Email of the day on the big turn:

Since returning from the Chart seminar in London I have spoken to several people who work in the Israeli high-tech industry, They all tell me that about 10% of their colleagues have lost their jobs recently. Today you referred to your MIIN index. How can we invest in these countries?

Thank you for this additional insight. The market for big ideas ballooned with the delivery of free money. Suddenly, no idea was too grand, or time to delivery/commercialization too long. That trend was looking tired in 2019, as the Federal Reserve’s quantitative tightening was siphoning liquidity from the global economy.

The monetary and fiscal response to the pandemic blew a bubble in the valuation of private assets that’s on par with the late 1990s. Job losses in the tech sector are leading the wider market because that is where hiring policies were most bloated during the boom.

Think about companies like Instacart, DoorDash, or Delivery Hero that thrived during the pandemic. Tightening liquidity and consumer balance sheets deprives them of both funding and customers.

I took a taxi, in Paris, last week for the first time in years. The first thing the driver said was his card machine does not work and requested cash. When we turned around to leave, it suddenly worked again. It was a gentle reminder of why companies like Uber have been successful.

However, Uber and Lyft have serious problems with how to make money and maintain their price advantage relative to taxis. In the end, they were big bets on autonomous driving and that is not going to be delivered any time soon. Tesla is expanding the rollout of its “full self-driving” tech to more customers. Even if it does not work as described it’s bad news for ride-hailing services. https://www.teslarati.com/tesla-fsd-beta-rollout-no-autopilot-miles-safety-score/

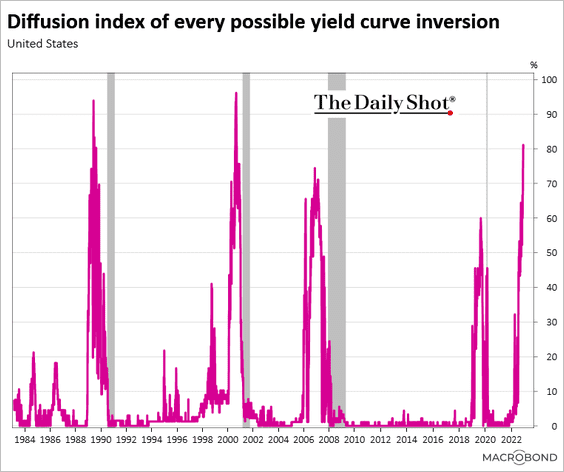

More than 80% of the yield curve is now inverted. What we need to be prepared for is a deflationary shock. Within the year 10-year yields could easily halve from the October peak. Endowments will only begin to write down their investments in private enterprises/property at the end of the year.

More than 80% of the yield curve is now inverted. What we need to be prepared for is a deflationary shock. Within the year 10-year yields could easily halve from the October peak. Endowments will only begin to write down their investments in private enterprises/property at the end of the year.

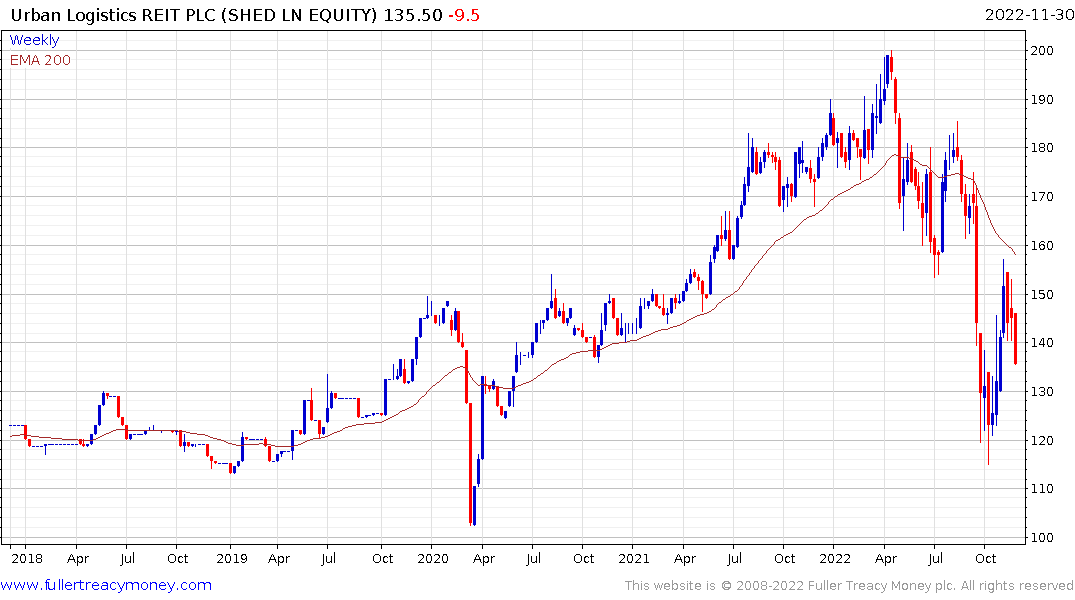

Commercial property is way overpriced for this stage of the credit cycle. The UK-listed Urban Logistics REIT (warehouses) remains in a significant downtrend for example.

These kinds of investments need lower rates to sustain their values. That’s a possibility next year as economic weakness forces monetary tightening to go into reverse. Corporate earnings have not weakened yet so valuations still have room to expand in the megacap sector.

The FANGMANT/total market cap of the US market chart continues to have Type-3 top formation completion characteristics.

The epicentre of risk is in private markets. While the UK pension leverage was a visible symptom of trouble, all long-term income investors have been presented with the same issue. The only way to capture yield was through taking on more risk. Monetary tightening will expose more issues in this sector.

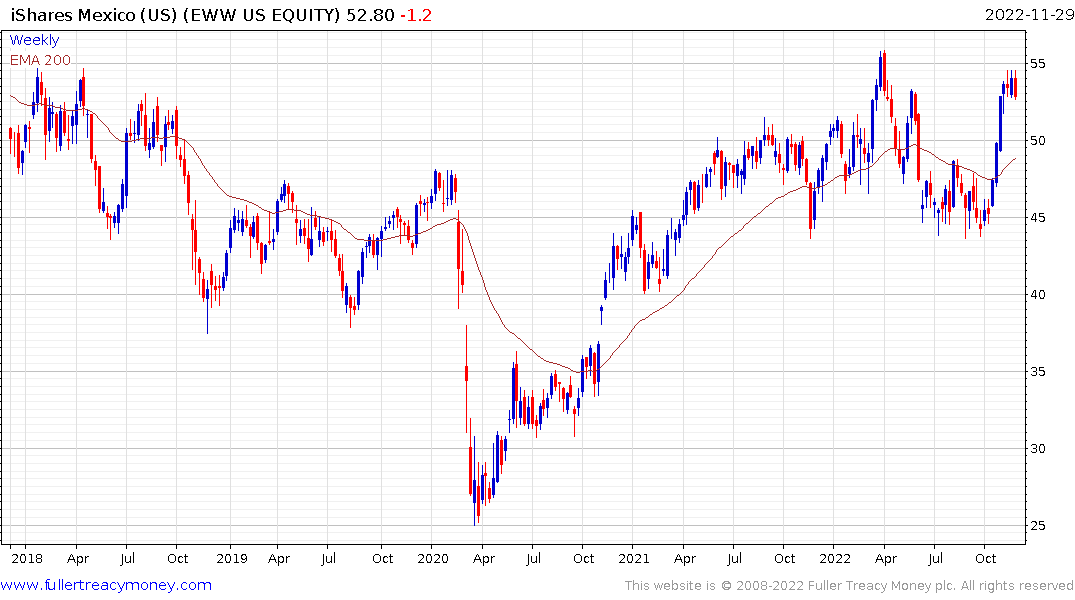

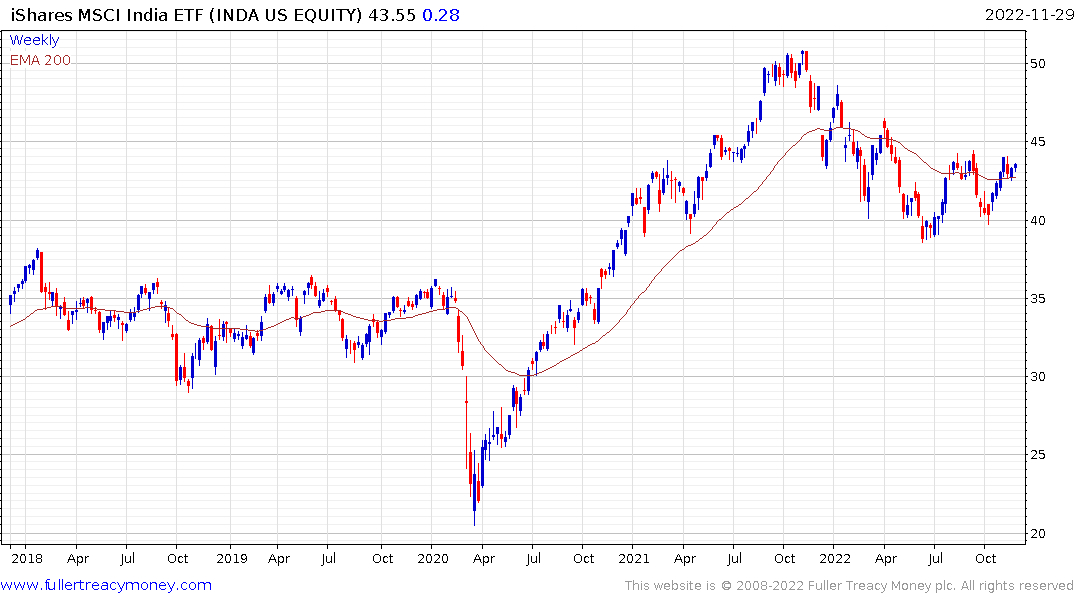

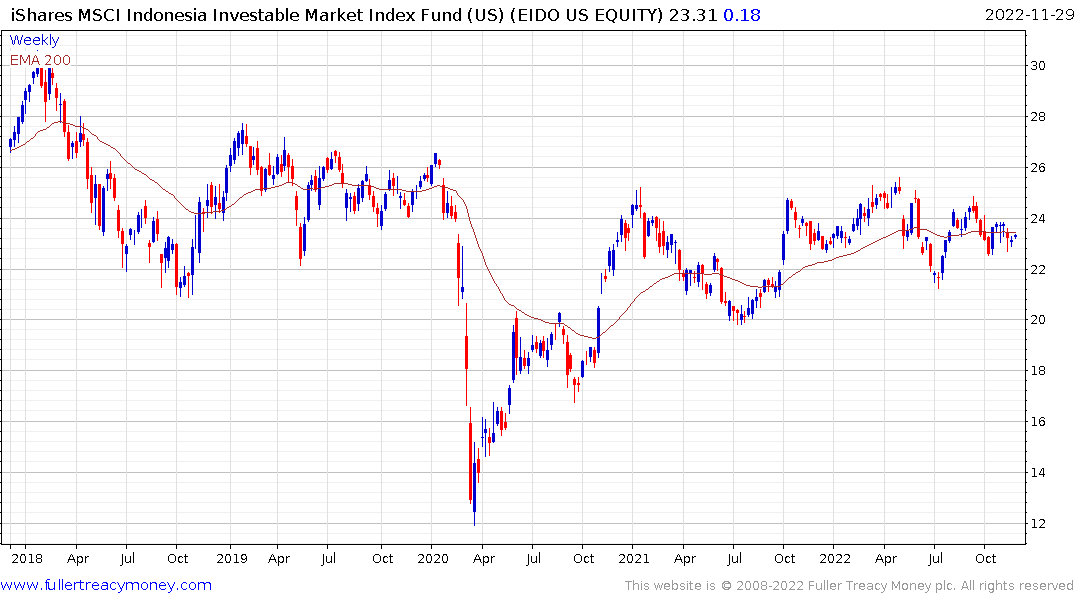

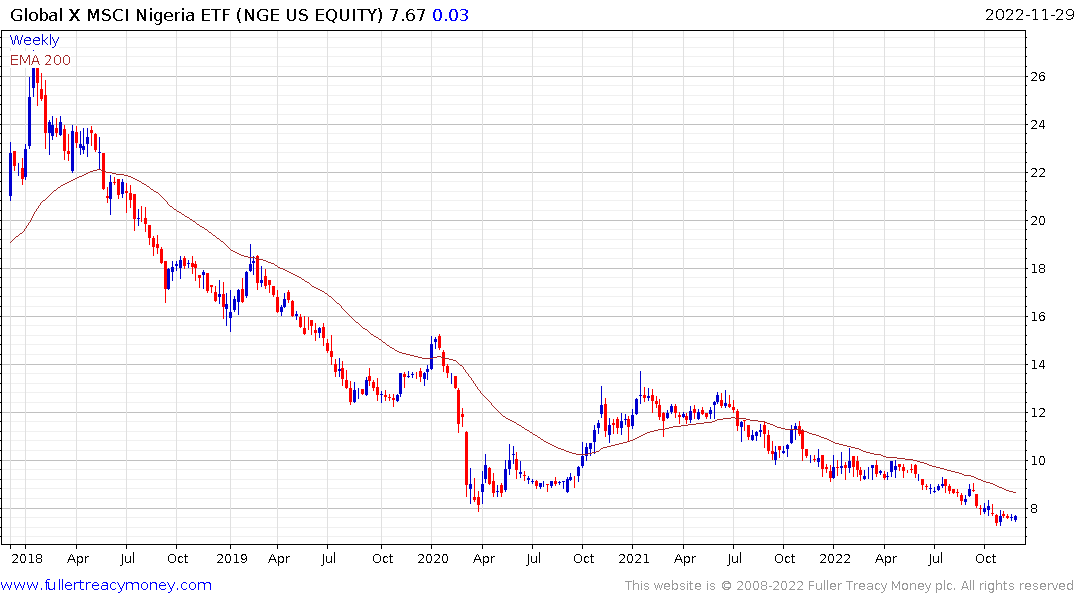

The Dollar has hit a medium-term peak. That supports precious metals and emerging markets. The countries outside the main geopolitical theatre benefit from great power competition. At least for now Mexico, India, Indonesia, and Nigeria are well placed as major population centres, commodity exporters and, growing manufacturing centres.

There are ETFs for all of these countries. Mexico (EWW), India (INDA), Indonesia (EIDO) and Nigeria (NGE).

There are ETFs for all of these countries. Mexico (EWW), India (INDA), Indonesia (EIDO) and Nigeria (NGE).

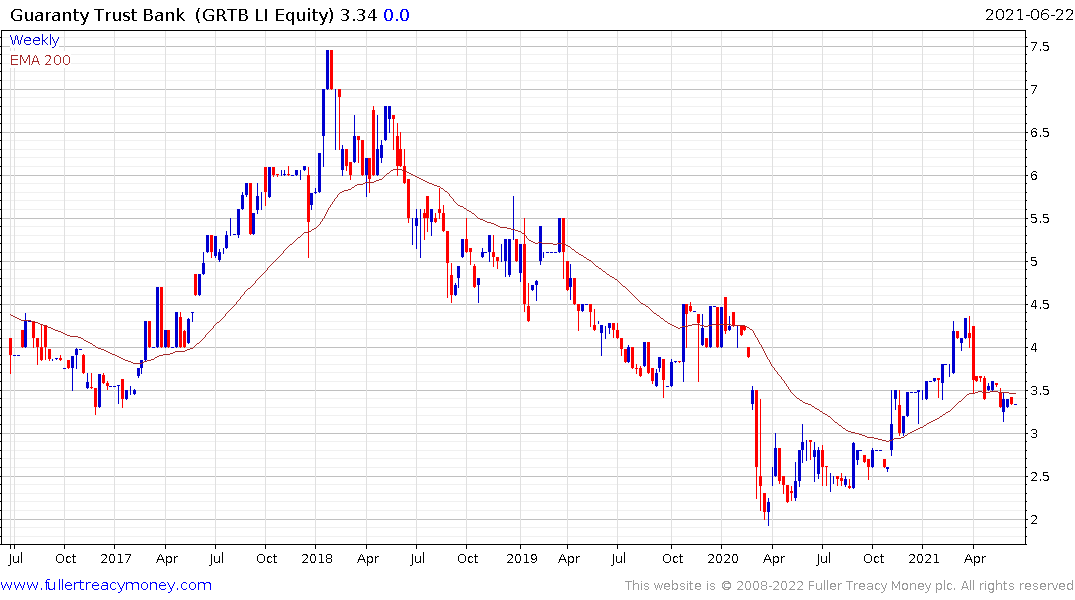

Nigeria’s Guaranty Trust Banks’ UK listed GDR is building a base formation.

Zenith Bank is rebounding from very depressed levels on the local market but its ADR is illiquid.

My intention in highlighting the relative performance of select emerging markets is to point to where opportunities will rest next year. The risk in the next few months is earnings roll over, stocks have another down-leg and growth surprises on the downside. That is what will be required to force central banks to relent and create an attractive medium-term buying opportunity.

Back to top