A Circular Reference: Ushering In A New Era For Natural Gas

Thanks to a subscriber for this report which may be of interest to subscribers. Here is a section:

Previously a commodity with volatile price swings due to a domestic market that was short supply, the outlook for natural gas through 2020 shows a well supplied market capable of delivering to growing demand sources. There will be s-t dislocations (weather / infrastructure constraints) and the introduction of LNG exports will re-couple the U.S. to the global economy, but we see an emerging theme of natural gas entering a range bound period of $3-3.50/mmbtu. The 5 year build up in demand (2013-18) now looks to be meeting up with the 10 year buildup in supply (2005-15), creating a period of price equilibrium with upward and downward pressures on both sides.

Demand – Focus On The Known Drivers

After a 15 year period of stagnant consumption (1995-2009), demand for natural gas has enjoyed consistent growth over the past 5 years (2-3Bcfpd annually), a trend we expect to pick up through 2020. The drivers of growth are visible – power generation, industrial use, and Mexico exports – and will provide a base level of consumption growth. The reemergence of natural gas on the global scene via LNG exports has also long been a theme and will be additive to demand, though the quantifiable impact is tough to point to as capacity utilization will vary based on global prices and supply. We estimate ~6Bcfpd of export demand in 2020 in our base case, which is needed to balance the S/D outlook. In total, we see demand growth approaching ~98Bcfpd by 2020 (ex pipeline imports) up from ~78Bcfpd in 2015.Supply – Filling Demand Needs…Just Need More Pipeline Capacity

U.S. supply has increased ~50% over the last 10 years to ~75Bcfpd, a rate of growth not witnessed since the 1960-1970s and following a brief pause in 2016/17, we anticipate growth to resume in 2018. We see four key trends from our supply forecast: 1) Supply is ~2Bcfpd below demand (weather normalized) in 2016/17 but ~3Bcfpd oversupplied in 2018, 2) Northeast supply growth increases by ~9Bcfpd in 2018, driven by the pipeline build out, 3) The bull case for supply by 2H18 is based on demand as the Northeast has excess pipeline capacity, and 4) The Northeast isn’t the only source of growth as we anticipate the Haynesville and Associated Gas Basins to return to growth by 2018, and implementing new technology could support growth elsewhere. Our forecast grows to meet demand and fills storage with enough deliverability in 2018, creating a more range bound environment with equal s/d pressures.

Here is a link to the full report.

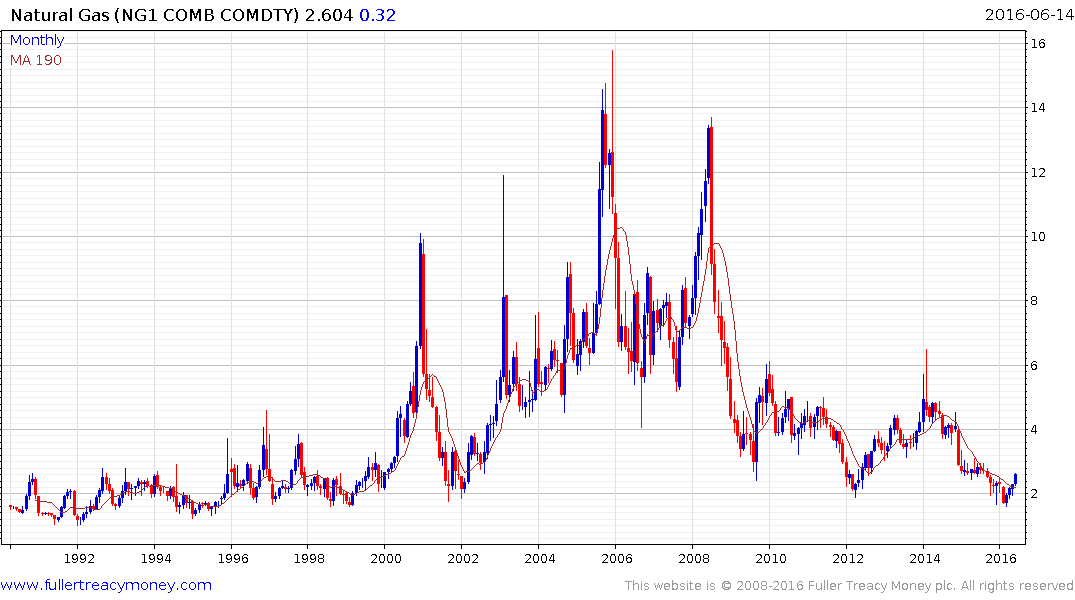

The natural gas market was the original recipient of the innovations that led to the boom in unconventional supply. Since then it has offered an object lesson in the ramifications of how that is likely to play out for other commodities where supply is surging not least oil. The greatest beneficiaries have been consumers who have seen prices for essential energy commodities decline to levels not preciously imaginable. That has also resulted in demand increasing not least from substitution which has also benefitted consumers in other sectors.

Natural gas is the only major commodity that has returned to test the lows that prevailed before bull market that began in the early 2000s. That alone is a measure of how profound the change on the supply side had been. Following the contract change in late May prices have staged an impressive rally and a break below $2.50 would now be required to check momentum.

Medium-term, the outlook remains for prolonged ranging but the upper side of that range is close to $6 based on what has occurred over the last decade.

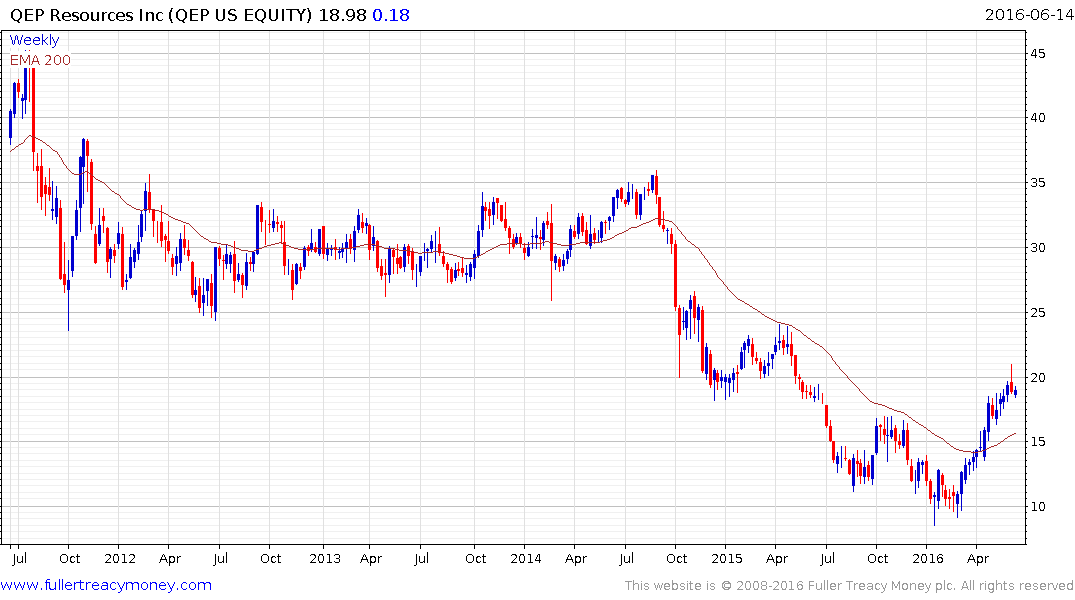

QEP Resources, SM Energy, Cimarex Energy and Encana share similar patterns with natural gas and continue to extend their rebounds.