Fracklog in the Biggest U.S. Oil Field May All But Disappear

This article by Ryan Collins and Meenal Vamburkar for Bloomberg may be of interest to subscribers. Here is a section:

Crude in the $40- to $50-a-barrel range may wipe out most of the fracklog in Texas’s Permian Basin and as much as 70 percent of the inventory in its Eagle Ford play by the end of 2017, according to Bloomberg Intelligence analyst Andrew Cosgrove. While bringing them online is the cheapest way of taking advantage of higher prices, the wave of new supply also threatens to kill the fragile recovery that oil and gas markets have seen so far this year.

“We think that by the end of the third quarter, beginning of the fourth quarter, the bullish catalyst of falling U.S. production will be all but gone,” Cosgrove said in an interview Thursday. “You’ll start to see U.S. production flat lining.”

Drillers that expanded operations in U.S. shale fields found that sidelining wells was the easiest way to cut costs when oil and gas prices plunged. Since then, these wells have been “just sitting around, basically waiting for a better price to come along,” said Het Shah, an analyst at Bloomberg New Energy Finance.

U.S. oil producers extended the biggest shale drilling revival since last summer as rigs targeting oil and gas in the U.S. rose by 7 to 447 last week, according to Baker Hughes Inc. Dave Lesar, chief executive officer of Halliburton Co., the world’s largest provider of hydraulic-fracturing work, said Wednesday that the market in North America has turned and that he expects a “modest uptick” in drilling in the second half of the year.

Unconventional wells are much more expensive than conventional wells but come with some interesting advantages that protect producers from volatility. They have very prolific early production rates which helps to quickly pay off the multi-million dollar cost of setting them up. They then enter a period of time when production falls precipitously. If prices are not high enough to invest in boosting production through fresh drilling then it drillers have the luxury of time as they wait for prices to recover, after all the oil isn’t going anywhere.

An additional aspect I have seen very little commentary on is “refracking”. This is the practice of going back to previously drilled wells and sending additional explosives done the pipe and fracking a different portion of the bore hold. This reinvigorates production at a fraction of the initial set up cost. Companies have been slow to explore this option because it is not yet fully understood what long-term effect it has on respective basins and every effort is being made to ensure these are long-life reserves. Nevertheless it would appear only a matter of time before refracking becomes commonplace which would take the margin cost of producing US onshore oil below where it stands today.

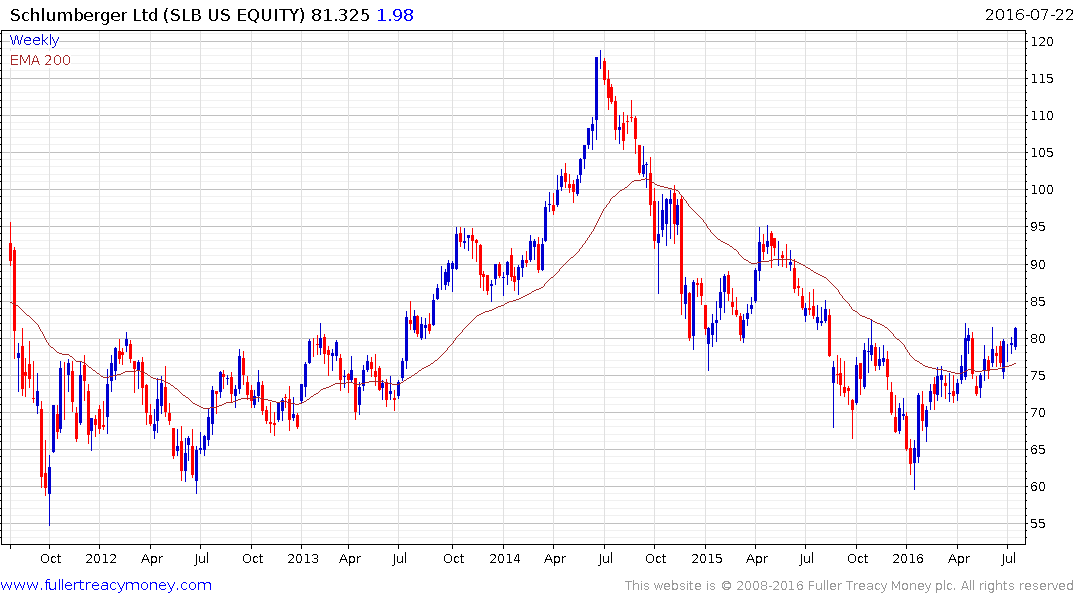

Interestingly Schlumberger and Haliburton have both concluded the lows are in for oil prices. They are not exactly early in making that call since prices almost doubled this year before entering the current pullback. What is does tell us however is they are potentially seeing greater interest from producers in the types of services they offer.

Schlumberger continues to consolidate above the trend mean while Haliburton is testing the lower side of an almost two-month range and will need to bounce soon if the consistency of the rebound from the January lows is to be sustained.

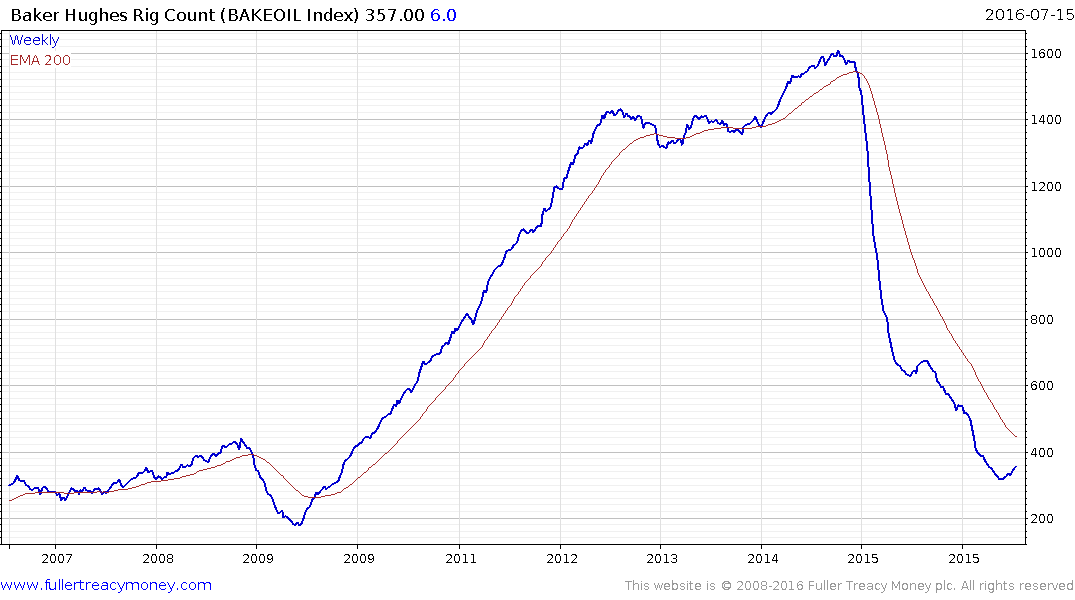

The completion of drilled wells has meant the Baker Hughes Rig Count has not acted as a lead indicator for renewed oil service sector activity but it has at least stopped going down.

The impending challenge for the sector is the fact that Brent Crude Oil has now posted a larger reaction than any since January, broken its progression of higher reaction lows and is now trading back below the trend mean. The six-month uptrend has lost consistency. While we concur there is a strong likelihood oil prices hit medium-term lows in January, the most likely scenario following such an impressive rebound is for some volatile ranging with what could be sharp peak to trough swings and a retest of the low is not out of the question.