Greed & Fear Negative SPX, Sees $130-$150 Oil Price

Thanks to a subscriber for this note summarizing the recent Raymond James Conference presentation by Christopher Wood. Here it is in full:

A few key takeaways (ask for replay)

a) has been negative USA , SPX P/S still very expensive at 2.5x, US M2 has risen by 40% in absolute terms since March 2020 (annualised rate of 15%), has slowed to an annualised rate of just 0.6% in the six months to July.

b) USA CPI ex-energy has been flat, while headline CPI down (due to oil price)

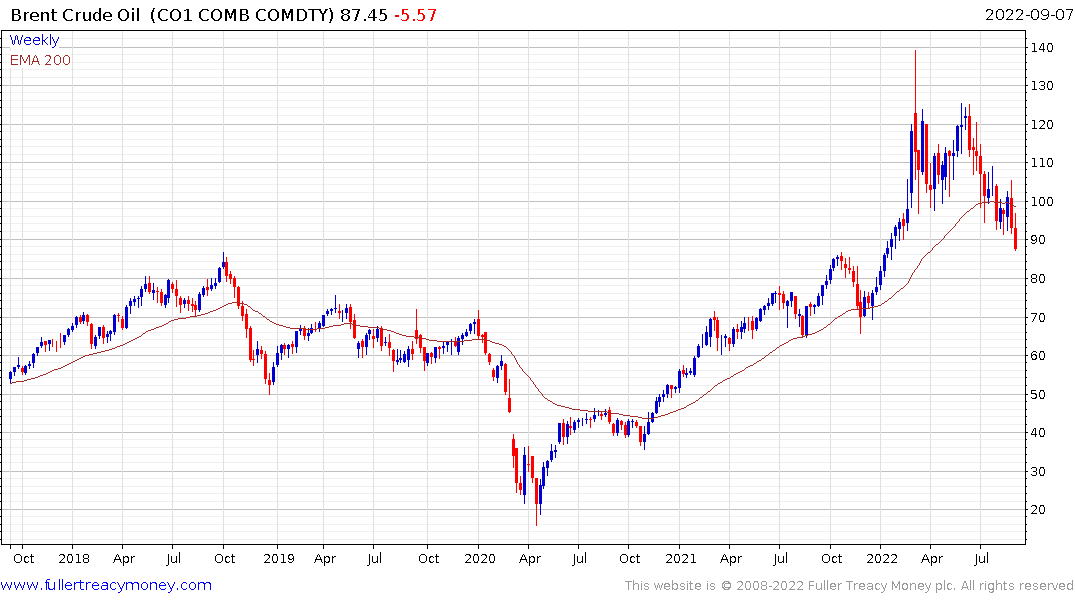

c) we see OIL price rising back to $130-$150, which would mean inflation expectations would rise too (0.80 correlation)

d) fossil fuel still 82% of global energy consumption

e) reminder EM equities vs US dollar index : 0.72 negative correlation

f) Indonesia has been our favorite market this year, credit growth rising

g) China property market woes outweigh infrastructure stimulus

i) we are neutral China

j) if YEN breaks 150 and we see 3% inflation in Japan, then base case is focus will be put on defending further Yen weakness

k) YEN is cheapest since 1971

l) India remains our favorite market on a 10 year view , we are heavy financials & property in India, housing affordability good

m) very underweight Australia (though + energy). Negative Australia housing as interest rates rising, home price declines accelerating

There is a lot of discussion in the media about the outlook for rates, the war in Europe and the region’s energy crisis, the new UK administration, and the lockdowns in China ahead of the Party Congress. For me the one thing that was front of mind this morning was it is easier to make money on the short side than by going long. That tells us a lot about the wider environment.

Europe’s economy is hurting. The UK is introducing price controls for energy but is ruling out windfall taxes for now. European countries are going the same and have no qualms about taxing fat balance sheets. With Russia shutting down natural gas supply, Europe is going to be short of gas this winter. The interests of consumers will be prioritized over industry. That implies the bill for unemployment insurance will jump as major industrial centres go on short time.

I just don’t see how the demand driver for $150 oil will arrive. Brent crude is breaking lower. US natural gas is also continuing to pull back from $10. Natural gas is a more global market because of LNG shipping, China is even exporting excess Russian supply to Europe to avail of the arbitrage. The global market is not fully fungible yet. However, it will be by the end of the decade because of the necessity to provide for the potential for ongoing supply disruptions.

I just don’t see how the demand driver for $150 oil will arrive. Brent crude is breaking lower. US natural gas is also continuing to pull back from $10. Natural gas is a more global market because of LNG shipping, China is even exporting excess Russian supply to Europe to avail of the arbitrage. The global market is not fully fungible yet. However, it will be by the end of the decade because of the necessity to provide for the potential for ongoing supply disruptions.

Crude oil on the other hand is mostly globally fungible, even if the primary contracts are for low sulphur content varieties. Russia does not have the same flexibility of oil supply as it does with gas. It can’t stop pumping from wells in the permafrost because they can’t easily be restarted. Slowing demand in a major economic centre like Europe is negative for oil.

Centrica, which owns British Gas, will be a beneficiary both of the efforts to provide bridge loans to affected energy providers as well as fiscal transfers from the government to ensure lower consumer facing prices. The dividend is at risk since it would be unseemly to pay investors while also suckling on the public weal but the company has scope to return to the black in this scenario. The share continues to rebound from the region of the trend mean.

Centrica, which owns British Gas, will be a beneficiary both of the efforts to provide bridge loans to affected energy providers as well as fiscal transfers from the government to ensure lower consumer facing prices. The dividend is at risk since it would be unseemly to pay investors while also suckling on the public weal but the company has scope to return to the black in this scenario. The share continues to rebound from the region of the trend mean.

The Yen is accelerating lower and rapidly approaching the psychological 150 area. That level coincides with major lows for the yen over the last 30 years. This is a potential area of support but would require significant Dollar weakness to suggest more than a pause.

The big issue for Japan is the 30-year yield is trending higher in a consistent manner while the 10-year is artificially supported. That’s an expensive proposition.

The big issue for Japan is the 30-year yield is trending higher in a consistent manner while the 10-year is artificially supported. That’s an expensive proposition.

Historically, Japan has relied on its robust trade surplus to fund this kind of program but that has been much less reliable over the last decade. Energy is the primary contributor to the current trade deficit so it is reasonable to argue the Yen will have difficulty rallying while energy prices are high. Since oil is rolling over that could be a support for the yen.