scope for continued upside.

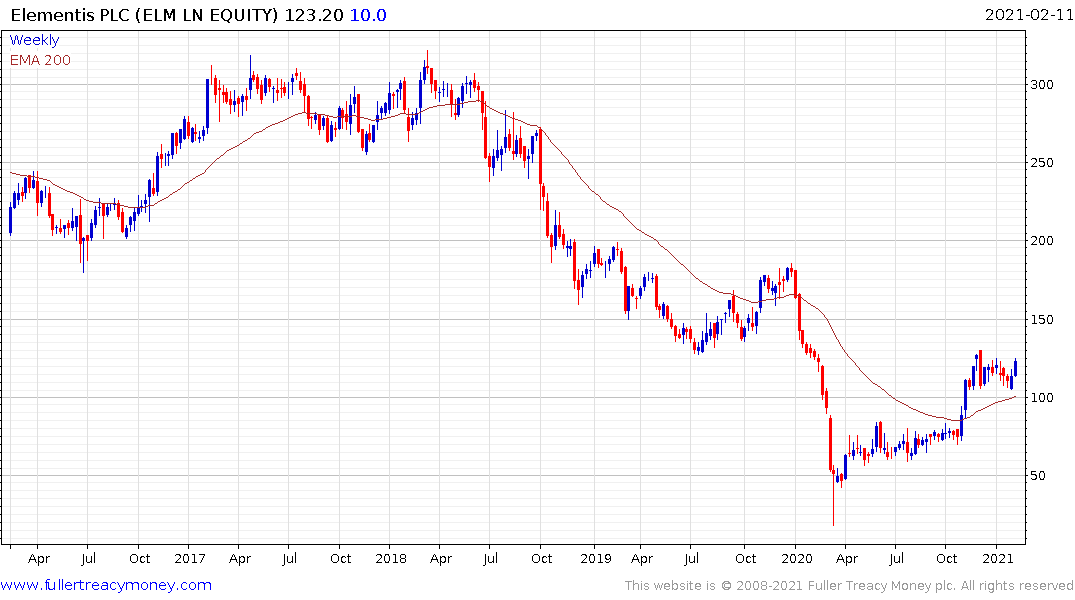

Elementis caught my attention while clicking through the constituents of the lithium miners’ section of the Chart Library. The company produces rheology sealants, surfactants for the cosmetics and energy sectors, and chromium. The primary mined materials are bentonite and hectorite.

While hectorite is a by-product of lithium mining at some projects, most notably Lithium America’s planned Thaler Pass mine in Nevada, there is no evidence that Elementis is a producer. I am moving the share to the oil services section because it is trading more in line with the potential outlook for renewed interest in shale drilling as oil prices recover.